Accident Claim Scams Often Start With One Repair Bill

Here’s my slightly unpopular take: most accident claim scams do not begin with a dramatic lie about the crash. They begin with a very boring PDF.

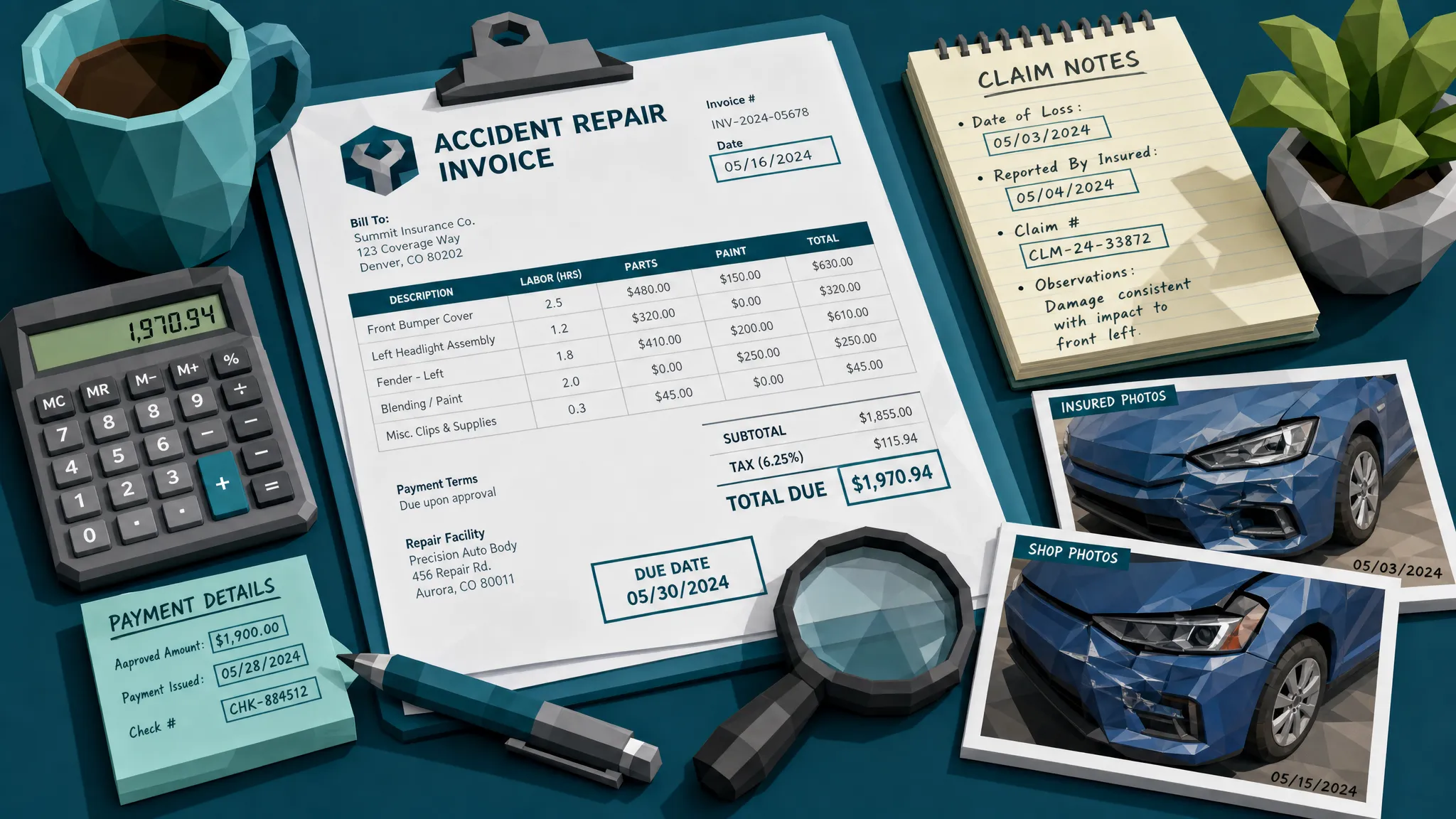

A repair bill lands in the claim file. It looks normal enough. There is a shop name, a total, a few line items, maybe a logo that appears to have survived three generations of photocopying. Nobody gasps. Nobody calls the special investigations unit right away. The claim moves forward because the bill feels like paperwork, and paperwork has a way of making fiction look official.

