Why Predictive Claim Models Miss Edited Evidence

If you have ever watched a predictive claim model give a tidy, low-risk score to a claim with a doctored receipt attached, you learn two things fast. First, the model is not stupid. Second, the fraudster was playing a different game.

Here is my hot take: predictive claim models get blamed for misses that were never in their field of view. Most of them are excellent at spotting suspicious claim patterns. They are far less reliable when the fraud lives inside the evidence itself, in a changed invoice total, a pasted payment line, a recycled receipt, or a photo that has been quietly edited before upload.

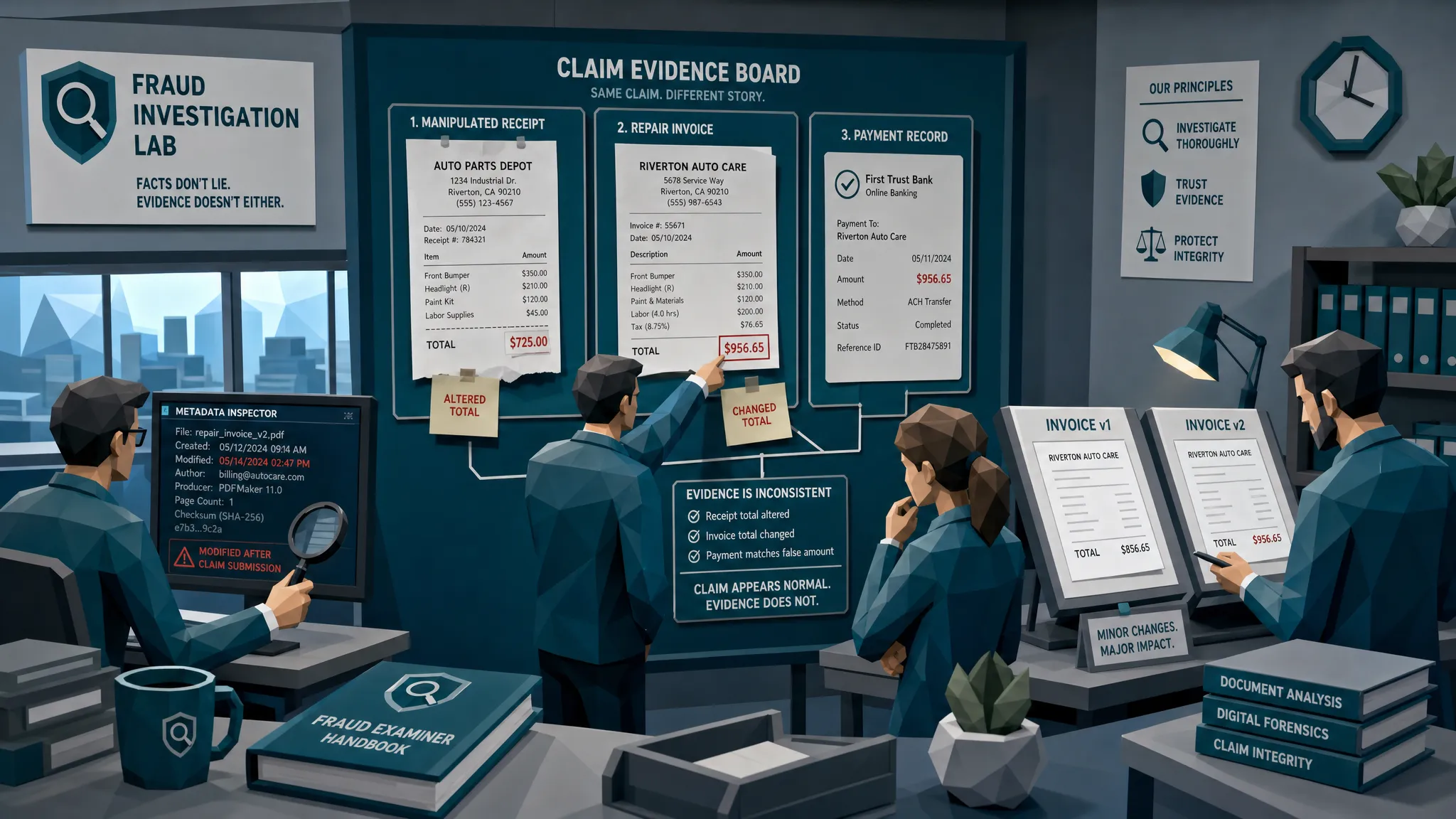

I have seen this more times than I care to admit. One property claim I reviewed years ago looked boring enough to make coffee nervous. The policyholder had a normal history, the loss amount sat within the expected band, the vendor looked plausible, and the timeline did not scream fraud. The predictive claim model shrugged. But the repair invoice had a total that had been edited after the original file was created. Different compression around the numbers. Slight font mismatch. Payment details that did not line up with the rest of the claim. The model saw an ordinary claim. The document told a very different story.

That gap matters more in 2026 because edited evidence has become cheap, fast, and annoyingly convincing.

What predictive claim models actually do well

Predictive claim models are useful. I am not here to throw them into the sea, although some days in fraud ops make that tempting.

A good model can look at claim history, policy data, claimant behavior, geography, loss type, provider patterns, settlement ranges, prior claims, network relationships, and timing. It can identify claims that resemble known bad behavior. It can prioritize workloads for adjusters and SIU teams. It can help separate routine claims from claims that deserve a closer look.

That is valuable. In a high-volume claims environment, nobody wants every cracked phone screen, water leak, or windshield chip sent to a senior investigator. Predictive scoring helps claims teams move faster and focus attention where it is most likely to matter.

The problem starts when teams expect a model built on structured claim data to answer a forensic question: is the invoice, receipt, estimate, image, or bank proof genuine?

That is a different question.

