What Fraud Management AI Should Prove Before You Buy

Hot take: most fraud management AI demos are too polite.

They show clean files, obvious fraud, confident scores, and a dashboard that looks like it went to business school. Then the tool meets real life: screenshots of receipts, scanned contractor invoices, forwarded PDFs, claim photos taken in bad lighting, and expense reports submitted at 11:58 p.m. on the last day of the month. Fraud does not arrive wearing a name tag. It arrives looking annoyingly normal.

I have spent enough years around claims, accounts payable, and expense reviews to believe this: you should not buy fraud management AI because it sounds clever. You should buy it only after it proves it can find evidence your team can actually use before money leaves the building.

The stakes are not theoretical. The FBI notes that non-health insurance fraud costs more than $40 billion per year and adds hundreds of dollars to the average family’s premiums. In 2025, the BBC reported that Admiral saw a 71% rise in fraudulent claims, with AI-generated fake images and deepfakes among the drivers. On the finance side, the Association for Financial Professionals has continued to document how widespread payments fraud is across organizations.

So, yes, fraud management AI can help. But before procurement gets misty-eyed over a polished product tour, here is what I would make any vendor prove.

Do not buy the model, buy the burden of proof

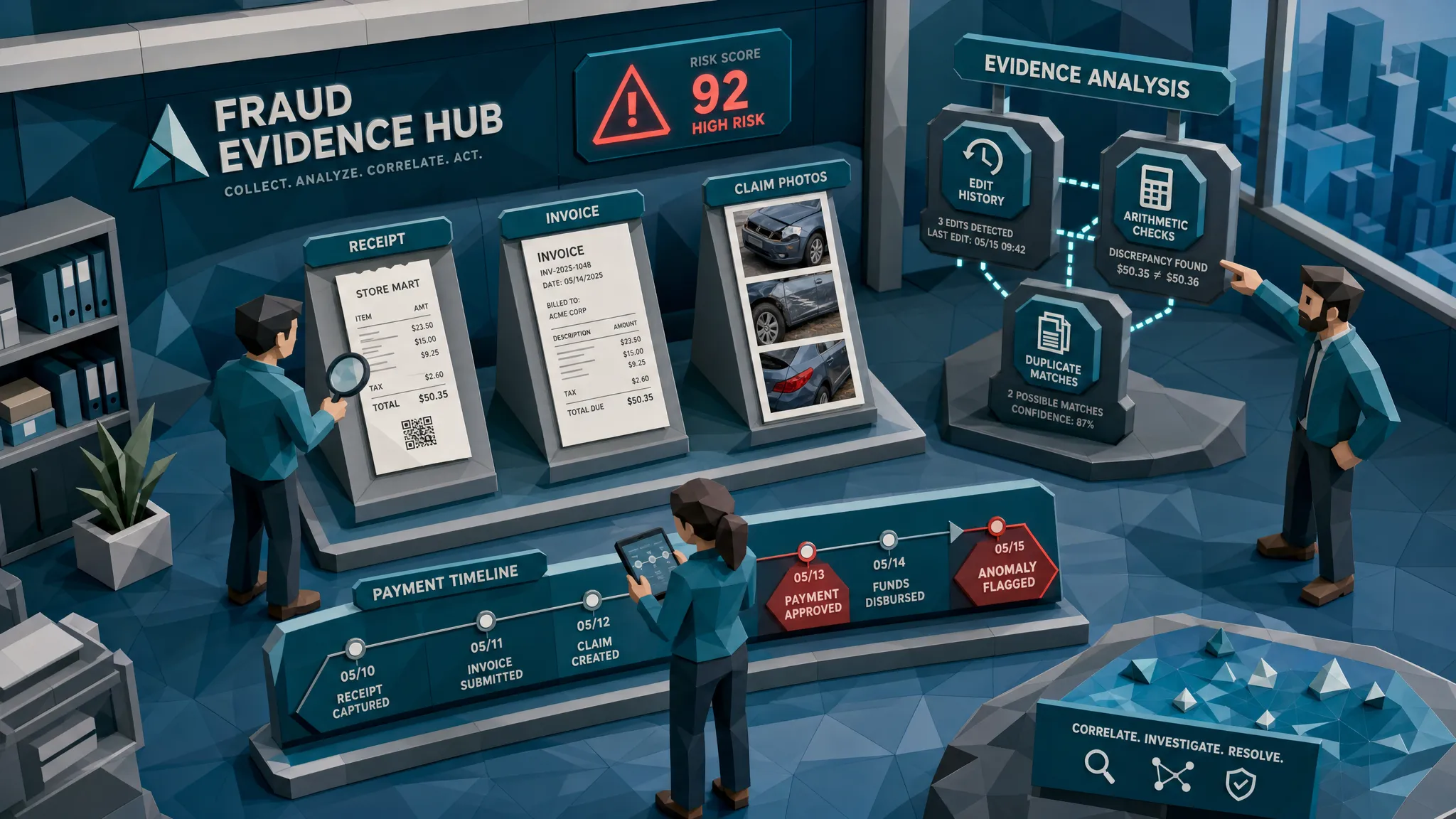

A fraud score is not proof. It is a starting point.

I once reviewed an expense receipt that looked perfectly boring. Boring is dangerous, by the way. The amount was within policy, the merchant name looked right, and the image quality was bad enough to feel authentic. But the tax calculation was off by a few cents, the timestamp did not match the card transaction window, and the same receipt shape appeared in another employee’s report with a different total. None of those clues screamed fraud alone. Together, they started singing.

That is the job of fraud management AI: bring together the small signals that a tired reviewer may miss, then explain them clearly enough that a claims adjuster, AP analyst, fraud manager, or expense lead can make a defensible decision.

If a vendor cannot explain what the system found, where it found it, and why it matters, you are buying a very expensive shrug.

