Auto Insurance Claim Fraud Often Starts With a Receipt

Hot take from a fraud person who has spent too many evenings staring at claim files: the most dangerous document in an auto claim is often not the dramatic crash photo. It is the dull little receipt.

A receipt looks harmless. It is small, familiar, and usually low drama. Nobody frames a receipt on the wall. But in auto insurance claim fraud, that tiny document can quietly turn a normal loss into an inflated payout, a duplicate reimbursement, or a completely fabricated expense trail.

The FBI has long warned that insurance fraud creates real costs for households, with non-health insurance fraud alone estimated at more than $40 billion per year and adding hundreds of dollars to the average family’s premiums, according to the FBI’s insurance fraud overview. That number is not built from movie-style criminal masterminds. A lot of it comes from routine claims where one piece of evidence looks “good enough” to pass.

And in auto claims, “good enough” often starts with a receipt.

Why receipts matter more than most claims teams admit

A receipt does three jobs in an auto insurance claim. It proves that a cost happened, it anchors the amount, and it gives the claim a sense of completion. Once a receipt enters the file, the conversation shifts from “Did this happen?” to “Can we reimburse it?”

That shift is exactly why receipts are attractive to fraudsters. A doctored towing receipt can add $250. A stretched rental receipt can add $600. A recycled repair receipt can add thousands. None of those manipulations need to reinvent the crash. They only need to make the paperwork slightly more expensive than reality.

