Insurance Fraud Car Accident Claims Leave Paper Clues

After a decade around claim files, my hot take is simple: insurance fraud car accident claims usually do not fall apart because someone spots a movie-villain mistake in a crash photo. They fall apart because the tow bill, repair estimate, rental invoice, medical receipt, and payment trail cannot all be true at the same time.

The paperwork is often more honest than the people submitting it. A dented bumper can be photographed from a flattering angle. A PDF can look tidy. But a claim file has a paper shadow, and that shadow gets messy when someone has edited totals, recycled receipts, backdated invoices, or invented a vendor after the fact.

This matters because the financial pressure is real. The FBI estimates non-health insurance fraud costs more than $40 billion each year in the U.S. and adds hundreds of dollars to the average family’s premiums. Car accident claims are a prime hunting ground because they create a believable mess: damage, towing, storage, rentals, repairs, medical visits, and sometimes disputed liability. Plenty of room for creative accounting, which is fraud-speak for someone had too much time and a PDF editor.

Why the paper trail beats the crash photo

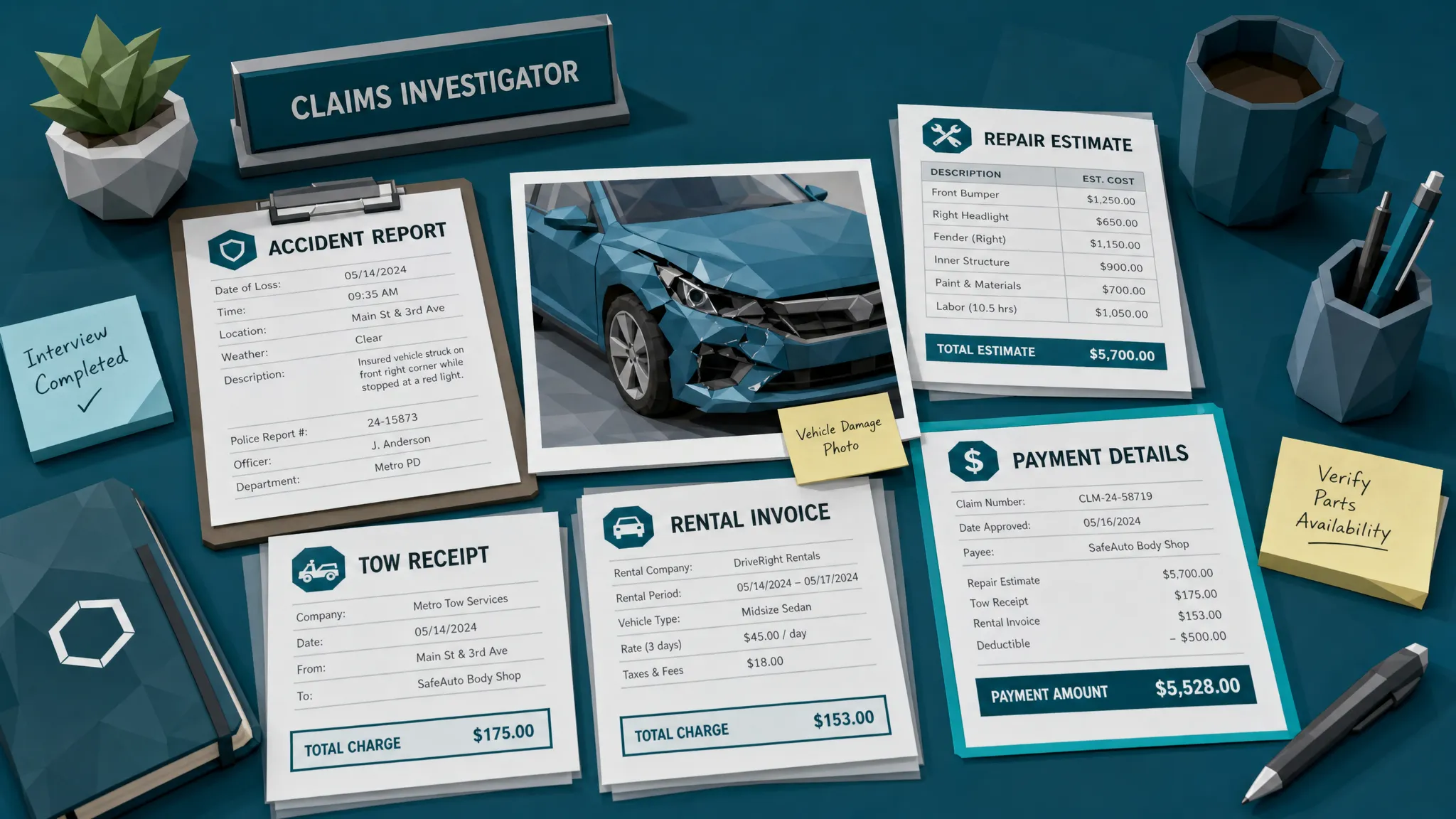

A car accident claim is rarely one document. Even a straightforward fender bender can produce a police report, FNOL notes, photos, a tow receipt, a storage invoice, a body shop estimate, a supplement, a rental bill, payment confirmation, and maybe a medical bill or two.