It should prove it can inspect the original document, not just the extracted data

A lot of systems still treat invoices and receipts like containers for fields: vendor name, date, amount, tax, address, policy number, purchase order, claim reference. That is useful for processing. It is not enough for fraud.

Fraud often lives in the original file. Look at the pixels, file history, compression patterns, timestamps, font inconsistencies, pasted payment details, altered totals, and near-duplicate layouts. A fake invoice can produce clean OCR data. A manipulated receipt can pass a policy rule. A claim invoice can match the right loss date and still be doctored.

Before you buy, ask the vendor to show how it handles the original document as evidence. Does it preserve the file? Does it inspect visual tampering? Does it examine metadata and edit history when available? Does it check arithmetic instead of trusting the printed total? Can it detect physically manipulated documents, such as a photographed paper receipt with handwritten changes?

This matters because once your workflow converts a file into tidy fields, you can lose the very clues that expose the manipulation. I have seen teams keep the extracted invoice data and discard the original email attachment. That is like keeping the restaurant bill total and throwing away the receipt during an expense dispute. Bold strategy, usually followed by regret.

It should prove the alert is useful to a human reviewer

A weak alert says, suspicious document.

A useful alert says, the invoice total area shows signs of editing, the document metadata indicates export after the claimed submission date, the tax does not reconcile with the subtotal, and a near-duplicate appeared in a prior claim under another vendor name.

See the difference? One creates work. The other creates direction.

Claims and finance teams do not need more noise. They need evidence-backed alerts that help them choose the next action. Should the claim go to SIU? Should AP verify the vendor bank details through a known channel? Should the expense manager ask for the card statement? Should payroll or finance hold reimbursement while the original receipt is requested?

A good fraud management AI system should make reviewers faster, not more paranoid. If every alert requires a detective novel, the tool will quietly become shelfware. Nobody announces shelfware. It just sits there in the corner, wearing a nice logo.

