Insurance Claims AI Fraud Still Leaves Paper Trails

AI has made insurance fraud look cleaner. That is the part everyone keeps talking about. The fake receipt no longer has the wrong font. The staged damage photo no longer screams “bad Photoshop.” The repair estimate can sound like it came from a real garage because, frankly, it often sounds better than the real garages I have dealt with.

But here is my slightly unfashionable opinion after a decade around fraud teams: insurance claims AI fraud is not harder because the evidence looks real. It is harder because too many teams still inspect one document at a time.

The paper trail is still there. It is just less likely to be a coffee stain, a crooked scan, or a misspelled supplier name. Today, the trail is in the timing, the payment details, the file history, the math, the vendor behavior, and the tiny disagreements between documents that were never meant to be read together.

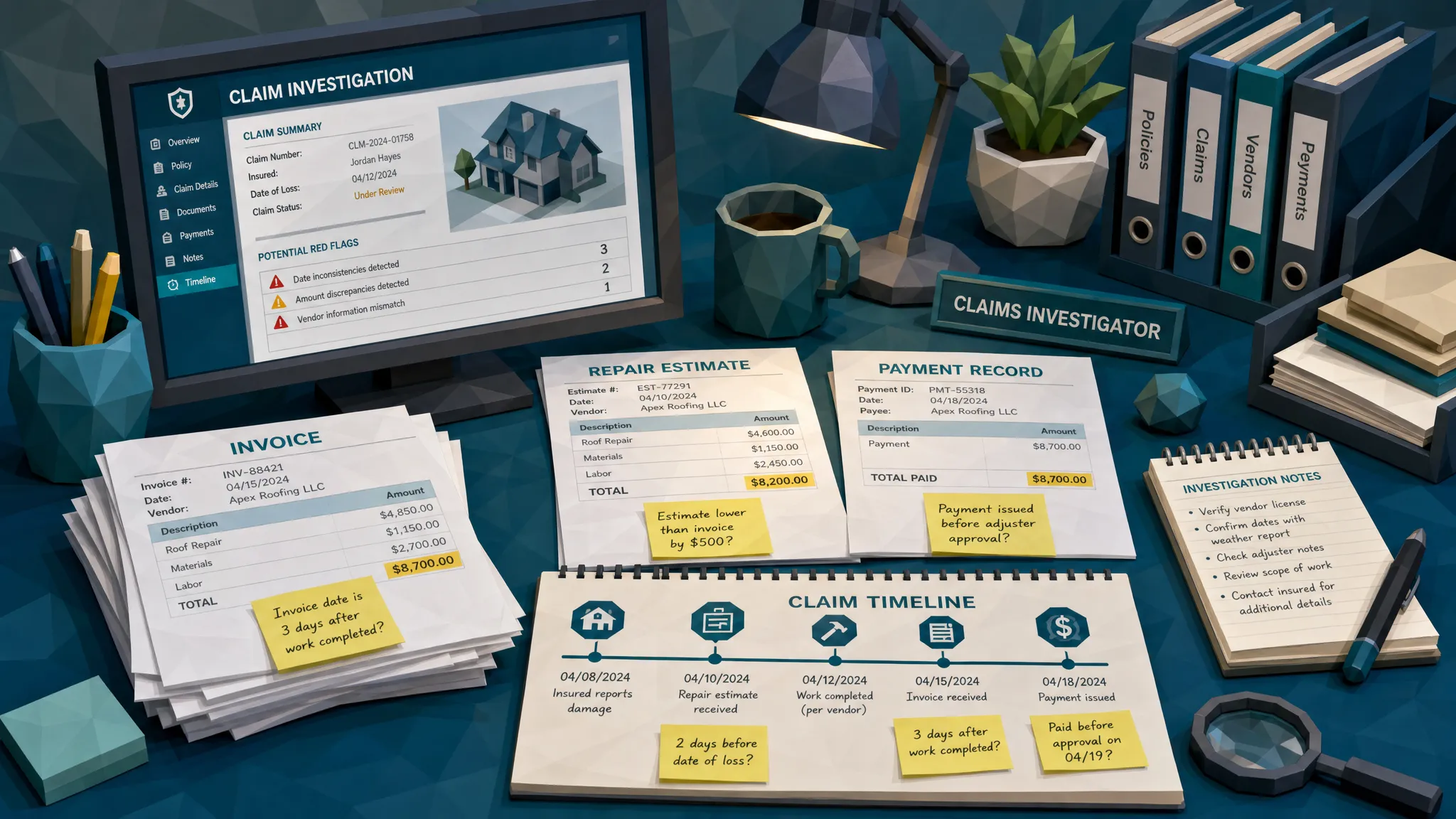

I once reviewed a property claim where the invoice looked flawless. Logo, VAT details, item descriptions, bank account, everything seemed tidy. The issue was not the invoice. The issue was that the “emergency repair” payment details matched a vendor used in three unrelated claims across different addresses, and the invoice creation time came after the claim handler had already received it. The document looked innocent. The timeline did not.

That is where modern claims fraud detection gets interesting.

The AI Fraud Panic Is Real, but It Is Also Misleading

Let’s be honest, the panic is not coming from nowhere. The FBI estimates insurance fraud costs the United States more than $308 billion per year, adding hundreds of dollars to annual premiums for the average family. In the UK, insurers have also reported a sharp rise in suspicious claims, with BBC coverage of Admiral data pointing to AI-generated images and deepfakes as emerging drivers.

And consumer behavior is changing. Verisk’s 2025 fraud research found a worrying generational gap, including higher willingness among younger consumers to consider altering claim evidence with AI. That does not mean an entire generation is out there fabricating burst pipes on their lunch break. It does mean the barrier to entry has collapsed.

Ten years ago, a claimant needed some skill to alter an invoice convincingly. Now they need a prompt, a phone, and mild overconfidence.

