Bogus Insurance Claims Often Start With One Edited Bill

I have a boring opinion that has saved a lot of money: many bogus insurance claims do not begin with a dramatic accident photo, a suspicious witness statement, or a grand conspiracy. They begin with one edited bill.

After ten years around fraud operations, I still trust a dull invoice about as much as I trust a hotel minibar price list. Most claim bills look ordinary because ordinary is the disguise. A total gets nudged upward. A date gets moved inside the coverage window. A line item appears that no one remembers approving. By the time the claim lands with an adjuster, the document has already done its quiet little magic trick: it has turned a story into a number.

That matters because insurance fraud is not a rounding error. The FBI has long estimated that non-health insurance fraud costs more than $40 billion a year in the U.S., adding roughly $400 to $700 to the average family’s annual premiums. McKinsey has also warned that insurers lose tens of billions globally to claims fraud, while only a portion of fraudulent claims are detected.

My hot take: if your claims workflow treats invoices and receipts as administrative paperwork, you are inspecting the crime scene after someone swept the floor.

Why one edited bill is such a powerful fraud tool

A bill is persuasive because it feels official. It has a logo, a date, a subtotal, a tax line, maybe a technician’s name. It gives everyone in the chain something concrete to point at. The claimant says the work was done. The vendor name looks plausible. The adjuster sees a payable amount. The claim system extracts the fields. Everyone moves on.

Fraudsters love that rhythm. Claims teams are busy, customers want fast payouts, and nobody wants to punish honest policyholders with unnecessary friction. Digital insurance has made legitimate buying and servicing far easier too. Platforms that help customers compare and buy insurance online in the UAE are part of a useful shift toward faster, clearer insurance experiences. The uncomfortable bit is that the same expectation of speed carries into claims, where a manipulated document can travel very quickly if no one checks the original evidence.

An edited bill also lets fraud hide in the middle. A completely fake claim may need a false loss event, fake photos, fake vendors, and a nervous claimant. A lightly edited invoice only needs one believable document and a process that is moving too quickly.

The small edits that cause big leakage

The obvious fraud is not what worries me most. If someone submits a receipt for a luxury yacht repair under a cracked phone claim, even the intern will raise an eyebrow. The expensive stuff is subtler.