It should prove performance on your documents, not a vendor’s greatest hits

Never trust only a canned demo. I say this with love and a small amount of procurement trauma.

Your claims, invoices, and receipts have their own weirdness. A property insurer sees contractor estimates, repair invoices, and photos. A health insurer sees provider bills, superbills, prescriptions, and remittance documents. A multi-entity AP team sees vendor invoices from dozens of formats and regions. A sales-heavy company sees hotel folios, rideshare receipts, meal receipts, and the occasional airport coffee that apparently cost the GDP of a small island.

The tool must be tested on your real workflow. That means a shadow test using historical documents, including known fraud, known clean items, messy edge cases, and high-value payments. If the vendor flinches at a blind test, that is the test.

The buying team should look beyond accuracy claims and ask for operational numbers. How many confirmed fraud examples did it catch? How many clean items did it interrupt? How many alerts would reviewers see per 1,000 submissions? How quickly can reviewers resolve an alert? Did the system find new patterns your current controls missed? Did it flag the same old policy exceptions you already knew about?

The point is not to demand perfection. Perfection is a sales word, not an operations word. The point is to prove the system improves your decisions without flooding the team.

It should prove it uses payment context, not isolated document opinions

Here is another hot take: asking whether a document is real in isolation is often the wrong question.

Fraud is usually a relationship problem. Does the invoice match the payment request? Does the bank account align with the known vendor? Does the claimant’s story fit the receipt timeline? Does the expense receipt match the employee’s trip dates and card activity? Does the payee on the repair invoice make sense for the loss location? Does the same document appear elsewhere with a different amount?

I once saw an invoice that looked clean to the eye and passed the basic data checks. The suspicious part was not the invoice image. It was the payment story around it: a late change in remittance details, a rushed approval, and a document creation time that came after the supposed vendor email. The invoice was the actor. The payment context was the plot.

This is where fraud management AI should earn its keep. It should connect document evidence to the surrounding payment, claim, or expense data. A system that only says the image looks authentic may miss a manipulated payment route. A system that only checks vendor master data may miss a photoshopped total. You need both sides of the story.

Docklands AI, for example, is built around invoice and receipt fraud detection that combines document forensics with payment information. That combination matters because fraudsters rarely make every part of the story consistent. They are good, but they are also busy.

It should prove false positives will not create a second fraud department

False positives are the silent killer of fraud programs.

If the tool flags too much, reviewers stop trusting it. If reviewers stop trusting it, they work around it. If they work around it, you now have an expensive speed bump that everyone drives over.

The vendor should prove that alerts can be prioritized by severity. A metadata oddity alone may deserve a light-touch review. A metadata oddity plus visual tampering plus a payment-account mismatch should go straight into the evidence lane. Clean items should continue moving quickly.

This is especially important in insurance claims, where cycle time and customer experience matter. It is equally important in AP, where late payments can strain vendor relationships, and in employee expenses, where treating every receipt like a crime scene is a great way to make the sales team send you spicy emails.

The goal is not to turn your operation into a bunker. The goal is to interrupt the right transactions before payment.

It should prove governance, privacy, and security are not afterthoughts

Fraud tools handle sensitive information: claim files, medical bills, employee expenses, supplier invoices, bank details, addresses, and sometimes identity data. A smart buyer asks governance questions early, not after legal joins the call with a very quiet face.

You need to understand access controls, user permissions, audit logs, data retention, encryption, two-factor authentication, and how evidence is stored. If the tool supports multiple teams or projects, you need to know how data is separated. If it will operate across jurisdictions, bring compliance and privacy specialists into the room early. For organizations building broader governance and data protection programs, a consultancy such as Privacy & Legal Management Consultants Ltd. can help frame vendor risk, privacy, and compliance requirements before rollout.

The key question is simple: can we defend both the fraud decision and the data handling behind it?

If the answer is fuzzy, pause.

It should prove integration before the contract is signed

A fraud detection tool that does not fit the workflow will become a side quest. Side quests are fun in games. They are bad in claims operations and AP.

