Public Adjuster Scams and the Documents Behind Them

After 10 years poking holes in claim files, I’ve learned to distrust one sentence more than almost any other: the paperwork looks fine.

That sentence is where money leaks. Public adjuster scams rarely announce themselves with a crooked logo or a cartoon villain in a hard hat. They usually arrive as a tidy bundle of documents: a signed representation agreement, a polished estimate, a few contractor invoices, some receipts, photos of damage, and a payment instruction that feels urgent but reasonable.

Here’s my hot take: the public adjuster is often the least interesting part of a suspicious file. The documents around the adjuster tell the better story.

And that story matters. Insurance fraud is not a rounding error. The FBI warns that insurance fraud adds an estimated $400 to $700 a year to the average family’s premiums. Meanwhile, digital manipulation is getting easier. The BBC reported that Admiral saw a 71% rise in fraudulent claims, with fake images and edited evidence playing a larger role. For claims leaders, SIU teams, and adjusters, the lesson is blunt: if we only review the claim narrative, we miss the paper trail doing the dirty work.

What public adjuster scams are, and what they are not

Let’s be fair up front. Public adjusters are not inherently suspicious. Many are licensed professionals who help policyholders document losses, interpret coverage, and negotiate complicated property claims. After major storms, fires, or water losses, a good public adjuster can keep a chaotic claim from turning into a paperwork bonfire.

Public adjuster scams happen when that role is abused. Sometimes the person is unlicensed or misrepresents authority. Sometimes a legitimate adjuster is surrounded by questionable contractors or inflated documentation. Sometimes the scam is less about the adjuster personally and more about the ecosystem: restoration vendor, estimator, invoice submitter, payee, and claimant all creating a file that looks complete enough to push toward payment.

That distinction matters. We should not treat every public adjuster-led claim like a crime scene. But we should treat every supporting document as evidence, because evidence has a funny habit of contradicting itself.

The documents behind most public adjuster scams

When people talk about public adjuster scams, they usually focus on behavior: door knocking after storms, aggressive promises, high fees, or pressure to sign quickly. Those are worth watching, but documents are where the scheme becomes payable.