That pile of documents is where fraud usually leaves fingerprints.

I once reviewed a collision file where the vehicle damage looked plausible. The bumper was cracked, the claimant sounded calm, and the repair estimate was not outrageous. The odd clue was the rental invoice. The rental period started before the accident time recorded in the claim notes. Could it have been a clerical mistake? Sure. But when the tow invoice also had a time stamp that did not fit, the file stopped being routine.

That is the point. A clue is not proof. But a cluster of small document conflicts is exactly what claim managers and SIU teams should care about before payout.

The first paper clue is usually timing

Fraudsters love changing the big number. They are less disciplined with dates and sequence.

In car accident claims, timing clues show up everywhere. A tow receipt may list a pickup before the crash. A repair estimate may have a file creation date before the loss. A rental car invoice may begin too early or extend long after repairs should have been completed. A medical bill may reference a treatment date that does not match the alleged injury timeline.

The trick is to read the documents like a story. If the accident happened at 6:20 p.m., when was the tow called? When did the vehicle arrive at storage? When did the body shop inspect it? When was the estimate generated? When did the claimant submit the invoice? When were payment details added or changed?

Most honest files have a few rough edges. Real life is untidy. But impossible sequencing is different. If the paperwork requires a tow truck to bend time, I start paying attention.

Repair estimates have their own accent

Good body shops have habits. Their estimates tend to use consistent templates, line numbering, labor categories, tax handling, parts descriptions, and supplement language. When a repair invoice has been edited, those habits can wobble.

The common clues are subtle: a total that appears sharper than the rest of the scan, a different font in one line item, spacing that gets tight around the labor amount, or a deductible line that seems pasted in from another document. Sometimes the math is the giveaway. Labor, parts, tax, and fees should add up in a way that matches the jurisdiction and the shop’s normal practice.

One of my favorite boring clues is tax. Fraudsters will inflate the final total but forget that not every line is taxable, or they apply tax to the wrong subtotal. Nobody puts tax math on a poster in the SIU break room, but it catches more nonsense than people expect.

Body shop supplements deserve attention too. A supplement can be legitimate, especially after teardown. But if the supplement conveniently lifts the claim just below an approval threshold, appears from a different template, or changes the payee details along with the amount, that is not a paperwork quirk. That is a review item.

Receipts and invoices must match the payment story

In my view, the payment story is the most underused fraud clue in car accident claims.

A receipt says something was paid. An invoice says something is owed. A payment confirmation says money moved. Those are different things, and fraudsters often blur them together. A claimant may submit an invoice as if it proves payment. A repair facility may be real, but the bank details may route to a personal account. A receipt may show cash paid, while the claimant later asks for direct reimbursement to a different name.

This is where document review should connect to payment information. Does the vendor name match the remit-to name? Does the account holder make sense? Did the claimant change payment instructions late in the claim? Does the amount requested match the amount on the invoice after deductible, tax, depreciation, or prior payment?

Docklands AI focuses heavily on this point because checking whether an image looks real is not enough. The payment details on a claim, expense, or invoice help build a deeper fraud picture. A clean-looking document tied to a suspicious payment path is not clean. It is dressed nicely for court.

Vendor footprints matter in car accident claims

Car accident paperwork often involves third parties: tow yards, storage lots, glass repair shops, medical clinics, rental agencies, cleanup vendors, and sometimes contractors responsible for road debris or parking lot conditions.

I am not saying every unfamiliar vendor is suspicious. Small businesses handle plenty of legitimate work. But the vendor footprint should make sense. Does the business exist where the accident happened? Does the service match the loss? Does the invoice format match the type of work? Does the phone number, address, or payment destination line up with other records?

This gets especially important in claims involving debris, construction zones, commercial properties, or parking facilities. If a Nashville file involves construction debris or parking lot conditions, for example, I would expect the supporting paperwork to line up with local services such as professional street sweeping services in Nashville, site records, incident logs, and cleanup timing. If the story says the lot was professionally maintained but every document points to nobody being on site, that gap deserves a second look.

Again, the clue is not one invoice. The clue is whether the invoice fits the world around it.

AI makes accident fraud prettier, not cleaner

We are seeing a shift in how fake evidence looks. The old days of obvious copy-paste edits are not gone, but they now have company. Fake images, synthetic receipts, and polished-looking PDFs are easier to create than ever.