A predictive model may know whether the claim amount is unusual. It may know whether the vendor has appeared in prior questionable claims. It may know whether the claimant filed too soon after policy inception. But unless the workflow inspects the original evidence, the model may never see the clues that matter most.

Why edited evidence slips through

Edited evidence hides in the original file, not in the extracted fields.

When an invoice is uploaded, many claims systems quickly convert it into clean data. OCR extracts the vendor name, date, total, line items, tax, and maybe an invoice number. The workflow then compares those fields against rules or expected values. If everything looks reasonable, the document often becomes a supporting attachment rather than an active piece of evidence.

That is where fraud gets comfortable.

A changed total can still be within a normal repair range. A backdated receipt can still match the claimed loss window. A fake supplier invoice can still include a valid-looking address and tax calculation. A doctored photo can still support the general story. Once the system turns the document into neat fields, the messy forensic signals are easy to lose.

I like to describe this as ironing a wrinkled shirt before checking whether the stain was blood or ketchup. The document comes out looking structured and searchable, but you may have flattened the very clues you needed.

Common edited evidence in claims includes altered repair invoices, inflated receipts, swapped payment details, reused documents from older claims, synthetic receipts, edited medical bills, manipulated timestamps, and AI-generated supporting images. Some are clumsy. Some are polished. The polished ones are the ones that make predictive claim models look bad.

The fraud environment has changed

Insurance fraud has always been expensive, but the tools have changed. The FBI notes that insurance fraud contributes to higher premiums, with estimated costs of hundreds of dollars per year for the average family. That is the boring public-service version. The operational version is simpler: every bad document that gets paid trains fraudsters to try again.

The rise of easy editing tools and generative media has made the evidence problem worse. The BBC reported a sharp rise in fraudulent claims linked to AI-generated fake images and deepfakes. Verisk's 2025 Fraud Report also pointed to a worrying consumer willingness, especially among younger respondents, to alter claim evidence using AI tools.

That does not mean every young claimant is plotting in a hoodie under neon lighting. Please do not make that your fraud strategy. It means the barrier to producing convincing false evidence is lower than it used to be.

