AI Fraud Prevention Needs More Than a Risk Score

Here is my unpopular opinion after a decade around fraud teams: a fraud score is often the least interesting part of a fraud system.

There, I said it.

A score can help prioritize work. It can nudge a claims adjuster, AP analyst, or expense reviewer toward a closer look. But if your AI fraud prevention program depends on a mysterious number between 0 and 100, you have not built a control. You have built a very confident shrug.

I have seen this play out in real life. A claims team once showed me a dashboard where every suspicious invoice had a score, a color, and almost no explanation. Red meant bad. Green meant fine. Yellow meant someone had to ruin their afternoon. When I asked why one invoice was red, the answer was, “The system says it is high risk.” That is not fraud prevention. That is astrology with a login.

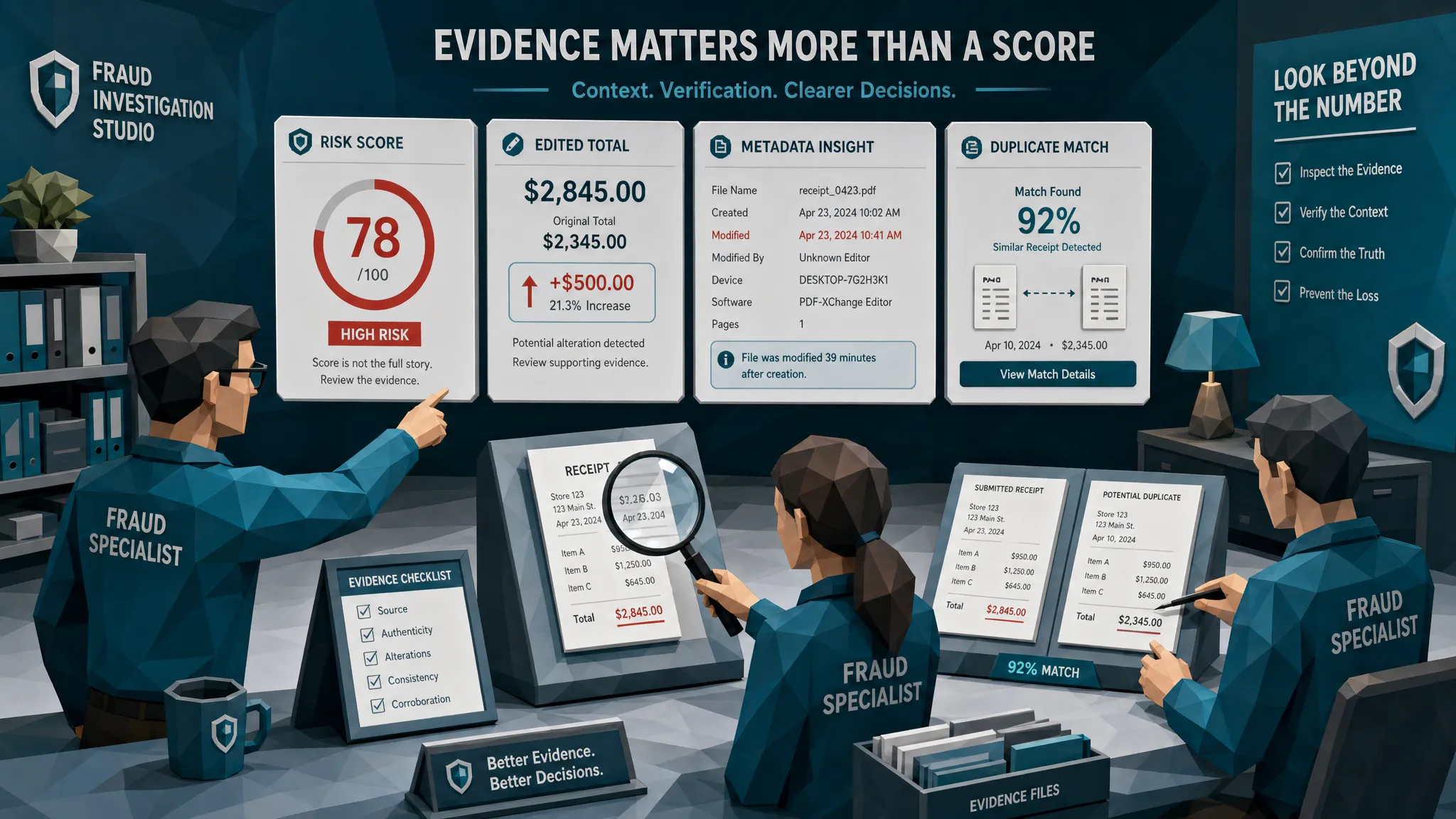

Modern fraud, especially invoice, receipt, and claims document fraud, does not fall apart because a system says “87% risky.” It falls apart because someone can point to evidence: the edited total, the mismatched metadata, the duplicate receipt submitted under a different claim, the bank details that changed after approval, or the math that only works if tax laws took the day off.

Why risk scores became so popular

Risk scores are popular because they are tidy. Executives like them because they fit neatly into dashboards. Operations teams like them because they help sort queues. Vendors like them because they are easy to demo.

And to be fair, a score is useful. Nobody wants a 60-page forensic report on every $42 lunch receipt. In high-volume AP, insurance claims, warranty claims, and employee expenses, teams need prioritization. A score tells reviewers where to look first.

The problem starts when the score becomes the decision.

Fraud work is messy. It requires judgment, context, and proof. A risk score compresses all of that into a number. That compression is convenient, but it hides the very things investigators need to act.

If an invoice receives a 91 risk score, what should the AP manager do? Hold payment? Call the vendor? Escalate to internal audit? Ask the business approver to re-confirm? If the system cannot explain what triggered the score, the team is left guessing. Guessing is not a control environment. It is how bad payments sneak through and good vendors get annoyed.

The fraud problem has outgrown “looks suspicious”

Fraud has always adapted to controls, but the pace has changed. A few years ago, altered documents often looked altered. Fonts were wrong. Boxes were crooked. Totals looked pasted in with the subtlety of a ransom note.