Still, AI does not remove the messy reality around a claim. A fraudulent claim has to survive a whole ecosystem of facts. It has to match policy dates, incident dates, repair timelines, supplier norms, payment details, photos, emails, claim notes, adjuster activity, bank records, and often the claimant’s own previous behavior.

That is a lot of places to trip.

My Hot Take: AI Makes Better Props, Not Better Stories

Most fake claim evidence fails because the story around it is weak.

A receipt may look authentic, but the vendor may not sell that item. A repair estimate may be formatted perfectly, but the labor rate may be wrong for the region. A hotel invoice for a travel disruption claim may pass a visual check, but the payment card may not line up with the claimant’s usual behavior. A damage photo may look plausible, but the metadata may show it was generated, edited, stripped, or created after the supporting invoice.

That is why I keep telling claims leaders not to obsess over “Can we spot the fake image?” as a single question. It is useful, but incomplete.

The better question is: Does this evidence behave like it belongs to this claim?

That shift matters. A claim is not a folder full of independent documents. It is a narrative with receipts attached. Fraudsters are often good at improving one page. They are much worse at making every surrounding detail agree.

Docklands has covered this broader point before in relation to how AI-generated fraud can still slip through the documents themselves, but in insurance claims the stakes are especially high because the document is rarely alone. It sits inside a chain of decisions and payments.

The Paper Trail Has Gone Digital, but It Has Not Disappeared

When I say “paper trail,” I do not mean paper. Half the claims I see now involve PDFs, screenshots, app exports, phone photos, email attachments, and supplier portals. The trail is digital, but the principle is the same: every action leaves context.

The first clue is often time.

A suspicious claim might include an invoice dated before the incident, a repair estimate created after the reimbursement request, or a receipt timestamp that clashes with business hours. In auto claims, you may see towing, repair, rental, and medical documents that cannot all be true at the same time. In property claims, the date of a contractor invoice may not match the reported discovery date, weather event, or inspection note.

The second clue is money.

This is where many generic document checks fall short. A fake invoice is not just an image problem. It is a payment problem. The bank details, payee name, amount, currency, tax calculation, duplicate account usage, and settlement instruction can all tell a deeper story.