A fraudster no longer needs advanced design skills to change a receipt. They can use a phone app, a browser tool, or a template. The output may pass a quick human glance and a basic OCR check. If the claim story itself looks normal, a predictive model may not object.

Predictive models score the claim, not the truth of the evidence

This is the core issue.

A predictive claim model typically asks: based on what we know, how likely is this claim to be problematic?

Edited evidence asks: is this specific document what it claims to be?

Those questions overlap, but they are not the same. A low-risk customer can submit a manipulated receipt. A legitimate loss can include an inflated invoice. A real repair can be paired with a fake estimate. A known vendor can have one document edited by a claimant before submission.

I once reviewed a claim where the event was real, the damage was real, and the claimant probably would have been paid anyway. The fraud was in the extra few hundred dollars added to the receipt. That sort of case is easy to miss because the model is looking for a suspicious claim, while the actual problem is a suspicious document.

This is why I get twitchy when teams say, our model already handles fraud. Maybe it handles some fraud. Maybe it handles a lot of fraud. But if it does not inspect the evidence, it has a blind spot big enough to park a courtesy car in.

The provenance lesson claims teams should borrow

Fraud control gets easier when evidence is tied to provenance. In other words, where did this thing come from, what changed, and can we verify the chain behind it?

You see this mindset outside insurance too. In research procurement, for example, suppliers build trust by tying products to batch records, test results, and certificates of analysis. A supplier such as batch-tested research peptides illustrates the broader principle: evidence is stronger when it connects back to verifiable source material, not just a polished final document.

Claims evidence deserves the same treatment. A receipt is not trustworthy because it looks like a receipt. An invoice is not reliable because the fields parse cleanly. A photo is not true because it matches the claimant's story. The question is whether the evidence holds up when you inspect its origin, edits, math, duplicates, and payment context.

That is where predictive models need help.

What document forensics adds to predictive claim models

The fix is not to replace predictive claim models. The fix is to stop asking them to do a job they were not built to do.

Document forensics gives claims teams a second layer of review focused on the submitted evidence itself. It looks for signs that an invoice, receipt, image, estimate, or proof of payment has been altered, generated, reused, or physically manipulated.

Visual inspection at the pixel level can surface pasted text, inconsistent compression, mismatched fonts, irregular spacing, strange shadows, or areas that have been blurred and resaved. Metadata analysis can reveal file history, timestamps, software traces, missing device information, or impossible timing. Mathematical checks can catch totals, tax, discounts, and line items that do not reconcile. Duplicate detection can find reused receipts that have been cropped, renamed, or slightly edited. Payment-context analysis can compare the document against payee details, bank information, claimant history, vendor behavior, and the surrounding claim story.

That last part is especially important. A generic image check might say a document looks suspicious. A claims-aware fraud review asks a better question: suspicious compared with what this claim says happened?

For example, an invoice might look fine visually, but the bank account does not match the vendor history. A hotel receipt might have clean formatting, but the payment card, stay dates, and claim timeline do not line up. A repair estimate might have plausible totals, but the same layout appears across multiple unrelated claims with tiny variations. That is where document evidence and payment context together become much harder to fool.

Why edited evidence creates false confidence

The dangerous misses are rarely cartoonish. They are not neon signs saying fraud here, please investigate. They are usually ordinary-looking documents in ordinary-looking claims.

A predictive score can create false confidence when reviewers treat it as a truth label rather than a prioritization tool. Low risk becomes approved. Medium risk becomes maybe later. High risk becomes SIU. That works until fraudsters learn to make the claim data look boring while hiding the manipulation in the attachment.

Fraudsters adapt to thresholds. If claims above $5,000 receive more scrutiny, they submit $4,850. If new vendors get questioned, they mimic a familiar vendor. If certain loss types are heavily modeled, they choose common, low-drama scenarios. If the model weighs claimant history heavily, first-time or otherwise clean claimants can slip through with edited documents.

That does not make predictive models useless. It means teams need to separate probability from proof.

A model can say, this claim looks low risk. Document forensics can say, this invoice has signs of editing around the total, the metadata indicates post-loss modification, and the payment details conflict with prior vendor records. One helps prioritize. The other gives the reviewer something defensible to act on.