Now, fake and manipulated documents can look painfully clean. AI-generated invoices and receipts can pass a quick visual review. A fraudster can change dates, totals, tax lines, payee details, and supporting photos in minutes. The result may look polished enough for a busy reviewer at 4:55 p.m. on a Friday.

The trend is not theoretical. Verisk’s 2025 fraud research reported that 55% of Gen Z respondents would consider using AI to alter claim evidence, compared with 12% of boomers. Admiral also told the BBC it saw a sharp rise in fraudulent claims, with AI-generated fake images and deepfakes part of the picture.

Finance teams are not spared either. The Association for Financial Professionals has repeatedly found that payments fraud targets a large share of organizations. The FBI’s insurance fraud overview also warns that fraud adds real cost to households and businesses, not just insurers.

My hot take: the next wave of AI fraud prevention will be judged less by how accurately it scores risk and more by how clearly it explains evidence.

A score does not tell you what kind of problem you have

Two documents can both score “high risk” for very different reasons.

One invoice may be a genuine vendor invoice with an altered bank account. Another may be a fully synthetic invoice from a fake supplier. A third may be a duplicate of a real invoice, lightly edited and resubmitted. A fourth may be legitimate, but badly scanned, compressed, and sent through three forwarding chains before landing in AP.

If all four get the same red badge, your team still has to figure out what to do next.

This matters because each scenario calls for a different response. A possible bank-detail change may need vendor verification through a trusted channel. A duplicate may need cross-system matching. A suspected synthetic invoice may need document forensics and vendor validation. A poor-quality scan may need the original file, not an accusation.

When a score does not explain the type of risk, it creates two bad habits. Reviewers either overreact and block too much, or they get numb and push items through. I have watched both happen.

The second one is more dangerous. Once reviewers believe the tool “cries wolf,” they stop treating alerts as evidence. They treat them as noise.

The evidence layer AI fraud prevention actually needs

A good fraud alert should feel like a case note, not a fortune cookie.

In invoice and receipt fraud, the most useful systems show what changed, what conflicts, and what needs to be verified. The score should summarize the evidence, not replace it.