If the same payment account appears across multiple unrelated claimants, I want to know. If a supplier bank account changes right before a payout, I want to know. If a repair invoice amount is just under an approval threshold, repeatedly, I really want to know.

That is one reason insurance claims AI fraud should be investigated through the claim and payment context, not just the uploaded file. A beautiful fake document can still point to an ugly payment pattern.

The Best Clues Are Often Boring

Fraud work is not always dramatic. Most days, it is not a thriller. It is closer to noticing that the milk in the fridge expires before the grocery receipt says it was bought.

The boring clues are the useful ones.

A manipulated invoice might have perfect branding but inconsistent tax math. A fake repair receipt might use a supplier address that belongs to a storage unit. A medical bill might have a provider name that does not match the payment recipient. A warranty claim might include a purchase receipt where the serial number formatting does not match the manufacturer’s pattern.

None of these details prove fraud by themselves. That is important. A flag is not an accusation. But when several boring details line up, the picture changes quickly.

I have seen claims where the document image passed manual review because it looked neat, but the underlying PDF showed signs of editing. I have seen receipts where the item prices added correctly, but the subtotal and tax were mathematically impossible. I have seen invoices where the “supplier” appeared legitimate until we noticed the same bank details on several claims that should have had no connection.

Fraudsters love the visible layer. Investigators should love the boring layer.

Why Visual Review Alone Is Now a Trap

Manual review has always had value. Good adjusters and SIU analysts develop instincts that no checklist can fully capture. I am not here to insult the seasoned handler who can smell a suspicious claim before the second coffee.

But the volume and quality of AI-assisted evidence has changed the economics of review. If your process depends on a human noticing that a receipt “looks off,” you are asking people to win a game that has moved past appearances.

McKinsey has estimated that insurers lose tens of billions annually to claims fraud, while only a fraction of fraudulent claims are detected. Whether your exact book of business is above or below that benchmark, the operational problem is familiar: too many claims, too many documents, too little time.

Visual checks are especially weak when fraudsters submit evidence that is technically plausible. A receipt can be clean. A PDF can be tidy. A damage photo can be convincing. The question is whether the evidence holds up when you compare it against the claim story, payment behavior, file properties, and known fraud patterns.

That is where document forensics and claim-level detection need to work together. We have written about this balance in insurance claim fraud detection models versus document forensics, because neither approach is enough on its own. Models can flag suspicious claims. Forensics can interrogate the evidence. Together, they help teams move from suspicion to something more defensible.

What I Would Look For First in a Suspected AI Claim

If I were advising a claims team tomorrow morning, I would not start by telling them to buy the shiniest fake-image detector and call it a day. I would ask where their current process loses context.

Are documents reviewed separately from payments? Are receipts checked without vendor history? Are adjuster notes disconnected from file metadata? Are claim handlers expected to catch manipulated documents while also meeting cycle-time targets?

The practical review should focus on a few core questions:

- Does the document’s creation, modification, and submission timeline make sense?

- Do the payment details match the named supplier, claimant, and claim history?

- Do totals, tax, discounts, quantities, and unit prices behave like real billing?

- Does the document format match what that vendor or provider usually issues?

- Are there duplicates, near-duplicates, or repeated patterns across claims?

- Has the image or PDF been edited, regenerated, compressed oddly, or stripped of useful history?

That list is not glamorous, but it catches real issues. More importantly, it gives SIU and claims teams a cleaner basis for escalation. “This receipt looks fake” is a weak hand. “This receipt was created after submission, has impossible tax math, and shares payment details with two unrelated claims” is a much better conversation.

Payment Context Is the Underrated Fraud Signal

Here is the part I think many carriers still underweight: the money trail often tells the truth before the document does.

A fake invoice is built to persuade a human. Payment details are built to receive funds. That makes them harder to fake cleanly at scale, because fraudsters eventually reuse accounts, names, addresses, patterns, or tactics.