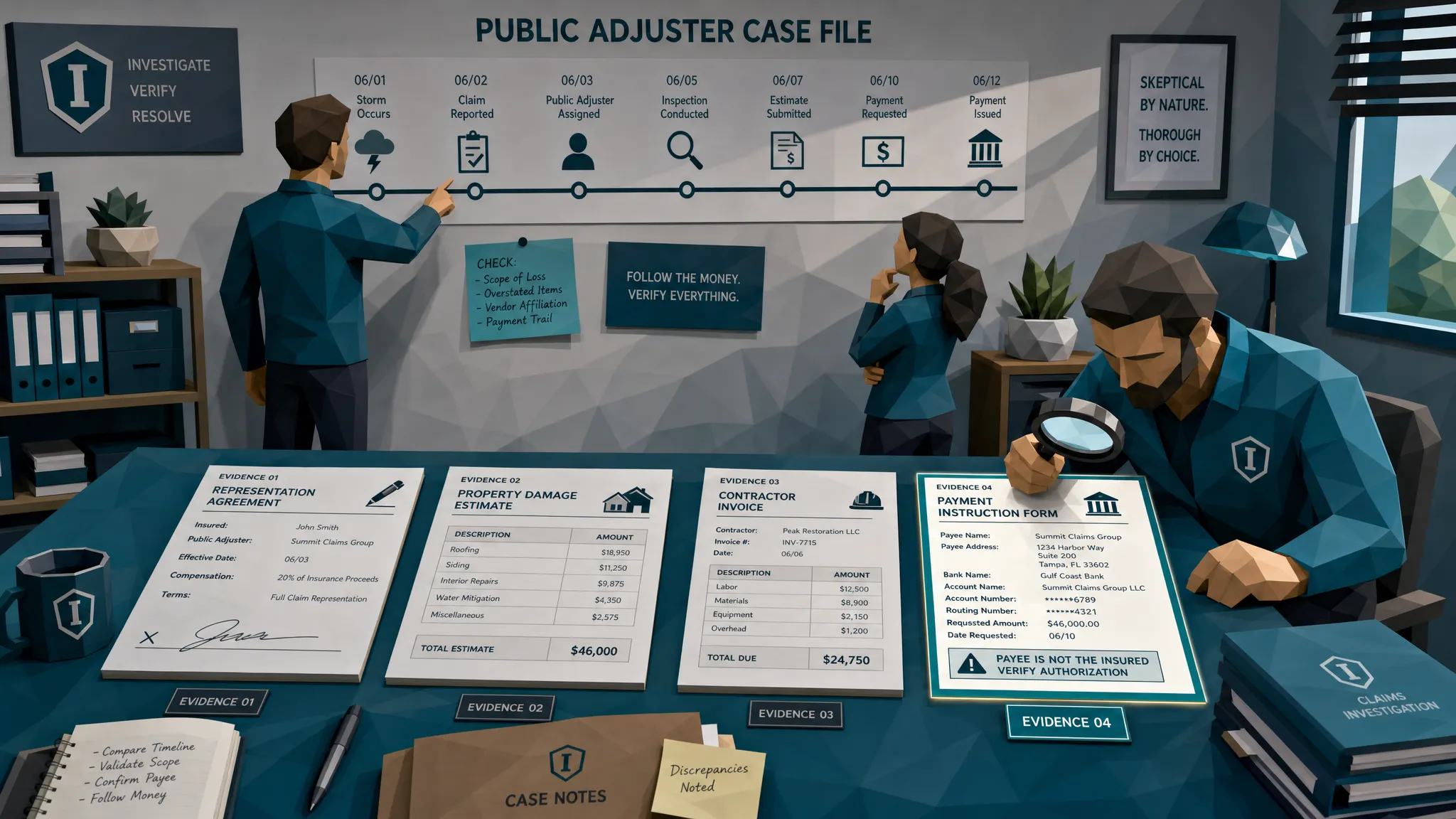

A suspicious claim file often has several document types working together. One document creates authority. Another inflates damage. Another justifies the payment. Another redirects the money. If each document is reviewed in isolation, the file may pass. When reviewed together, the seams start showing.

The representation agreement that arrives too neatly

The first document to inspect is often the public adjuster agreement or letter of representation. This is the document that says who can speak for the policyholder and sometimes who may receive communications or payment.

The red flags are not always dramatic. I look for signatures that appear copied from another file, dates that do not match the claim timeline, missing required disclosures, odd fee language, and versions that seem to have been rescanned several times. A representation agreement signed at 9:00 a.m. on the same day as a full roof estimate, contractor invoice, and damage photo set should make reviewers pause. Either everyone involved is incredibly efficient, or the file was assembled like a sandwich at lunch rush.

I once reviewed a storm claim where the representation agreement was dated before the reported date of loss. Nobody noticed because the estimate total was the exciting part. The date mismatch was boring, which is exactly why it mattered.

Estimates that look professional but do not breathe

A professional-looking estimate can lull a claims team into comfort. The layout looks familiar. The line items look technical. The total is precise down to the cent. Lovely.

Then you compare it to the photos and the loss facts.

Common problems include rooms that do not match the property layout, quantities that exceed the visible damage, repeated line items, debris removal that appears twice, or supplements that inflate the claim without new evidence. I have seen a modest kitchen become 430 square feet on paper, which would have made it larger than my first apartment. That is not an estimating nuance. That is a document telling on itself.

The most suspicious estimates often avoid cartoonish overbilling. They stay just close enough to plausible. That is why math checks, line-item consistency, and comparison against the rest of the file matter more than a quick glance at the total.

Contractor invoices that support a story too perfectly

Contractor invoices are a favorite supporting actor in public adjuster scams. They can make an inflated estimate look like real work was completed or scheduled.

The basic invoice details matter: vendor name, address, license number, tax information, invoice date, payment terms, and remit-to details. But the better clues sit in the relationship between the invoice and everything else. Does the invoice reference work not visible in the photos? Does the vendor show up across multiple unrelated claims with similar formatting? Does the invoice look newly created even though it claims to document older work? Does the payee differ from the contractor named elsewhere in the file?