A strong alert usually answers a few simple questions:

- What specific document signals were found?

- Does the file history suggest editing, generation, or manipulation?

- Do the numbers reconcile across subtotal, tax, discounts, and total?

- Has this document, or a near-copy of it, appeared before?

- Does the payment information make sense for this vendor, claimant, employee, or project?

Notice how ordinary those questions sound. That is the point. The best fraud work is often not magical. It is disciplined common sense applied at scale.

I once reviewed a batch of expense receipts where one employee had submitted the same dinner receipt twice, six weeks apart. The second version had a slightly different crop, a heavier blur, and a tip that had grown like it had been watered. The risk score was useful because it pushed the item into review. But the case was made by the evidence: near-duplicate image, altered total region, inconsistent math, and a payment card reference that did not match the claimed date.

That is the difference between “the system thinks this is bad” and “here is why this should not be reimbursed yet.”

Payment context is where many fraud tools get interesting

A document can look real and still be wrong.

This is where I think many AI fraud prevention tools fall short. They inspect the image, maybe read the fields, and then stop. But invoices and receipts do not exist in a vacuum. They are attached to claims, vendors, employees, purchase orders, card transactions, bank details, projects, service dates, and approval chains.

A moving invoice in a home insurance claim, for example, might be perfectly plausible on its face. If a policyholder had water damage and needed contents moved into storage, an invoice from a real local provider such as Zapt Movers would not be strange. The question is whether the submitted document matches the loss timeline, service address, payee, amount, and payment trail. A legitimate business name does not make every submitted PDF legitimate.

That point sounds obvious until you sit in a claims queue with 400 documents waiting.

Payment context catches the “near right” frauds. The invoice vendor exists, but the bank account is new. The receipt total is plausible, but the card transaction is missing. The claim repair date is reasonable, but the metadata says the file was created months later. The supplier is approved, but this invoice arrives from an unusual channel with altered remittance details.

Fraudsters often focus on making the document look good. They are less disciplined about making the whole story hold together.

False positives are not a side issue

Fraud teams talk a lot about missed fraud. They should. But false positives can quietly wreck a program.

Every bad alert has a cost. It slows clean payments. It irritates legitimate vendors and customers. It teaches reviewers to distrust the tool. In insurance, it can turn a simple claim into a bad customer experience. In AP, it can strain supplier relationships. In employee expenses, it can make staff feel like finance has installed a tiny courtroom inside the expense portal.

This is why I dislike score-only systems. They often hide uncertainty. A document might be risky because it has strong evidence of manipulation, or because it resembles past fraud patterns in a loose way. Those are not equal. A mature system should separate high-confidence evidence from softer indicators.

For example, “edited total area with inconsistent pixel structure and tax math mismatch” deserves a different workflow than “unusual vendor amount compared with past invoices.” The first may justify holding payment. The second may justify a quick verification.

Good AI fraud prevention should reduce unnecessary friction, not spread suspicion like confetti.

What a useful fraud alert should look like

If I were designing an alert for a claims manager, AP manager, or expense lead, I would keep it plain.

Start with the document and the reason it matters. “Invoice total may have been altered.” Then show the evidence. “The total region has visual manipulation indicators. The file metadata shows editing software after document creation. The tax line does not reconcile with subtotal and jurisdiction. A near-duplicate invoice was submitted under a different claim last month.”

Then recommend the next action. Not a dramatic “fraud confirmed,” because that is rarely appropriate at first pass. Something more operational: “Hold payment pending vendor verification,” “Request original file,” “Route to SIU,” or “Compare against card transaction.”

That structure gives teams confidence. It also makes audits easier. If a payment is stopped, the organization can explain why. If a claim is escalated, SIU receives evidence, not vibes. If a vendor pushes back, AP can point to specific inconsistencies rather than hiding behind a score.

In my experience, investigators do not need the system to be theatrical. They need it to be specific.

Where Docklands AI fits into this problem

Docklands AI is built around a simple idea: invoices and receipts should be checked as evidence before they trigger payment, reimbursement, or claim settlement.

