How False Insurance Claim Evidence Falls Apart Under Review

Here’s my mildly unfashionable opinion after a decade in fraud work: most false insurance claim evidence does not collapse because one heroic reviewer spots a cartoonishly fake receipt. It collapses because the story cannot carry its own groceries.

The invoice says one thing. The photo says another. The payment trail shrugs in the corner. Metadata quietly raises its hand. By the time you compare all of it, the claim has not exploded, it has simply run out of excuses.

That matters because the money involved is not pocket change. The FBI estimates insurance fraud costs the United States more than $308 billion each year, adding hundreds of dollars to annual premiums for the average family. And the evidence problem is getting sharper. In 2025, the BBC reported that Admiral saw a 71% rise in fraudulent claims, with fake images and digitally altered evidence playing a growing role.

My hot take: the best review teams do not ask, “Does this look fake?” They ask, “Does this evidence survive being compared with itself?” That is where a false insurance claim usually starts to wobble.

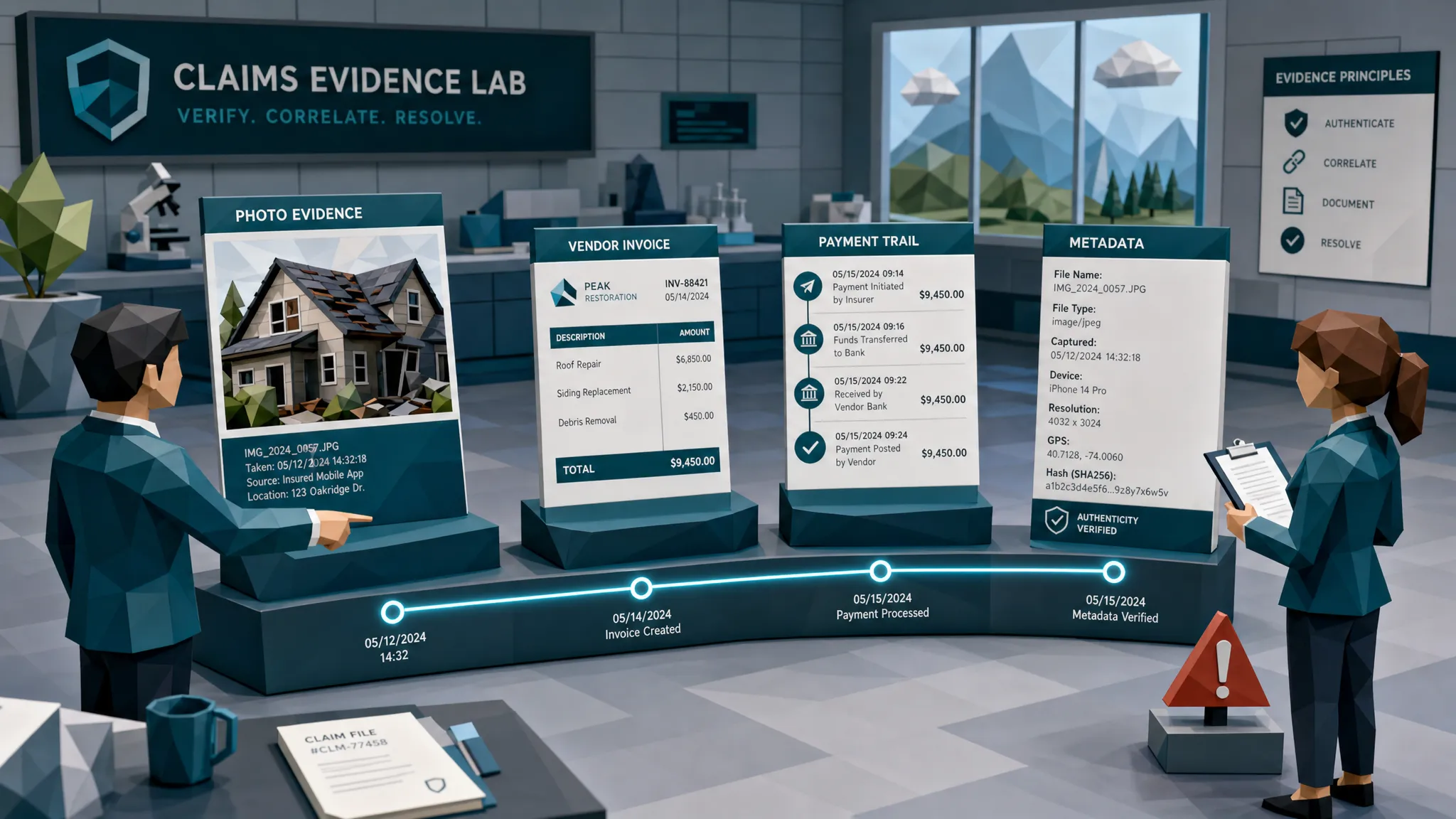

The first crack is usually the timeline

False evidence loves a tidy timeline. Real life, as anyone who has handled property claims after a storm knows, is messier. Contractors are late. Receipts arrive out of order. Photos are taken on phones, forwarded by relatives, compressed by messaging apps, and uploaded three days after everyone has forgotten the exact sequence.

That messiness is not fraud. In fact, normal messiness can be reassuring. What worries me is evidence that is too conveniently aligned until one hidden timestamp ruins the party.

I once reviewed a water damage claim where the repair invoice looked clean, professional, and painfully ordinary. Nothing about the layout screamed fake. But the claimant’s photos suggested the damaged area had already been stripped before the contractor supposedly inspected it. Then the invoice file showed a creation date after the claimant said it had been emailed. One oddity would not have bothered me. Three timeline contradictions in a row? That is when the coffee gets interesting.

A false insurance claim often tries to use one document to prove too many things at once: ownership, damage, repair cost, date of loss, and urgency. Under review, each of those claims gets pulled apart. If the receipt predates the item’s release, if the repair estimate references damage not visible in photos, or if the bank payment happens before the invoice was supposedly issued, the story starts losing bolts.