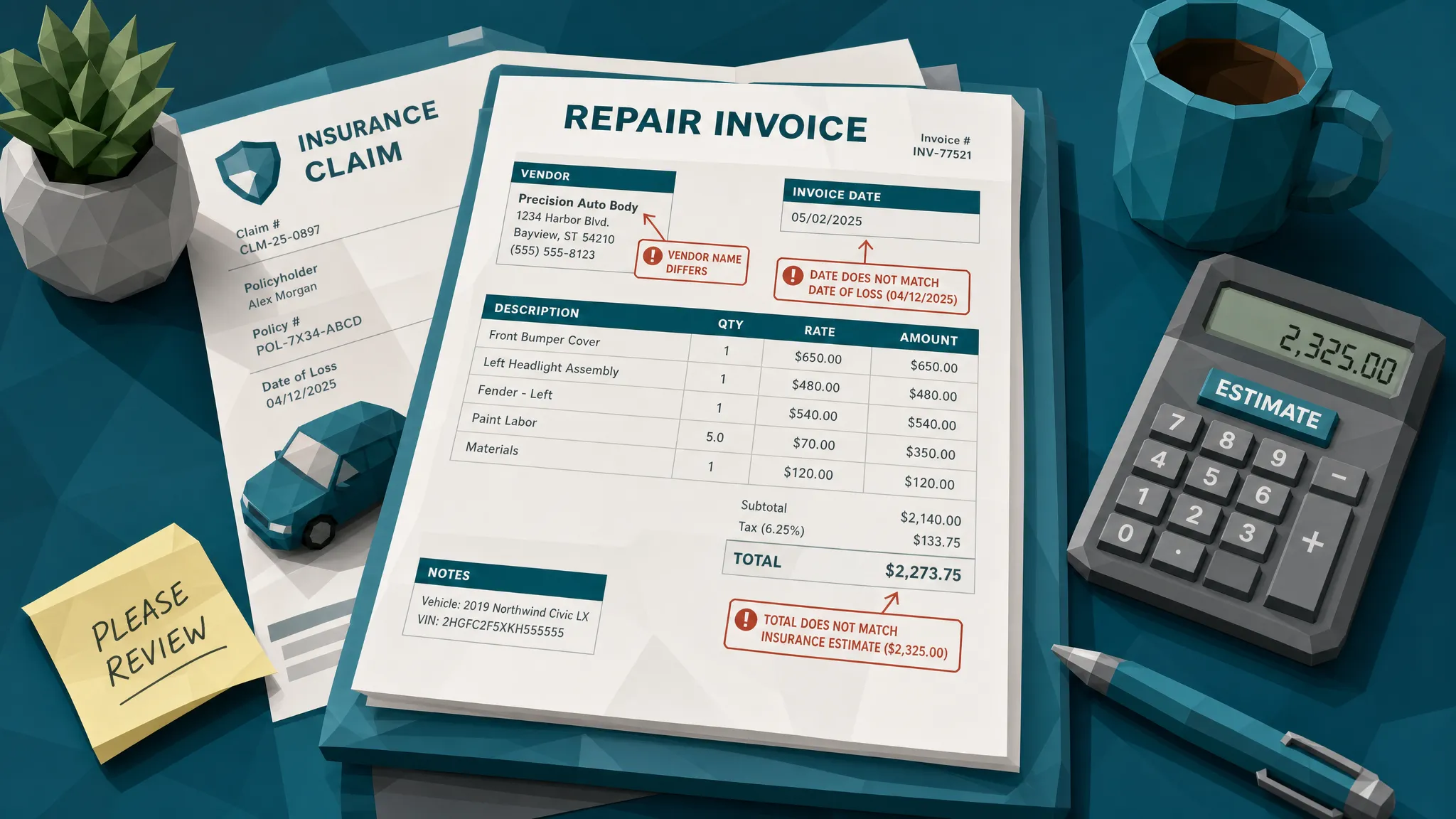

Totals are the easy edit. A $480 repair becomes $980. A contractor adds an emergency surcharge after the fact. A medical bill gets a larger patient responsibility amount. The overall layout still looks fine because only one number changed.

Dates get moved to fit coverage. This is common in property, health, warranty, and travel claims. A service date outside the policy period quietly becomes a date inside it. A receipt issued after a denial gets backdated to look contemporaneous. It is a tiny edit with a big consequence.

Line items appear or inflate. Water extraction becomes water extraction plus mold treatment. One replacement part becomes two. A diagnostic visit becomes a full repair. In warranty claims, I have seen invoices where the labor description expanded like bread dough, while the actual repair notes stayed suspiciously thin.

Payment details change late. This one deserves more attention. If a bill says the claimant paid Vendor A, but the reimbursement route points somewhere else, that is not a clerical detail. It is part of the fraud story. Docklands AI focuses heavily on the payment information around a claim, expense, or payment for this reason. The document and the money trail need to agree.

Vendor identities get borrowed. Fraudsters often use a real business name because real businesses pass the sniff test. The invoice may use a slightly wrong address, a different bank account, a copied logo, or a phone number that routes to the claimant’s cousin. Lovely family, terrible control environment.

What an edited bill usually gets wrong

Here is the good news: edited bills often leave clues. The bad news is that those clues are rarely the kind a tired reviewer notices at 4:47 p.m. on a Friday.

The first clue is visual inconsistency. Digits in one field may be sharper than the rest of the scan. A total may sit slightly higher than the neighboring text. The background behind an edited area may have a different texture. On photographed paper bills, shadows and compression patterns sometimes betray where someone pasted or covered a number.

The second clue is bad math. Fraudsters are surprisingly good at changing the big number and surprisingly bad at updating the boring ones. I once reviewed a repair invoice where the subtotal had been increased, but the tax still matched the original lower amount. The document looked polished. The arithmetic looked like it had been assembled during a coffee emergency.

The third clue is metadata. File history, timestamps, device information, and editing traces can contradict the claim story. A bill supposedly scanned at a shop may have been edited with design software. A receipt allegedly photographed at the time of purchase may have been created days later. Metadata is not perfect proof by itself, but it is very good at telling you where to ask the next question.

The fourth clue is duplication. A bill may be reused across multiple claims with small changes to date, name, address, or amount. In manual review, those near-duplicates are painful to spot. To a trained document screening system, they are often much louder.

And yes, the tools available to fraudsters are getting better. BBC reporting on Admiral’s 2025 findings described a sharp rise in fraudulent claims, including cases involving AI-generated fake images and deepfakes. Verisk’s 2025 Fraud Report also pointed to growing sophistication in claims manipulation and a worrying willingness among younger consumers to consider altering evidence with AI.

Still, the edited bill remains wonderfully old-fashioned. New tools, same human shortcuts.

Why normal claim review misses the edited bill

I have sympathy for adjusters. They are asked to be empathetic, fast, technically accurate, policy-aware, and fraud-sensitive, usually while managing a queue that seems to reproduce overnight. Expecting them to perform forensic document review on every bill is not a control. It is a wish with a headset.

Traditional claims systems also tend to focus on extracted data. The system reads the vendor name, date, amount, and claim number. If those fields pass the rules, the document may feel clean. But field validation does not prove the document is authentic. It only proves the fields look acceptable after extraction.

That distinction matters. A manipulated invoice can contain valid-looking fields. A forged receipt can pass a threshold rule. A backdated medical bill can match a policy period. If the review never looks at the original file as evidence, the fraudster has already won the first round.

