Predictive Analytics for Insurers Needs Evidence

Here is my mildly unpopular opinion after a decade around fraud operations: predictive analytics for insurers is often treated like a courtroom witness when it is really a very good smoke alarm.

A smoke alarm can tell you something needs attention. It cannot tell you who lit the match, what burned, or whether the toaster is simply being dramatic.

That distinction matters more in 2026 than it did even two years ago. Fraud teams are swimming in claim scores, anomaly alerts, behavioral signals, provider risk profiles, and network maps. Useful? Absolutely. Enough to support a tough claims decision? Not by itself.

I once sat in a review where a claim had a risk score high enough to make everyone in the room sit up straighter. A manager asked the question every fraud professional has heard: can we decline it? The answer was awkward but correct: not on the score alone. The model had suspicion. The file needed evidence.

That is the whole point. Predictive analytics for insurers needs evidence because suspicion helps you prioritize, while proof helps you act.

Prediction is a triage tool, not a verdict

Insurance fraud is too expensive to ignore and too sensitive to handle casually. The FBI notes that non-health insurance fraud costs more than $40 billion per year in the United States alone, adding hundreds of dollars to the average family’s annual premiums. That is not a rounding error. That is leakage with a steering wheel.

Predictive models are good at finding patterns humans miss. They can flag a home repair invoice that lands unusually fast after a storm, a medical bill with odd coding patterns, a warranty claim tied to a repeat repair shop, or a motor claim where the history smells a bit too rehearsed.

I like those tools. I have used them, defended them, cursed at them, and, on better days, thanked them.

But here is the catch: predictive models work mostly from data about the claim. They look at fields, histories, relationships, amounts, timings, geographies, and behaviors. If the submitted document itself is fake, edited, AI-generated, or physically manipulated before upload, the model may simply process a tidy version of a lie.

That is how bad evidence becomes clean data.