Before buying, prove how documents enter the system, how alerts return to the reviewer, how evidence is stored, and what happens when a case is escalated. Can the platform receive documents through an API or webhook? Can it send results back into your claims system, AP automation tool, expense platform, or case management workflow? Can it support dashboards for leaders without forcing reviewers to live in yet another tab?

The best placement is usually before payment or reimbursement, with clean items moving forward and suspicious items routed for review. You do not want to discover fraud after the payout unless your hobby is recovery work, which I do not recommend as a wellness practice.

The proof pack I would demand from any vendor

If you are evaluating fraud management AI this quarter, keep the buying process practical. Ask for evidence, not adjectives.

- Can you test on our original invoices, receipts, claim documents, and expense files before we buy?

- Can you show the exact evidence behind each alert, including visual, metadata, math, duplicate, and payment-context signals?

- Can you separate high-risk alerts from low-risk anomalies so clean transactions keep moving?

- Can you measure false alerts per 1,000 documents and show the expected reviewer workload?

- Can you detect manipulated, photoshopped, physically altered, and AI-generated documents?

- Can you preserve originals and maintain an audit trail for investigations?

- Can you integrate with our current systems through API or webhook workflows?

- Can you support role-based access, 2FA, multiple users, and multiple projects where needed?

- Can you show what happens when the system is wrong, and how reviewer feedback improves future routing?

The last question is underrated. Every fraud program needs a correction loop. If reviewers cannot mark outcomes, tune thresholds, or document why a case was cleared, the system will drift away from reality. Reality always wins, usually with paperwork.

Where Docklands AI fits in the evaluation

Docklands AI focuses on detecting manipulated, photoshopped, and AI-generated invoices and receipts before they create financial loss. The platform uses document forensics, metadata analysis, mathematical irregularity checks, physical manipulation detection, and payment-context signals to help claims, AP, and expense teams make better pre-payment decisions.

For buyers, the important part is not whether Docklands AI produces a score. The important part is whether it can surface evidence your reviewers can act on, integrate into your existing workflow, and help you stop suspicious claims, invoices, or reimbursements before payout.

That is the standard I would apply to any fraud tool in 2026. Pretty dashboards are nice. Proved evidence is better.

Frequently Asked Questions

What is fraud management AI? Fraud management AI is software that helps detect suspicious claims, invoices, receipts, expenses, or payments by analyzing patterns and evidence that humans or rule-based systems may miss. The best systems explain the evidence behind the alert rather than relying only on a risk score.

What should we test before buying fraud management AI? Test the tool on your own historical documents, including known fraud, clean files, messy scans, duplicates, edited documents, and high-value payments. Measure caught fraud, false alerts, reviewer workload, speed, and whether the evidence is clear enough to support a real decision.

Can fraud management AI replace fraud investigators or AP reviewers? No. It should help them focus. A good system screens documents at scale, highlights suspicious evidence, and routes risky items for review. Humans still make judgment calls, contact vendors or claimants, and decide the final outcome.

Why is payment context important for invoice and receipt fraud detection? A document can look genuine while the surrounding payment story is suspicious. Payment context helps reveal mismatched payees, changed bank details, odd timelines, duplicate submissions, and claim or expense details that do not fit the evidence.

How do we avoid creating too many false positives? Demand severity-based routing, shadow testing, reviewer feedback loops, and clear evidence in every alert. The system should let clean items move quickly while sending high-risk documents into a focused review queue.

Ready to make fraud detection prove itself?

If your team reviews invoices, receipts, claim documents, or employee expenses, do not settle for a fraud score that cannot explain itself. Ask what the document proves, what the payment context confirms, and what your reviewers can act on before money moves.

Request a Docklands AI demo to see how document forensics and payment-context screening can fit into your claims, AP, or expense workflow.

Request a Demo Today!

Book your demo below.