There is another operational problem: once a bill is approved, it gains credibility. I have watched teams hesitate to challenge a document later because two people had already touched it and nobody flagged it. Approval becomes a little halo. Fraudsters know this. They aim for boring enough to pass the first look.

My seven-minute test for a suspicious claim bill

When I train claims teams, I do not start with dramatic fraud theory. I start with a simple sequence. It will not catch everything, but it catches more than vibes and coffee.

- Preserve the original file before converting, compressing, annotating, or forwarding it.

- Recalculate subtotal, tax, discounts, fees, and final amount by hand or with a trusted tool.

- Compare service dates against the loss date, policy period, inspection notes, and claimant timeline.

- Check whether the vendor, payee, bank details, address, and phone number tell the same story.

- Look for visual mismatches in fonts, spacing, shadows, background texture, and image sharpness.

- Search for duplicate or near-duplicate bills across prior claims, vendors, addresses, and claimants.

That sequence is not meant to turn every adjuster into a forensic examiner. It is a triage routine. The goal is to decide whether the bill belongs in the fast lane or needs a closer look.

A quick example: imagine a homeowner submits a $2,400 invoice for emergency plumbing after a bathroom leak. The company name is real. The logo looks real. The claimant is polite. But the invoice date is two days before the reported loss, the payment account is not linked to the plumbing company, and the final total does not match the tax rate. Any one of those might be explainable. Together, they are the document equivalent of a dog barking at an empty hallway.

How to stop bogus insurance claims without slowing clean ones

The answer is not to make every claimant feel like they are crossing a border checkpoint. That is bad service and, frankly, bad fraud management. The answer is to screen the bill earlier, preserve the evidence, and route only suspicious items with clear reasons.

This is where document-level fraud detection earns its keep. A good screening layer should inspect invoices and receipts before payout for digital edits, Photoshop-style tampering, AI-generated documents, metadata inconsistencies, mathematical irregularities, physical manipulation, duplicates, and payment-context conflicts. It should also explain what it found so a human reviewer can make a defensible decision.

Docklands AI is built for that exact problem. It analyzes claim invoices and receipts for manipulation signals, checks metadata and math, detects AI-generated and altered documents, and uses payment information to build a deeper fraud picture. For claims operations, the practical value is not a shiny score. It is evidence-backed routing: clean documents keep moving, questionable bills go to the right reviewer with the right clues.

The integration piece matters too. Claims teams do not need another island. Docklands AI supports API and webhook integration, real-time reporting and analytics, executive dashboards, multiple users and projects, and security features such as 2FA. In plain English, it can sit inside the workflow instead of becoming another tab everyone forgets to open.

The cultural fix: stop admiring the paperwork

Here is the mindset shift I wish more claims teams would make: a bill is not proof because it has a logo. A receipt is not proof because it has a timestamp. A PDF is not trustworthy because it looks boring.

Boring is the uniform fraud wears when it wants to get paid.

The best fraud teams I have worked with are not cynical. They are disciplined. They assume most claims are legitimate, but they also know which documents deserve a second look. They do not accuse first. They preserve first, compare first, verify first.

That approach protects honest policyholders too. Every bogus insurance claim that slips through eventually shows up somewhere: higher premiums, tighter rules, slower approvals, more friction for the next customer who did nothing wrong. Catching the edited bill early is not about being difficult. It is about keeping trust affordable.

Frequently Asked Questions

What is an edited bill in an insurance claim? An edited bill is an invoice, receipt, estimate, or statement that has been altered after creation. Common changes include totals, dates, line items, vendor details, payee information, and proof-of-payment fields.

Do all edited bills indicate fraud? No. Some edits are legitimate, such as a corrected typo or an amended invoice issued by a vendor. The key is whether the edit is documented, consistent with the timeline, and supported by payment and vendor records.

Why do bogus insurance claims often use bills instead of only photos? Bills translate a claim story into a payout amount. A manipulated photo may support the event, but an edited bill tells the insurer how much to pay, which makes it a high-value target for fraudsters.

Can OCR detect manipulated claim invoices? OCR can extract text from a bill, but extraction is not the same as authentication. To detect manipulation, teams need checks on the original document image, metadata, math, duplicates, and payment context.

Where should insurers screen bills for fraud? The best point is before payout, ideally at document intake or before payment approval. Early screening helps claims teams route suspicious documents without slowing legitimate claims.

See the edited bill before it becomes a paid claim

If your claims team is still relying on manual review to catch one altered number in a stack of routine bills, you are giving fraud a very comfortable chair.

Docklands AI helps insurers detect manipulated, photoshopped, and AI-generated invoices and receipts before they become payouts. Screen claim documents, connect the findings to payment context, and give your reviewers evidence they can actually use.

Because in claims fraud, the smallest edit is often the most expensive one.

Request a Demo Today!

Book your demo below.