One of my simplest habits is to compare the invoice language against the estimate language. Fraudsters love copy and paste. If a contractor invoice mirrors the public adjuster estimate line for line, including the same odd abbreviations, I want to know why.

Receipts that fill gaps in the claim narrative

Receipts are often used to prove temporary repairs, emergency mitigation, materials purchases, lodging, equipment rental, or replacement items. They are also easy to edit, easy to generate, and easy to submit as low-friction evidence.

A suspicious receipt may have inconsistent fonts, strange spacing around totals, tax math that does not reconcile, missing payment details, or metadata showing it was edited after submission. Physical manipulation also happens: printed receipt, handwritten change, photo taken, PDF attached. That chain can strip useful context while making the item look old-fashioned and harmless.

My favorite receipt red flag, if favorite is the right word, is the receipt that is blurrier exactly where the total and date appear. Apparently, cameras only get emotional around reimbursement values.

Damage photos that do not match the paperwork

Photos are powerful because they feel direct. The adjuster sees damage, the claimant sees damage, the carrier sees damage. Done.

Not quite.

Photos can be reused, staged, cropped, or edited. They can show damage from another property, another date, or another claim. With AI-generated and digitally manipulated images becoming more common, photo evidence deserves the same disciplined review as invoices and receipts. Verisk’s 2025 fraud research found that carriers are seeing more sophisticated claims manipulation, which matches what many of us feel in the trenches.

The key is not to ask whether a photo looks real. Ask whether it fits. Does it match the estimate? Does it match the reported peril? Does the image metadata align with the inspection timeline? Are the same shingles, floorboards, or background objects showing up in unrelated claims?

Payment instructions that quietly change the risk

If I could make every claims team put a sticky note on their monitor, it would say: follow the money before you admire the documents.

Public adjuster scams often involve payment instructions that deserve scrutiny: assignment of benefits, direction-to-pay forms, contractor payment authorizations, updated mailing addresses, bank details, or settlement instructions. The document may be legitimate in form but risky in context.

Late-stage payee changes are especially important. A claim that looked routine for weeks can become high risk when payment is redirected to a new entity, a third-party contractor, or an account that does not match the documented vendor relationship. That does not prove fraud. It does mean the file should leave the fast lane.

The vendor footprint can be useful, but it can also fool you

Claims teams often check whether a contractor or adjuster has a website, reviews, social media, or a business address. That is sensible. A vendor with no footprint is a question mark.

But a polished online presence is not proof of legitimacy. Anyone can look established quickly. I like a good website as much as the next person, and legitimate businesses often use agencies offering web design and SEO services to reach customers. That proves marketing effort, not that the invoice, estimate, or payment instruction is authentic.

The better vendor review asks: does the digital footprint match the claim activity? A roofing contractor that suddenly appears across 18 claims after a hailstorm is not automatically suspicious. A roofing contractor with a new domain, reused invoice templates, inconsistent addresses, and payment routed to a different entity deserves a closer look.

Where public adjuster scams usually fall apart

The files that worry me most are not messy. They are too smooth. Everything is attached, every document supports the next document, and every question has a ready answer. Good fraud operators understand workflow. They know a complete file moves faster.

So we need to review for contradiction, not ugliness.

The strongest signals usually appear across the file:

- Timeline conflicts, such as invoices dated before inspection, photos taken after repairs allegedly occurred, or representation documents signed before the loss was reported.

- Visual tampering, including pasted totals, inconsistent compression, unusual blur, mismatched fonts, or signs that a PDF or image was modified.

- Metadata anomalies, such as edit histories, software traces, timestamps, GPS data, or missing metadata that conflicts with how the document was supposedly created.

- Mathematical irregularities, including tax errors, subtotals that do not add up, duplicate line items, or estimate quantities that do not fit the property.

- Duplicate or near-duplicate documents, especially receipts, invoices, photos, and templates reused across claims.

- Payment-context mismatches, such as a vendor named in the invoice but a different payee in the payment instruction.

None of these signals alone should trigger a dramatic fraud accusation. This is claims, not a courtroom TV show. But two or three of them together can turn a routine claim into a meaningful SIU referral.