After a decade around fraud reviews, I have learned to respect the humble repair bill. It can be the first clean-looking object in a messy scheme. It can also be the first place the scheme falls apart.

The FBI estimates insurance fraud costs the United States more than $300 billion each year, and staged or exaggerated accident claims are a familiar part of that landscape. But the cases I worry about most are not always the Hollywood versions with fake witnesses and choreographed collisions. They are the claims where the loss may be real, but the repair bill quietly grows a second head.

Why one repair bill matters more than it should

A repair bill does a lot of work in an accident claim. It translates damage into dollars. It supports liability decisions. It gives the adjuster something concrete to approve, negotiate, or challenge. It also creates a tidy bridge between the story of the accident and the payment being requested.

That is exactly why fraudsters like it.

A manipulated repair bill can do several things at once. It can inflate labor hours, add parts that were never replaced, change dates to fit the claim timeline, or make an unrelated repair look accident-related. Sometimes the bill is not fake from top to bottom. It is worse than that, because it is partly real.

Partial truth is the fraudster’s favorite seasoning. A genuine shop name, a legitimate tax ID, or a real diagnostic fee can make an altered total feel believable. I once reviewed a claim where the initial invoice looked routine, until the payment details showed a different business name than the repair shop listed on the bill. The explanation was “they use another company for billing.” Maybe. But the alleged billing company had been incorporated three weeks earlier and shared an address with the claimant’s cousin. Fraud is often less clever than it thinks it is.

The lesson is not that every odd repair bill is fraudulent. The lesson is that the bill should never be treated as a standalone truth machine.

The repair bill is where the story becomes expensive

In accident claims, the story may start with impact, injury, damage, or disruption. But the repair bill is where that story asks for money.

That shift matters. Before the bill arrives, the claim can still be vague. Once an invoice appears, the claim becomes measurable. That is when exaggeration becomes easier to hide behind numbers.

A claimant may not feel comfortable inventing an entire accident. But adding a few extra repairs to an invoice, changing a date, or reusing a bill from a previous incident can feel less risky to them. I am not defending the logic, I am just telling you what I have seen. People who would never rob a bank will sometimes “round up” a claim until it looks like a small home renovation project.

The danger for insurers is that many review processes still treat repair bills as administrative evidence. If the document passes a quick visual check and the amount is within authority, it may slide through. That is how accident claim scams scale. Not through genius, but through workflow fatigue.

This is why I often tell adjusters to look at the document, then look around the document. The surrounding context is usually where the bill starts sweating.

The red flags I take seriously

I am cautious about calling anything a definitive fraud signal in isolation. Real businesses have ugly invoices. Real repair shops make typos. Real claimants lose paperwork, pay in strange ways, and upload photos that look like they were taken during an earthquake.

Still, some patterns deserve attention. A repair bill should raise eyebrows when the details seem too conveniently aligned with the claim narrative, or strangely disconnected from everything else in the file.

The most useful red flags are not cosmetic. A blurry logo is not enough. A slightly odd font is not enough. What matters is whether the invoice behaves like a real business record.

Watch for inconsistent dates. If the accident allegedly happened on Tuesday, but the repair estimate was created the previous Friday, you have a problem. If the invoice date, payment date, rental period, and inspection date cannot coexist in the same universe, you have a better problem, because now you have something concrete to investigate.

Watch for totals that change without explanation. A repair estimate for $1,840 that becomes a final invoice for $4,950 is not automatically fraud, especially with hidden damage. But the jump should be supported by supplements, photos, parts records, or authorization notes. If the increase is only visible in the final PDF, I start making coffee.