Photos fail when the scene has no physics

Digital photos are persuasive because they feel immediate. A cracked TV, a flooded kitchen, a smashed pendant light, a damaged roof tile, we see it and our brains want to move on. Fraudsters know this. They do not need a masterpiece. They need a reviewer in a hurry.

But photos have habits. Shadows should agree with lighting. Reflections should make sense. Edges should not blur differently around the damaged area than around the rest of the scene. Compression artifacts should not cluster only around the expensive item. If a photo has been stitched, generated, or heavily edited, it may still look fine at thumbnail size, but the physics often complain.

The newer wrinkle is image generation. Verisk’s 2025 fraud report found that carriers increasingly see more sophisticated claim manipulation. I would describe the day-to-day version less elegantly: the pictures are getting prettier, but the surrounding paperwork is still sloppy.

That is the useful part. A generated photo might show a damaged appliance, but does it match the invoice model? Does the room match prior inspection photos? Does the claimed purchase date match the product’s availability? Does the payment evidence show the claimant ever bought it? A photo can be impressive and still be lonely.

Receipts and invoices break on small arithmetic

In my experience, people overestimate how often fraud is caught by spotting a bad logo. They underestimate how often it is caught by tax math that is off by $3.17.

Receipts and invoices are full of tiny rules. Sales tax rates, VAT treatment, subtotal rounding, service charges, disposal fees, invoice numbering, merchant addresses, line item formats, SKU conventions, payment references, and refund indicators all create a fingerprint. A real vendor may make mistakes, of course. But fake evidence often gets the headline amount right and the boring parts wrong.

For a contents claim, the claimed item also needs to exist in the real market. If someone claims a high-end chandelier, I expect the model, price bracket, retailer type, and product category to make sense. I might compare the claimed item against manufacturer pages, prior purchase records, or legitimate retail catalogs such as modern lighting categories like pendant lamps and chandeliers before I accept a suspiciously convenient receipt with a pasted logo and no product trail.

This is not about price policing every lamp, sofa, laptop, or medical device. It is about asking whether the document behaves like it came from a real transaction. Real receipts have context. Fake ones often have decoration.