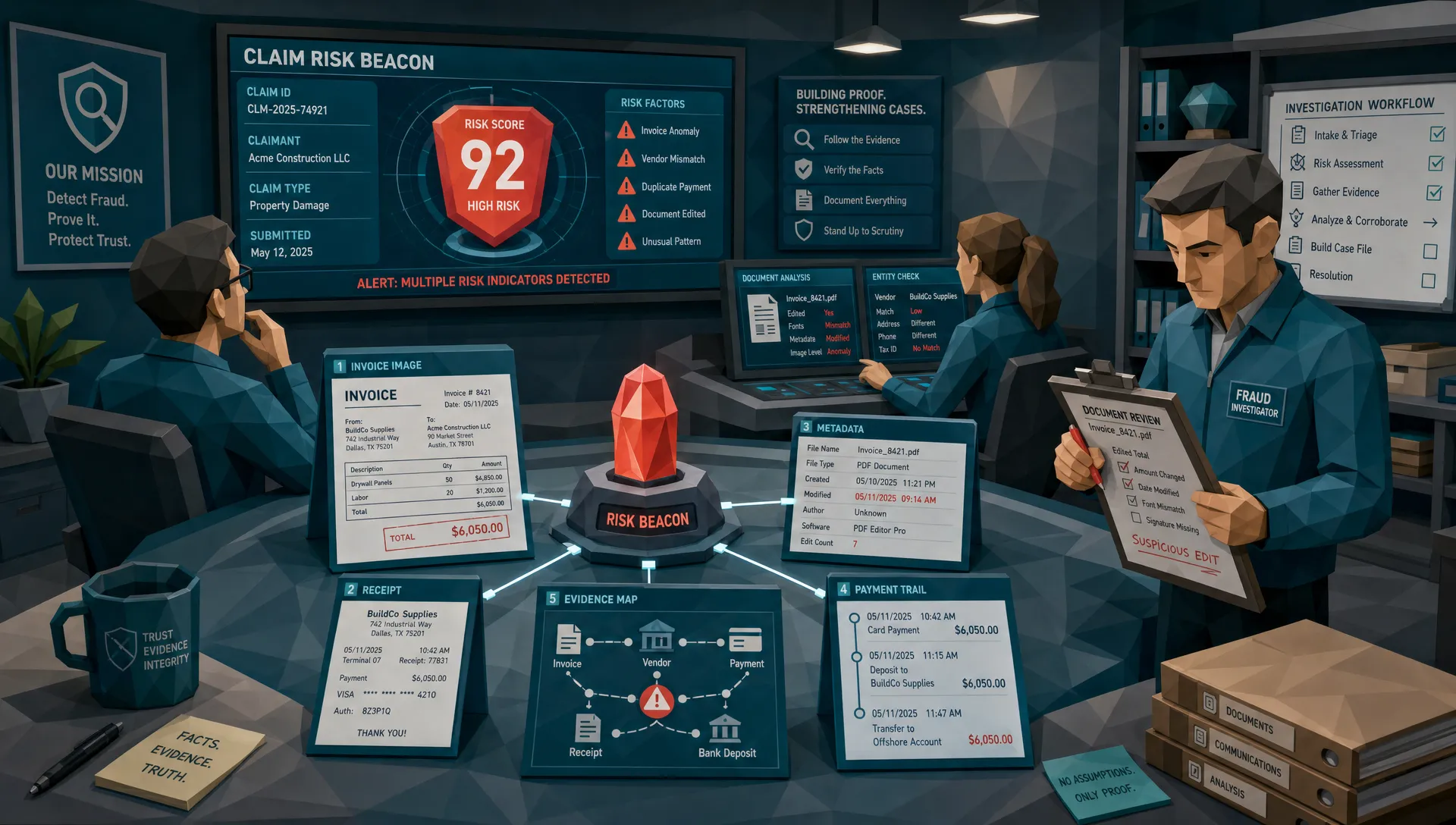

A model can tell you a repair shop is statistically unusual. It cannot, without document-level checks, tell you that the invoice total was pasted over the original amount, that the tax does not reconcile, that the metadata does not match the claimed timeline, or that the receipt image carries signs of digital editing.

This is why I am wary of any fraud program that celebrates high-risk scoring without asking a second question: what exactly can we prove?

The fraud has moved closer to the evidence

For years, many fraud schemes were lazy. A claimant reused an old receipt. A vendor inflated a line item. Someone submitted the same invoice twice with a new claim number. The fraud was not clever, it was just annoying.

Now, the tools are better. A claimant can edit a receipt on a phone during lunch. A fake invoice can look professional enough to pass a tired Friday afternoon review. AI-generated photos and documents make the old sniff test less reliable.

The trend is not imaginary. The BBC reported that Admiral saw a sharp rise in fraudulent claims linked to AI-generated fake images and deepfakes. Verisk’s 2025 Fraud Report also found that many carriers believe claims manipulation has become more sophisticated, and it highlights how consumer willingness to alter evidence with AI varies sharply by generation in its 2025 fraud analysis.

That last point makes some people uncomfortable, but it matches what I see in the field. The barrier to manipulation has dropped. You no longer need a dedicated fraud ring with a graphic designer in a back room. You need a phone, a motive, and ten quiet minutes.

So when we talk about predictive analytics for insurers, we have to admit something important: the model may be looking downstream from the manipulation. If the document has already been altered, the claim data extracted from it can be persuasive in exactly the wrong direction.

There is a practical lesson here. If your analytics stack scores the claim but never inspects the evidence, you have built a very clever queueing system. You have not built a reliable fraud decision process.

What evidence actually means in a claims file

Evidence does not mean a vague note saying suspicious vendor or possible exaggeration. I have seen files like that, and they age badly. Six months later, nobody remembers what suspicious meant, and the claimant’s complaint letter is written in very clear English.

Evidence means the file contains explainable findings that a claims manager, SIU investigator, or auditor can understand without squinting at a spreadsheet.

In invoice and receipt fraud, that usually means looking at the document from several angles:

- Image integrity, including signs of splicing, cloning, inconsistent compression, or edited regions.

- Metadata and file history, including timestamps, device traces, software clues, and inconsistencies with the claim timeline.