In claims, this matters across multiple lines. In home insurance, contractors and emergency repair vendors can be abused. In auto, repair shops, towing, storage, and rental documentation create many payment touchpoints. In health and warranty claims, provider or merchant identity can be the weak point. In employee or travel-related claims, receipts may be fabricated while the reimbursement destination remains very real.

This is why Docklands AI looks beyond the question of whether a document or image appears real. The platform uses claim, expense, or payment information to build a deeper fraud picture, combining signals such as AI-generated document detection, tampering detection, metadata forensics, mathematical irregularities, and payment context.

That approach reflects how fraud actually works. The document is the costume. The payment is the motive.

Be Careful: Better Detection Should Not Mean More False Accusations

There is a real risk in the current market. Everyone is suddenly selling certainty. “This is AI.” “This is fake.” “This is fraud.” I get why that sounds attractive, but claims teams need to be more disciplined than that.

A stripped metadata field can happen for innocent reasons. A claimant may screenshot a receipt because that is what their phone made easy. A contractor may use ugly invoice software. A PDF may be compressed by an email system. Weird does not always mean fraudulent.

The goal is not to punish weird documents. The goal is to identify clusters of evidence that deserve review.

Good fraud detection should help teams prioritize, not replace judgment. It should reduce noise, explain why something is suspicious, and give investigators a clear trail to follow. It should also help honest claimants get paid faster by moving low-risk claims through with less friction.

That last point matters. Fraud controls that slow every claim create their own kind of loss. The best systems make the suspicious claims more visible without treating everyone like a suspect.

The Future of Insurance Claims AI Fraud Is Messier, Not Magic

I do not think we are heading into a world where every claim is fake and every receipt is a deepfake. That makes for good conference drama, but poor operating strategy.

What we are heading into is a world where mediocre fraud looks much better than it used to. The bad actors who once submitted laughably altered receipts can now submit clean, plausible evidence. That raises the floor.

But the ceiling is still limited by context. Fraudsters must still make the document match the claim, the payment, the timing, the vendor, the math, the policy, and the real world. They must make the story hold together under pressure.

Most do not.

For claims leaders, the opportunity is to stop treating AI fraud as a visual authenticity problem only. Treat it as a paper trail problem, updated for 2026. Bring together document forensics, payment analysis, claim history, vendor intelligence, and human investigation. The answer is not more paranoia. It is better linkage.

AI may write a cleaner invoice. It may generate a sharper photo. It may even mimic the tone of a real supplier.

But it still leaves receipts. In this business, that is rather convenient.

Frequently Asked Questions

What is insurance claims AI fraud? Insurance claims AI fraud involves using AI tools to create, alter, or enhance claim evidence such as receipts, invoices, repair estimates, medical documents, or damage images. The goal is usually to support a false or inflated claim.

Can AI-generated claim documents be detected? Yes, but detection is strongest when teams look beyond appearance. File history, metadata, editing traces, mathematical errors, vendor inconsistencies, duplicate patterns, and payment details can all reveal problems that visual review may miss.

Why do fake insurance claims still leave a paper trail? Fraudulent claims must fit into real-world timelines, payment flows, supplier records, policy rules, and claim notes. Even when one document looks convincing, inconsistencies often appear when the full claim context is reviewed.

Should insurers rely only on AI tools to detect fraud? No. Automated detection is useful for triage and evidence review, but fraud decisions should involve human judgment, documented reasoning, and escalation procedures. The best approach combines technology with experienced claims and SIU teams.

What documents are most commonly manipulated in insurance claims? Common targets include repair invoices, receipts, damage photos, medical bills, contractor estimates, proof-of-purchase documents, towing invoices, rental bills, and warranty claim evidence.

Follow the Trail Before It Becomes a Payout

If your claims team is seeing cleaner receipts, sharper fake evidence, or more suspicious supplier patterns, the answer is not to stare harder at PDFs.

Docklands AI helps insurers detect manipulated, photoshopped, and AI-generated invoices and receipts using document forensics, tampering detection, metadata analysis, mathematical checks, and payment context. If you want to catch the paper trail before it becomes a loss, it is worth seeing what your current process is missing.

Request a Demo Today!

Book your demo below.