Payment details are the boring witness that lies less

If documents are actors, payment details are the stage crew. Nobody notices them until the set falls down.

This is where many false claim files start to look tired. The receipt shows card ending 4821, but the claimant’s bank screenshot shows a different payment method. The invoice names one repairer, but payment went to an unrelated individual. The proof of payment is a cropped banking screenshot with no beneficiary, no settled status, and no reference. The claimant says the vendor was paid immediately, but the invoice terms show 30 days and the bank evidence shows nothing.

I am not saying every mismatch is fraud. Families use shared cards. Contractors use trading names. Some perfectly honest people submit dreadful screenshots because, frankly, bank apps were not designed for claims evidence.

But payment context is powerful because it tests the document against behavior. A false insurance claim may produce a nice invoice. It may produce a nice photo. It is harder to produce a believable payment trail that lines up with vendor identity, claim timing, document metadata, invoice amount, and the claimant’s explanation.

This is also why simple image checks are not enough. Asking whether a receipt image looks real is a start. Asking whether the payment information supports the receipt is much better.

Metadata is a witness, not the judge

Metadata has a glamorous reputation in fraud conversations, which is funny because most metadata looks like it was designed to punish people who enjoy reading. File creation dates, modification history, GPS coordinates, device identifiers, software tags, and upload paths can all help explain where a document has been.

The trick is not to overplay it.

Missing metadata does not prove fraud. Many platforms strip it automatically. A claimant may take a screenshot because the original PDF was too large. A broker may scan documents into one combined file. Legitimate claims often arrive looking like they have survived a small administrative war.

Still, metadata can expose contradictions. A repair invoice supposedly emailed by a vendor may show signs of being created on the claimant’s device. A receipt photo may carry GPS data from a location nowhere near the stated purchase. A PDF may show editing software used after the claim was submitted. A file may have been created minutes before upload despite representing a purchase from months earlier.

By itself, metadata is rarely the whole case. Combined with image clues, math issues, duplicate patterns, and payment mismatches, it becomes a very useful witness.

Vendor details reveal whether the business is real enough

False evidence often uses vendor names the way teenagers use fake IDs: confidently, but with limited follow-through.

A repairer’s invoice might have a mobile number but no business footprint. A clinic bill might use a provider address that belongs to a coworking space. A contractor invoice might show bank details changed from prior claims. A receipt might show a merchant name that does not match the payment descriptor. In warranty claims, I have seen documents where the supposed service center did not repair that brand at all.

Again, real businesses can be messy. Small tradespeople are not always administrative poets. But there is a difference between scruffy and fictional.

A good review looks for commercial gravity. Does the vendor exist? Does the address make sense? Does the tax registration, phone number, email domain, invoice sequence, and payment beneficiary form a coherent business? If not, the document may still look professional while the vendor story quietly evaporates.

Duplicates expose the production line

One fraudulent receipt can be convincing. Fifty fraudulent receipts often start looking related.

Duplicate and near-duplicate evidence is one of the most underappreciated ways a false insurance claim falls apart. Fraudsters reuse templates, crop old documents, change dates, alter totals, and resubmit similar files across different claims. They may not realize that a stain, fold mark, barcode pattern, background texture, or invoice layout can connect documents that have different names and amounts.

This is where volume helps the insurer, if the insurer can actually compare files at scale. Manual reviewers are good at noticing the same receipt twice in the same claim. They are not built to remember a near-identical repair invoice from six months ago in another region. Software can help here by comparing visual patterns and document structure, then surfacing likely matches for human review.

Fraud has a handwriting. It just takes patience, and enough document memory, to read it.

The review mistake I see too often

The most common mistake is treating claim evidence like a beauty contest. Clean receipt? Pass. Professional invoice? Pass. Clear photo? Pass. Nice banking screenshot? Pass.

That is exactly how bad evidence gets through. A false insurance claim does not need every document to be perfect. It only needs each reviewer to inspect one piece in isolation.

The better approach is boring and ruthless: compare everything. The photo should agree with the invoice. The invoice should agree with the payment. The payment should agree with the vendor. The vendor should agree with the claimant’s story. The timeline should agree with all of it.