- Mathematical checks, including totals, taxes, discounts, quantities, and line items that do not reconcile.

- Physical manipulation clues, including printed-then-scanned edits, shadows, folds, alignment issues, or suspicious overlays.

- Payment context, including whether payment details match the claimant, vendor, prior files, or known risky patterns.

That last one matters more than people think. A document can look visually legitimate and still be suspicious when the payment trail does not fit. In claims, expense, and invoice fraud, the money movement often tells the story the document is trying to hide.

This is also where document forensics and predictive modeling should stop competing. They answer different questions. A risk model asks, should we look here? Evidence analysis asks, what is actually wrong with what we found?

Docklands AI focuses on that evidence layer for invoices and receipts: detecting AI-generated documents, Photoshop-style tampering, metadata anomalies, mathematical irregularities, physical manipulation, and payment-related signals. If you want the broader comparison, we have covered why insurance claim fraud detection models and document forensics both matter in more detail.

Proof is normal in other industries, so why not claims?

One thing fraud teams can borrow from engineering is a healthy disrespect for assumptions. If you have ever worked near hardware, you know nobody ships a circuit into production because a slide deck says it probably works. Teams such as ProMicro’s embedded systems and electronics design specialists prototype, test, inspect, and validate before a product gets anywhere near scale.

Claims operations should have the same discipline. A high fraud score should not be the end of the conversation. It should trigger validation.

I once reviewed a property claim involving a small kitchen repair. Nothing glamorous. The invoice looked normal at first glance, with the usual logo, labor line, materials line, and a grand total that felt plausible. The predictive score was moderately high because the vendor had appeared in several unrelated claims. That was enough to route it for review, but not enough to challenge it.

The evidence changed the conversation. The tax calculation was off by a few cents in a way that did not match the jurisdiction. One line item had slightly different compression artifacts than the rest of the invoice. The payment account had been used in a prior claim under a different vendor name. None of those clues alone would make me slam a folder shut like a TV detective. Together, they justified a careful follow-up.

That is how this should work. Prediction got the claim onto the right desk. Evidence gave the adjuster something concrete to do next.

The false positive problem is really a trust problem

Fraud teams often talk about false positives as an efficiency issue. That is true, but incomplete. False positives also damage trust.

If adjusters get too many weak alerts, they stop believing the system. If SIU receives too many files with no evidence, investigators waste time rebuilding the case from scratch. If customers are challenged based on vague risk signals, the carrier can create friction, complaints, and reputational pain.

This is where evidence earns its budget.

A predictive score might say a claim is in the top 2 percent of risk. Useful. But when the file also shows an invoice with inconsistent metadata, a suspicious payment destination, and a manipulated total field, the conversation becomes much cleaner.

The adjuster is no longer saying the computer did not like your claim. They can say we need clarification because the document appears inconsistent with the stated timeline and payment details. That is a very different posture.

For SIU leaders, this matters because good evidence improves prioritization. The best investigators should not be spending half a day chasing every odd-looking claim score. They should be working files where the risk signal has been strengthened by document proof.

For claims leaders, it matters because evidence helps separate fraud from messiness. Plenty of legitimate claims look weird. People lose receipts, vendors make mistakes, PDFs get compressed, and small businesses use ugly templates. A good evidence process should help avoid treating every messy file like a criminal conspiracy.

That is also why I am skeptical of fraud dashboards that only show risk volumes, hit rates, and model confidence. Show me evidence confirmation rates. Show me how often document findings changed the claim action. Show me how many high-risk claims were cleared because the evidence held up. That is the adult version of fraud measurement.

A better workflow: score first, prove before action

The workflow I prefer is simple in principle, even if the plumbing takes some work.

At intake, predictive analytics scores the claim, invoice, receipt, provider, claimant, vendor, or repairer. That score decides urgency and routing. Low-risk claims can keep moving. Higher-risk claims get more scrutiny.