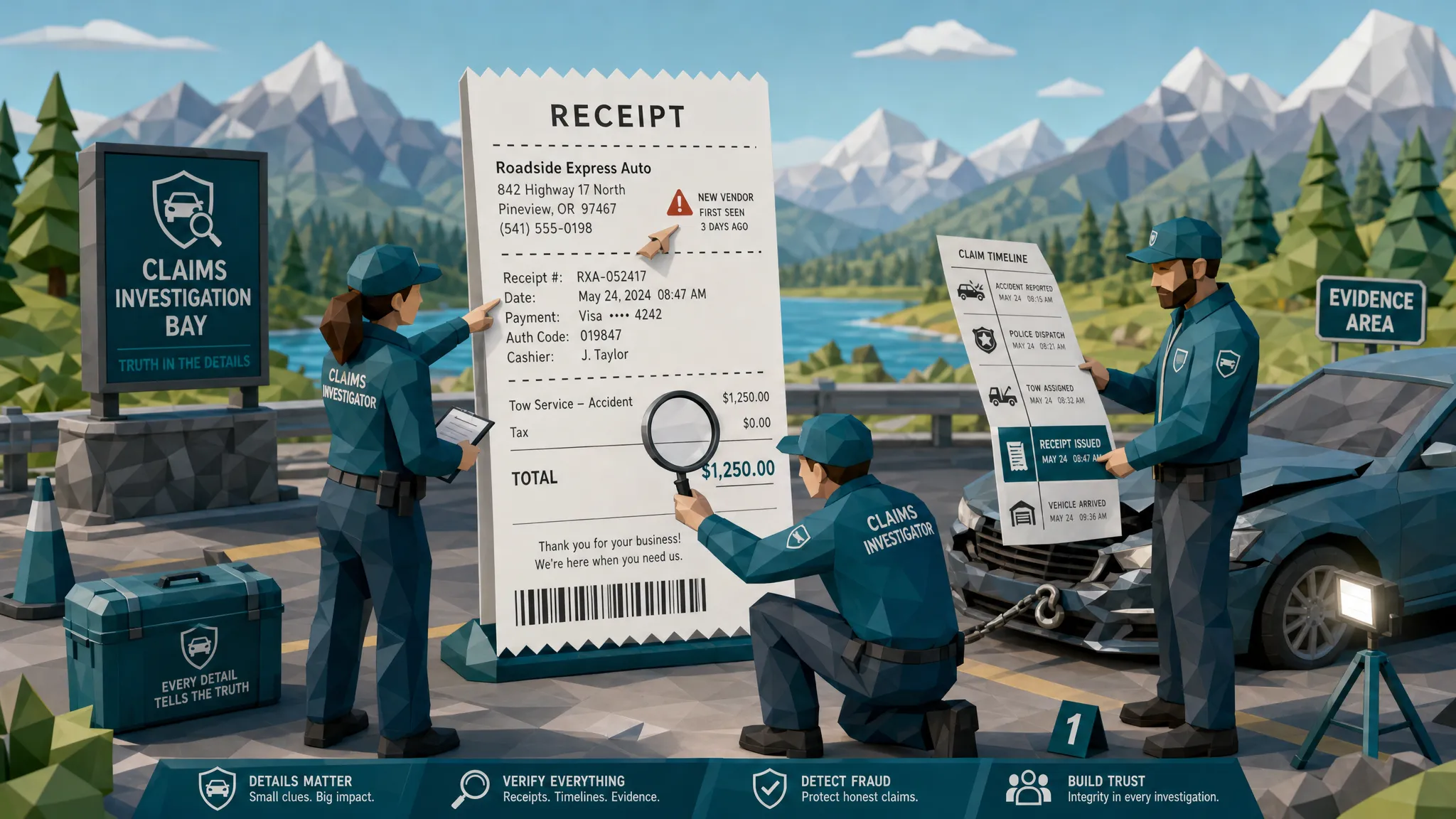

I once reviewed a relatively boring fender-bender claim where the photos looked fine, the claimant sounded normal, and the repair estimate was plausible. The issue was a towing receipt. It showed a tow two days before the accident date, from a vendor whose listed business hours did not cover the claimed pickup time, with a cash payment and no vehicle identifier. One receipt cracked open the whole file. Not because it screamed “fraud,” but because it whispered “please do not look too closely.”

That is how a lot of auto insurance claim fraud works. The fraud is not always a fake accident. Sometimes the accident is real, but the supporting costs are padded, reused, or manufactured.

The receipt is where leakage becomes measurable

Claims leaders talk about leakage, but I think we sometimes make it sound too abstract. Leakage is the difference between what should have been paid and what actually went out the door. A receipt is where that difference gets written down.

If you want a simple mental model, think of fraud leakage like compound interest in reverse. Small amounts, repeated across a large book, stop being small. For anyone who likes seeing how tiny financial percentages snowball, educational resources such as financial literacy and investing guides make the compounding point very clearly. In claims, the same math cuts the other way. A few hundred dollars per inflated receipt, multiplied across thousands of claims, becomes a serious number.

That is why I do not roll my eyes at “minor” receipt issues. A $93 discrepancy may not deserve a full SIU parade with confetti and subpoenas. But patterns of $93 discrepancies absolutely deserve attention.

The common receipt tricks in auto claims

Auto claims create a surprisingly rich menu of receipt-based fraud opportunities. The best ones, from the fraudster’s point of view, blend into ordinary claim handling.

Towing and storage receipts are a classic. A claimant submits a legitimate-looking tow bill, but the date is shifted, the mileage is inflated, or daily storage fees continue after the vehicle was supposedly released. The document may be genuine at the core, with only one or two fields changed.

Rental receipts are another favorite. If repair time is five days, the rental receipt says nine. If the claimant used a compact car, the receipt suggests an SUV. If there was no rental at all, a downloaded template can do a passable impression of one, especially when submitted as a photo instead of a clean PDF.

Repair receipts are where the dollars get more serious. A body shop invoice may include parts that do not match the damage, labor hours that exceed the estimate, or line items that duplicate what was already paid directly to a repair facility. Sometimes the receipt is not a receipt at all. It is an estimate dressed up like proof of payment, which is the claims equivalent of wearing a tuxedo T-shirt to court.

Then there are parts receipts, glass repair receipts, rideshare receipts, parking invoices, and “miscellaneous” expenses. I have learned to fear the word miscellaneous. It often means the submitter could not find a better category for something they want paid.

The first clues are boring, which is exactly the problem

Receipt fraud rarely announces itself with a neon sign. The clues are usually small, boring, and easy to miss during a busy day.