Admiral told the BBC it had seen a 71% rise in fraudulent claims, with AI-generated fake images and deepfakes contributing to the trend. The Verisk 2025 Fraud Report also points to a growing willingness among some consumers to consider altering claim evidence with AI.

Here is the practical takeaway: AI can make one document look convincing. It struggles to make the whole claim ecosystem coherent.

A generated repair invoice may look polished, but the metadata may be wrong. A fake receipt may have believable typography, but the tax math may be off. A doctored damage photo may look dramatic, but the repair estimate may describe parts that do not match the visible damage. A synthetic medical receipt may have a clinic name, but the payment details may point somewhere else.

That is why claims teams should resist the urge to judge documents only by appearance. Pretty documents can still be fraudulent. Ugly documents can still be legitimate. The evidence is in the relationships between the file, the math, the metadata, and the money.

A practical triage routine for adjusters

When I train claims teams, I do not ask adjusters to become forensic examiners overnight. They have enough to do. I ask them to build a simple rhythm that catches the common paper clues before a suspicious file becomes a paid file.

Use this routine when a car accident claim feels a little too convenient, too expensive, or too heavily documented for the damage described:

- Preserve the original files before converting, compressing, or re-saving them.

- Build a simple timeline from accident time to tow, storage, repair, rental, medical treatment, submission, and payment request.

- Reconcile the payment story by comparing vendor names, remit-to names, account details, paid status, and requested reimbursement.

- Check the math on repair estimates, receipts, taxes, deductibles, storage days, and rental periods.

- Compare documents against prior claims, duplicate submissions, reused templates, and known vendor patterns.

- Escalate with specific evidence, not vibes, because SIU teams need facts they can act on.

That last point matters. Suspicious is not the same as useful. An alert that says this looks weird wastes time. An alert that says the rental invoice starts six hours before the reported accident and the file metadata shows editing after submission gives an investigator a place to begin.

Where Docklands AI fits in the claims workflow

The best fraud controls do not slow every legitimate claimant to a crawl. Most people are telling the truth, and they should not suffer because a minority discovered image editors.

Docklands AI is built for the document layer of that problem. It screens invoices and receipts for signs of manipulation, including photoshopped edits, AI-generated documents, metadata inconsistencies, mathematical irregularities, and physical manipulation. It also uses payment information connected to the claim, expense, or payment to give reviewers a richer fraud picture than a basic is this image real check.

For claims operations, that means suspicious documents can be routed for review with evidence, while cleaner files keep moving. For SIU teams, it means fewer vague referrals and more files with concrete clues. For executives, reporting and analytics help show where fraud risk is entering the process instead of relying on after-the-fact recoveries.

The blunt truth is that car accident fraud is often caught by boring evidence. I mean that as a compliment. Boring evidence is defensible. Boring evidence survives scrutiny. Boring evidence saves money before it leaves the building.

Frequently Asked Questions

What are common signs of insurance fraud in car accident claims? Common signs include inconsistent accident timelines, edited repair estimates, mismatched tow or rental dates, inflated storage charges, duplicate receipts, suspicious vendor details, changed payment instructions, and metadata that conflicts with the claimant’s story.

Can a real car accident still involve fraudulent documents? Yes. A collision can be real while part of the claim is exaggerated or fabricated. Someone may inflate repair costs, extend a rental period, alter a receipt, or submit unrelated damage. Claims teams should separate the validity of the accident from the validity of each supporting document.

Are digitally edited receipts always fraudulent? No. Some documents are legitimately scanned, compressed, annotated, or corrected. The key is context. An edit becomes concerning when it changes financial details, conflicts with metadata, breaks the timeline, or routes payment to an unexpected party.

How can insurers detect AI-generated car accident evidence? Insurers should look beyond visual appearance. Useful checks include image consistency, file metadata, edit history, duplicate patterns, math validation, vendor verification, and payment-context review. AI-generated evidence often looks plausible in isolation but conflicts with surrounding documents.

Where should document screening happen in the claims process? Screening should happen as early as possible after document intake and again before payout if new invoices, receipts, or payment details are added. Early screening helps adjusters keep clean claims moving while routing high-risk files to SIU with evidence.

Put the paper clues to work

If your team handles car accident claims, you do not need another spreadsheet full of suspicion. You need faster ways to identify which invoices, receipts, estimates, and payment details deserve human attention.

Docklands AI helps claims teams detect manipulated, photoshopped, and AI-generated documents before payout, with document forensics and payment-context checks designed for real claims workflows. If the paperwork is already leaving clues, we can help you read them before the money moves.

Request a Demo Today!

Book your demo below.