That means looking beyond extracted fields. Docklands AI analyzes documents for signs of AI generation, Photoshop edits, tampering, metadata issues, mathematical irregularities, physical manipulation, duplicates, and related payment context. It is designed for the workflows where document fraud hurts most: insurance claims, accounts payable, and employee expenses.

The payment-context piece matters. A generic “is this image real?” check can miss the broader fraud picture. A document may be visually convincing, but still conflict with claimant history, vendor payment details, invoice timing, or reimbursement behavior. When document evidence and payment context are reviewed together, the alert becomes more useful to the human who has to make the call.

And that is the real goal. We are not trying to replace adjusters, AP analysts, fraud managers, or internal auditors with a number. We are trying to give them better evidence sooner, before money leaves.

How to move from score-led to evidence-led prevention

The shift does not have to be dramatic. In fact, I prefer boring implementations. Boring is underrated in fraud control. Boring means the process works on Tuesday when everyone is busy.

First, preserve original documents. Do not rely only on OCR output or extracted fields. Once the original file is lost, compressed, or overwritten, you may lose the visual and metadata clues that prove manipulation.

Second, screen before payment. Post-payment detection has its place, but it is expensive, awkward, and often too late. Recovering funds is harder than not sending them.

Third, connect document checks to the surrounding transaction. Compare invoice details to vendor records, claim data, card transactions, employee history, approval patterns, and bank-detail changes. Fraud usually leaves inconsistencies in the seams.

Fourth, route alerts by evidence type. A duplicate should not follow the same path as a suspicious bank-detail change. A possible AI-generated receipt should not be treated like a policy violation over a missing meal attendee. Different risks need different playbooks.

Finally, measure reviewer outcomes. Which alerts led to confirmed fraud, corrections, vendor verification, or clean release? Use that feedback to tune thresholds and workflows. A fraud system should learn from actual operations, not just from historical data sitting politely in a warehouse.

The score still matters, but it should know its place

I am not anti-score. I am anti-mystery score.

A risk score is useful when it helps triage a queue, set severity, or decide which documents need human review. It becomes dangerous when it replaces evidence, hides uncertainty, or gives teams a false sense of control.

The future of AI fraud prevention is not a prettier dashboard with bigger numbers. It is a cleaner handoff between automated detection and human judgment. The system should say, “Here is what I found, here is why it matters, and here is what you should verify next.”

That is how fraud teams win. Not by trusting the number. By following the evidence.

Frequently Asked Questions

Is a fraud risk score useless? No. A fraud risk score is useful for prioritization, especially in high-volume claims, AP, and expense workflows. The problem is relying on the score without supporting evidence, explanation, and a clear review process.

What should AI fraud prevention include besides a score? It should include document forensics, metadata analysis, mathematical checks, duplicate detection, payment-context review, evidence-backed alerts, and workflow routing that tells reviewers what to verify next.

Why is payment context important for invoice and receipt fraud? Payment context shows whether the document fits the surrounding transaction. A receipt or invoice may look real, but still conflict with vendor records, bank details, claim timelines, card transactions, or prior submissions.

How can teams reduce false positives in fraud detection? Separate strong evidence from weaker indicators, route alerts by severity, keep clean items moving, and track reviewer outcomes. False positives fall when alerts explain the specific issue instead of relying on a vague high-risk label.

Where should document fraud screening happen? Ideally at intake and again before payment or reimbursement if key details change. Early screening helps teams stop suspicious documents before funds move, while keeping legitimate claims, invoices, and expenses flowing.

Build fraud prevention your reviewers can actually defend

If your fraud workflow depends on a risk score that nobody can explain, it is time to raise the standard.

Docklands AI helps teams inspect invoices and receipts for manipulation, AI generation, metadata anomalies, math issues, physical tampering, duplicates, and payment-context conflicts before payment. The result is not just a number, but evidence your reviewers can use.

If you want AI fraud prevention that supports real decisions instead of decorating a dashboard, explore Docklands AI and see how evidence-led document screening can fit into your claims, AP, or expense workflow.

Request a Demo Today!

Book your demo below.