A better workflow for claims teams

The practical answer is early evidence screening. Do it before payout, before the claim becomes expensive to unwind, and before the suspicious document gets buried inside a closed file.

First, preserve original uploads wherever possible. Screenshots, compressed PDFs, and forwarded files often strip away useful clues. If your workflow destroys metadata at intake, you have already made the review harder.

Second, screen documents before relying on extracted fields. OCR is useful for workflow efficiency, but it should not be treated as fraud detection. You want the original file inspected for tampering, file history, math, duplicates, and physical manipulation before the payment decision is made.

Third, connect document findings to claim and payment context. A suspicious pixel pattern matters more when it appears around the invoice total. Missing metadata matters more when the claimant says the photo was taken at the scene. A payee mismatch matters more when it appears alongside a recently edited document.

Fourth, route by evidence, not vague suspicion. Reviewers do not need another black-box risk score with a dramatic color gradient. They need a clear reason: total appears edited, tax does not reconcile, duplicate found in prior claim, file was modified after submission, payment details conflict with vendor record. That is the kind of alert an adjuster or SIU analyst can actually use.

Finally, keep clean claims moving. The goal is not to turn claims operations into airport security for receipts. The goal is to let normal claims pass while edited evidence gets paused with enough detail for a fast decision.

Where Docklands AI fits

Docklands AI is built for this gap: detecting manipulated, photoshopped, and AI-generated invoices and receipts before they become paid losses.

The platform combines document fraud detection with forensic analysis, including tampering detection, metadata review, mathematical irregularity checks, physical manipulation signals, and AI-generated document detection. It also uses payment information from a claim, expense, or payment to build a fuller fraud picture, which is where many generic document checks fall short.

For claims teams, that means predictive claim models can keep doing what they do well, while Docklands AI inspects the evidence those models often miss. The workflow can sit alongside existing systems through API and webhook integrations, with reporting and analytics for fraud and claims leaders who need to see patterns over time.

The best version of this setup is simple. Predictive scoring tells you which claims look risky based on history and behavior. Document forensics tells you whether the submitted evidence itself can be trusted. Put those together and you get fewer blind spots, fewer weak referrals, and a much better shot at stopping edited evidence before payout.

Frequently Asked Questions

Do predictive claim models detect edited invoices and receipts? Sometimes they may flag claim patterns related to edited evidence, but they usually do not inspect the original document for pixel changes, metadata conflicts, math issues, duplicates, or physical manipulation unless those checks are specifically added.

Why does OCR miss edited claim evidence? OCR extracts text and fields. It is designed to read documents, not prove they are authentic. If a fraudster edits a total cleanly, OCR may simply read the new total and pass it into the claims workflow as normal data.

Should insurers replace predictive models with document forensics? No. Predictive models are valuable for triage and pattern detection. Document forensics complements them by checking whether the submitted evidence has been altered, reused, generated, or contradicted by payment context.

What types of claim documents should be screened? Invoices, receipts, estimates, proof-of-payment images, repair documents, medical bills, photos, and any document that influences payout should be screened when fraud risk or payment value justifies it.

How can claims teams reduce false positives? Tie every alert to specific evidence. A useful review should explain what was found, where it appears, and why it matters in the context of the claim. Vague risk labels create noise. Evidence-based alerts create decisions.

Make predictive claim models harder to fool

Predictive claim models are still worth using. I would not run a modern claims operation without them. But if edited evidence is slipping through, the answer is not another rule about suspicious totals or yet another dashboard that makes everyone feel watched.

The answer is to inspect the documents before payout and connect what you find to the payment story.

If your claims team wants to catch manipulated invoices, edited receipts, AI-generated documents, and payment-context mismatches before they cost money, talk to Docklands AI. We help claims and fraud teams add evidence-led document screening to the workflows they already use, so clean claims keep moving and suspicious evidence gets the attention it deserves.

Request a Demo Today!

Book your demo below.