When I train newer reviewers, I tell them to stop hunting for a smoking gun and start looking for a committee of small liars. One oddity may be explainable. Five independent oddities pointing in the same direction deserve attention.

A practical review flow that does not punish honest claimants

Fraud review has a public relations problem because nobody wants legitimate claimants treated like suspects. Fair. The goal is not to make everyone prove they are innocent. The goal is to avoid paying claims where the evidence cannot support the payment.

Start by preserving original files wherever possible. Forwarded screenshots and compressed PDFs lose clues. If the claim later goes to SIU, you want the earliest version, not the tenth-generation copy that has been resized, renamed, and emailed through three inboxes.

Next, test chronology before aesthetics. Date of loss, date of purchase, date of repair, file creation date, payment date, and upload date should not need a detective novel to reconcile. If the timeline is plausible, keep going. If it is not, document the inconsistency clearly.

Then compare document content with payment context. The amount, beneficiary, merchant descriptor, payment method, and settlement status should support the receipt or invoice. If the claimant cannot provide payment proof, that does not automatically mean fraud, but it changes the confidence level.

Finally, route exceptions with evidence rather than suspicion. A note that says “looks fake” is weak. A note that says “invoice total does not reconcile to line items, file shows post-submission edit, and payment beneficiary differs from named vendor” gives SIU something useful.

Where Docklands AI fits into this review

This is the part where I resist the urge to pretend technology replaces experienced adjusters. It does not. Good fraud detection supports human judgment. Bad fraud detection creates a noisy queue and calls it innovation.

Docklands AI is built for the evidence problem we have been talking about: manipulated, photoshopped, and AI-generated invoices and receipts in claims, accounts payable, and expenses. For insurance teams, it can screen claim documents for signs of visual tampering, metadata issues, mathematical irregularities, physical manipulation, and payment-context mismatches. It also supports API and webhook integration, reporting, dashboards, multiple users, and project workflows.

The practical value is consistency. Every claim handler has busy days. Every SIU has capacity limits. A screening layer helps compare the original document, the file history, the math, the visual evidence, and the payment story before money leaves the building.

If you want a deeper operational view, we have also written about screening invoices and receipts before you pay. The short version is simple: clean claims should move quickly, and suspicious evidence should arrive at review with specific reasons attached.

Frequently Asked Questions

What is false insurance claim evidence? False insurance claim evidence is any document, photo, invoice, receipt, estimate, or payment proof that has been fabricated, altered, recycled, or misrepresented to support a claim. It may be fully fake, or it may be a real document changed to inflate value, shift dates, or support damage that did not happen as described.

Can a false insurance claim document look genuine? Yes. Many questionable documents look normal at first glance. The stronger clues often appear when you compare the document with metadata, payment details, vendor identity, claim chronology, and other submitted evidence.

Is missing metadata enough to deny a claim? No. Missing metadata can happen for legitimate reasons, including screenshots, scans, email forwarding, and platform compression. It becomes more meaningful when combined with other issues, such as timeline conflicts, visual edits, duplicate documents, or payment mismatches.

What should adjusters do when evidence looks suspicious? Preserve the original file, document the specific inconsistency, compare it against payment and vendor context, and escalate according to your claims policy. Avoid vague notes like “fake receipt.” Evidence-led notes are more useful and more defensible.

Can automated screening replace SIU review? No. Automated screening should help prioritize and explain risk, not make final fraud decisions in isolation. The best use is to surface document-level evidence so claims handlers and SIU teams can review suspicious items faster and more consistently.

Make false evidence work harder

False claim evidence rarely survives disciplined comparison. The receipt has to match the payment. The invoice has to match the vendor. The photo has to match the damage story. The metadata has to avoid contradicting the timeline. That is a lot of plates to keep spinning.

If your claims team wants to catch manipulated invoices, altered receipts, and AI-generated evidence before payout, Docklands AI can help you add forensic document screening to your review workflow without replacing the systems your team already uses.

Request a Demo Today!

Book your demo below.