Here are the receipt signals I want adjusters and claim reviewers to slow down for:

- Dates that do not fit the accident timeline, repair timeline, rental period, or reported first notice of loss.

- Vendor details that are vague, inconsistent, newly created, or impossible to verify through ordinary channels.

- Math that is close enough to look right, but wrong when tax, subtotal, discounts, or fees are recalculated.

- Payment details that do not match the claimant’s story, such as cash-only receipts for large expenses or missing card information where it should exist.

- File clues that suggest editing, including strange compression around totals, mismatched fonts, cropped edges, or metadata showing later modification.

- Receipts that resemble earlier submissions across other claims, especially with the same layout, same damage description, or same suspicious vendor.

None of these proves fraud alone. That matters. Good fraud work is not about shouting “gotcha” at every odd receipt. It is about stacking evidence until the story either makes sense or starts to wobble.

Why busy adjusters miss manipulated receipts

I do not blame adjusters for missing this stuff. I have been in enough claim operations rooms to know the pressure. Customers want payment. Repair shops want status. Supervisors want cycle times down. Nobody gets applause for spending 14 minutes inspecting the kerning on a $180 tow receipt.

That is the fraudster’s edge. Modern claims workflows are designed to move clean claims quickly, as they should be. But that speed creates blind spots when the supporting document looks ordinary.

OCR can extract the date, vendor, amount, and maybe the tax. Useful? Absolutely. Fraud detection? Not really. OCR reads what the receipt says. It does not tell you whether the receipt was altered, recycled, fabricated, or inconsistent with the payment trail.

And now the document problem is getting noisier. BBC reporting on Admiral data described a sharp rise in fraudulent claims, with AI-generated fake images and deepfakes becoming part of the claims fraud landscape. Verisk’s 2025 fraud research also points to a market where claim manipulation is getting more sophisticated, including younger consumers showing more willingness to alter claim evidence, according to Verisk’s 2025 Fraud Report.

My view is simple: if photos are getting easier to fake, receipts are not magically staying honest.

A receipt-first triage that actually works

When I train reviewers, I ask them to stop treating receipts as attachments and start treating them as witnesses. A witness can be truthful, mistaken, incomplete, or lying. The job is to compare the witness against the rest of the story.

First, check the timeline. Did the tow happen after the accident and before the repair? Did the rental dates match the period the vehicle was unavailable? Was the receipt created before the claim was filed, or did it appear only after a coverage dispute?

Second, check the payment story. A receipt that says paid by card should have some supporting payment logic. I am not saying you need a bank statement for every claim. That would turn claims into archaeology. But where the amount is high, the vendor is unfamiliar, or the receipt has other oddities, payment context matters.

Third, check the vendor. Real businesses leave footprints. Phone numbers, addresses, tax registrations, websites, reviews, invoices with consistent formatting, and prior claim history all help. Fraudulent receipts often use vendors that are too generic, too new, or oddly disconnected from the geography of the loss.

Fourth, check the document itself. Does the total look pasted over? Are the digits in the amount slightly sharper than the rest of the receipt? Is the file a screenshot of a screenshot? Does the metadata show editing software where you would expect a point-of-sale export or a phone camera original?

Fifth, check for reuse. This is where individual reviewers struggle, because no human can remember every tow receipt across a book of business. But duplicate and near-duplicate receipts are a major clue. Fraudsters reuse what worked. We all do, frankly. I have been using the same chili recipe for eight years.

Do not separate the document from the payment context

One mistake I see in fraud programs is treating document authenticity as a standalone question. “Is this receipt real?” is useful, but incomplete. The better question is: “Does this receipt make sense in this claim, with this vendor, this timeline, this amount, and this payment path?”

A perfectly real receipt can still be misused. Someone can submit a genuine receipt from an unrelated repair. Someone can reuse a rental receipt from a different claim. Someone can alter only the claim number or vehicle description while leaving the rest untouched.