A practical review workflow for claims teams

The goal is not to slow every claim. Clean claims should move. Policyholders with real losses should not wait because someone else figured out how to abuse a PDF editor.

The goal is to separate clean files from evidence-rich exceptions early enough to prevent bad payouts.

Preserve the original documents

Always keep the original submitted file when possible. Do not rely only on screenshots, compressed email previews, or OCR-extracted fields. The original image or PDF may contain metadata, compression patterns, editing traces, and layout clues that disappear when the file is converted.

If your workflow strips files down to text fields, you may be throwing away the very evidence that would explain the fraud.

Verify authority before negotiating substance

Before spending time on estimate disputes, verify who has authority to speak and receive information. Check the public adjuster’s license through the relevant state insurance department. Confirm the policyholder actually signed the agreement. Use trusted contact information already on file, not the phone number conveniently provided in the suspicious packet.

This step is boring. Boring controls save money.

Compare documents as a set

Do not review the estimate, invoice, photos, receipts, and payment forms as separate chores. Put them in conversation with each other. The estimate says drywall in three rooms. The photos show one room. The invoice bills emergency mitigation before the reported date of loss. The payment form names a company that does not appear anywhere else.

That is not a paperwork quirk. That is a claim file asking for supervision.

Route by evidence, not suspicion

A weak alert says suspicious public adjuster. A useful alert says invoice total appears visually altered, receipt metadata shows editing after submission, estimate quantities conflict with photos, and payment request names an unrelated entity.

SIU teams need evidence they can act on. Claims handlers need clear reasons to pause a file. Executives need reporting that separates real risk from reviewer anxiety. Everyone wins when the alert explains what broke.

How Docklands AI helps with the document side of the problem

Docklands AI is built for the part of public adjuster scams that tends to hide in plain sight: invoices, receipts, and supporting claim documents that look acceptable until they are inspected more deeply.

We help claims teams detect photoshopped, manipulated, and AI-generated documents using document forensics and fraud analysis. That includes tampering detection, metadata forensics, mathematical irregularity checks, physical manipulation detection, and review of payment information to build a deeper fraud picture. The point is not to replace adjusters or SIU investigators. The point is to give them better evidence before payment leaves the building.

For high-volume claims operations, the operational fit matters as much as the detection. Docklands AI supports API and webhook integration, real-time reporting and analytics, executive dashboards, multiple users and projects, and 2FA security. In plain English, that means suspicious documents can be screened inside the workflow instead of becoming another manual queue that everyone promises to check later.

Public adjuster scams are document problems as much as conduct problems. If the file is where the money moves, the file is where the defense should start.

Frequently Asked Questions

Are public adjusters scams by default? No. Many public adjusters are legitimate, licensed professionals who help policyholders navigate complex claims. The risk comes from unlicensed actors, inflated documentation, forged authority, questionable contractor networks, or manipulated claim evidence.

What documents are most important in public adjuster scam reviews? Start with the representation agreement, estimate, contractor invoices, receipts, damage photos, authorization forms, and payment instructions. The strongest clues often appear when these documents contradict each other.

What is the fastest red flag to check? Compare the timeline. Dates on the loss notice, representation agreement, inspection, photos, invoices, and payment forms should make sense together. Impossible timing is one of the easiest ways a polished file falls apart.

Can OCR detect these scams? OCR can extract text, totals, dates, and vendor names, but it does not prove the document is authentic. Claims teams need document-level checks that inspect visual tampering, metadata, math, duplicates, and payment context.

When should SIU get involved? SIU should get involved when there are specific, documented inconsistencies such as altered invoice areas, metadata conflicts, duplicate photos, mismatched payees, forged authority, or estimate details that do not match the loss evidence.

Stop treating clean paperwork as clean evidence

If public adjuster scams are showing up in your claims leakage, the answer is not to distrust every public adjuster. The answer is to stop letting polished documents move unchallenged through the payout path.

Docklands AI helps insurance teams screen invoices, receipts, and claim documents for manipulation, AI-generated evidence, metadata issues, math problems, physical tampering, and payment-context mismatches before funds go out. If you want to see what your current process is missing, visit Docklands AI and request a demo.

Request a Demo Today!

Book your demo below.