Then the evidence layer runs on the submitted documents. For invoices and receipts, that means forensic checks on images, files, metadata, calculations, layout, payment information, and historical reuse. The goal is not to make every claim slower. The goal is to apply deeper review where it has the highest payoff.

Finally, the results should land in language a claims handler can use. Not mysterious machine confidence. Not a dozen unexplained flags. A practical finding might say the invoice total area shows signs of local editing, the embedded metadata indicates the file was modified after the stated service date, and the payment account appears across multiple unrelated vendor names.

That is a claim note. That is a referral reason. That is something SIU can test, challenge, and document.

If you are building or refining this process, one useful exercise is to pull twenty recent fraud referrals and ask a blunt question: did the model help us find the file, or did it help us prove the issue? If the answer is mostly the first, your next investment probably belongs in evidence.

We have also written about why predictive claim models miss edited evidence, because this gap shows up constantly when insurers rely too heavily on structured data.

The best models get better when evidence feeds them

There is a nice upside here. Evidence does not only help current claims. It improves future analytics.

A confirmed manipulated invoice is a better training signal than a vague suspicious outcome. A cleared high-risk claim is equally valuable because it teaches the organization what legitimate oddness looks like. Over time, the fraud program becomes less noisy because the feedback loop is grounded in what was actually found, not merely what was suspected.

This is where predictive analytics for insurers becomes much more useful. The model still finds patterns at scale, but document evidence sharpens the labels behind those patterns. Instead of fraud confirmed, maybe, sort of, if you read the notes, the organization can distinguish between edited receipt, fabricated invoice, payment mismatch, duplicate document, vendor anomaly, and clean file.

That level of detail helps claims managers, SIU, compliance, and finance speak the same language. It also helps executives understand the difference between activity and impact. More alerts are not always better. Better-supported alerts are.

What to ask your analytics team tomorrow

If I were a claims or fraud manager reviewing my current setup, I would ask three uncomfortable questions.

First, when a high-risk score is generated, what evidence is automatically gathered from the documents? If the answer is mostly OCR fields and rules, you may be missing the manipulation layer.

Second, can the finding be explained to a claimant, regulator, auditor, or legal team without hiding behind model language? If not, the alert may be operationally interesting but weak in a dispute.

Third, are payment details being considered alongside the document itself? A forged invoice is rarely created for artistic satisfaction. Someone wants to get paid. Follow the money, because it has poor manners and often leaves footprints.

These questions are not anti-analytics. They are pro-results. Predictive models are valuable, but they become much more useful when paired with evidence that can survive a real-world claims conversation.

Frequently Asked Questions

What is predictive analytics for insurers? Predictive analytics for insurers uses historical and current claim data to estimate risk, prioritize files, and identify patterns that may indicate fraud, leakage, or operational issues.

Why is a fraud score not enough to prove a suspicious claim? A fraud score shows probability, not proof. Claims teams still need document evidence, payment context, investigation notes, and policy analysis before taking serious action.

What kind of evidence should insurers look for in invoices and receipts? Insurers should look for digital tampering, AI-generated document clues, metadata inconsistencies, mathematical errors, physical manipulation, duplicate reuse, and payment details that do not fit the claim.

Does document forensics replace predictive analytics? No. Predictive analytics helps decide where to look first. Document forensics helps explain what is wrong, or confirm that the file is probably clean.

Can evidence-based review reduce false positives? Yes. When document findings are used alongside risk scores, teams can focus on files with stronger support and clear suspicious claims that look unusual but have legitimate evidence.

Make the score earn its keep

My hot take is simple: if a predictive model cannot lead you to evidence, it is only half a fraud control.

The future of claims fraud detection is not a bigger pile of alerts. It is a tighter connection between risk signals and provable document findings. That is how insurers move faster without getting reckless, challenge suspicious claims without guessing, and protect honest customers from paying for dishonest ones.

If your team is reviewing invoices, receipts, claims evidence, or payment details and wants a stronger evidence layer behind fraud decisions, Docklands AI can help detect manipulated, photoshopped, and AI-generated documents before they turn into paid losses.

Request a Demo Today!

Book your demo below.