The payment information on a claim is often the tie-breaker. If the receipt says a repair shop was paid directly, but the claim also requests reimbursement to the claimant for the same work, you have a problem. If a vendor’s invoice points to one payee and the payment instruction points elsewhere, you have a bigger problem. If the receipt is for a cash payment that conveniently lands just below a review threshold, I am at least raising an eyebrow.

This is where document screening becomes more useful when it is connected to the claim’s payment picture. A generic image check might say a receipt looks plausible. A claims-aware review asks whether the receipt fits the money movement.

Where Docklands AI fits in the claims workflow

A good fraud process should not punish honest claimants with endless delay. Most people filing auto claims just want their car fixed and their week back. The trick is to move clean claims quickly while quietly pulling suspicious documents into an evidence lane.

Docklands AI is built for that kind of document-level screening. It analyzes invoices and receipts for signs of manipulation, including photoshopped edits, AI-generated documents, metadata issues, mathematical irregularities, physical tampering, and duplicate patterns. It also uses payment information on the claim to build a fuller fraud picture, which is important because the receipt rarely tells the whole story by itself.

For claims teams, the practical value is not “let software deny claims.” Please do not do that. The value is better triage. Clean documents keep moving. Suspicious ones arrive with specific evidence reviewers can understand, such as a likely edited total, conflicting metadata, a reused receipt pattern, or a mismatch between the receipt and payment context.

That matters for SIU too. Investigators do not need more vague suspicion. They need defensible reasons to review a claim, ask for clarification, contact a vendor, or hold payment pending verification.

The reviewer mindset: curious, not cynical

There is a fine line between fraud awareness and assuming everyone is cheating. Cross that line and you create angry customers, unnecessary escalations, and a claims culture nobody enjoys.

The best fraud reviewers I have worked with are not cynical. They are curious. They ask calm questions. They preserve original files. They document what is inconsistent. They do not accuse a claimant because a receipt is ugly. Plenty of legitimate receipts look like they were printed during a thunderstorm.

The goal is not to catch every bad actor through suspicion. The goal is to build a workflow where the evidence gets checked consistently, especially before money leaves.

My rule of thumb is this: if the receipt changes the payout, the receipt deserves scrutiny proportionate to the amount and risk. A $22 parking receipt probably does not need a forensic drumroll. A $4,800 repair receipt from a new vendor with odd metadata and a late payee change absolutely does.

Frequently Asked Questions

What types of receipts are most common in auto insurance claim fraud? Towing, storage, rental car, repair, parts, glass replacement, and rideshare receipts are common targets because they directly affect reimbursement amounts and are often submitted as standalone proof.

Can OCR detect a fake or altered receipt? OCR can extract text from a receipt, but it generally cannot prove whether the receipt was manipulated, reused, or inconsistent with the payment context. Document forensics and contextual checks are needed for that.

Should every suspicious receipt go to SIU? No. Many issues can be resolved by asking for clarification, requesting the original file, or verifying with the vendor. SIU should receive cases where the evidence shows stronger indicators, repeated patterns, or material payout risk.

What is the biggest receipt red flag in an auto claim? The biggest red flag is a receipt that does not fit the surrounding story. That may mean timeline conflicts, vendor inconsistencies, payment mismatches, odd file history, or duplication across claims.

How can insurers reduce false positives when screening receipts? Use multiple signals rather than one rule. A strange font alone is weak evidence. A strange font plus wrong tax math, suspicious metadata, and a payment mismatch is a much stronger reason to review.

Final thought: start with the boring document

Auto insurance claim fraud rarely begins with a villain twirling a mustache. It begins with a document that looks ordinary enough to survive a busy workflow.

That is why receipts deserve more respect. They are small, but they carry the payout logic. They connect the accident story to the money. And when they are altered, recycled, or fabricated, they often reveal the fraud before the payment goes out.

If your claims team wants to screen invoices and receipts for manipulation, metadata issues, mathematical inconsistencies, duplicate patterns, and payment-context mismatches before payout, Docklands AI can help add that evidence layer into your workflow without turning every claim into a manual investigation.

Request a Demo Today!

Book your demo below.