Watch for line items that do not match the damage. A low-speed rear-end collision does not usually require unrelated front-end work. A cracked bumper does not explain new tires, deep interior cleaning, or “miscellaneous structural adjustment” with no labor detail. Vague line items are where nonsense goes to wear a tie.

Watch for payment oddities. If the repair bill names one shop, but the payment request points to a personal account or unrelated entity, slow down. Docklands spends a lot of time on this point because payment information can build a deeper fraud picture than a simple “does this image look real?” check. The invoice is one layer. The money trail is another.

If you want a broader view of document tampering across claim types, the Docklands piece on how fraud in claims often starts with document manipulation is a useful companion read.

Why manual review misses the obvious stuff

Manual review is not bad. In fact, experienced adjusters are often excellent at spotting narrative problems. The issue is volume. A claim handler might review dozens of files in a day, each with photos, estimates, invoices, emails, notes, and payment details. That is not a fraud investigation. That is a paperwork obstacle course.

I have sat with claim teams during busy periods and watched the pressure build. Nobody says, “Please ignore fraud.” The pressure is more subtle. Close the claim. Hit the service target. Do not annoy a legitimate customer. Avoid needless escalation. Move the file.

Fraudsters understand that environment, even if they would not describe it that way. They know a plausible repair bill can act like a green light.

In 2025, the problem got sharper. The BBC reported that Admiral saw a 71% rise in fraudulent claims, with fake images and digitally generated evidence playing a role. Verisk’s 2025 fraud research also pointed to changing attitudes around claim evidence, including younger consumers being more open to altering evidence with digital tools. The takeaway for me is simple: if evidence is easier to create and manipulate, document review has to become more skeptical without becoming slower.

That last bit is the trick. Fraud controls that delay every honest claimant are not controls, they are customer experience traps.

The best fraud clue is often a mismatch, not a smoking gun

People expect fraudulent repair bills to look fake. Sometimes they do. More often, they look boring until you compare them with the rest of the file.

A bill that looks fine on its own may conflict with the estimate. The estimate may conflict with the photos. The photos may conflict with the accident description. The payment recipient may conflict with the vendor name. The tax calculation may conflict with the shop location. The metadata may conflict with the alleged document creation date.

That is why I like mismatch hunting. It is less glamorous than catching a forged logo, but it works.

One of my favorite small examples involved a repair invoice that listed a replacement part number. The part was real, the price was plausible, and the shop looked legitimate. But the part did not fit the vehicle model in the claim. Nobody had invented a fake shop. Nobody had used neon-green Photoshop artifacts. They had simply copied a line item from another invoice and hoped nobody would care.

This is also where process discipline matters. In any operation where errors are costly, good teams create repeatable checks instead of relying on heroic inspection. You see the same principle outside insurance. Food production lines, for example, depend on controlled processes and contamination checks, which is why companies such as Innovative Water Concepts build sustainable cleaning and contamination-control solutions for environments where small misses can become expensive quickly. Claims are different, of course, but the mindset is familiar: do not trust a single clean-looking output if the underlying process leaves gaps.

For repair bills, the “process” is the full trail: who created the estimate, when the repair was authorized, what changed, who got paid, and whether the document’s technical signals agree with the story.

The accident may be real, but the bill can still be fraudulent

This point matters because fraud discussions often get too binary. Real accident equals valid claim. Fake accident equals fraud. Life, sadly, is more annoying.

A driver can be involved in a genuine accident and still inflate the repair cost. A contractor can perform real work and still bill for additional labor. A claimant can submit a legitimate invoice, then alter the total before uploading it. A shop can be real but complicit. A third party can intercept or replace payment instructions.

If your fraud model only asks, “Did the accident happen?” you will miss plenty of leakage.

I have seen cases where the physical damage was not the issue at all. The vehicle was damaged. The repair happened. The fraud was in the supplement, the duplicate submission, or the payment routing. That is why accident claim scams often start with one repair bill, not because the crash is imaginary, but because the bill is the easiest place to turn a covered loss into a payday.

The same logic applies beyond auto. In property and casualty claims, one contractor invoice can quietly bundle pre-existing damage into a storm loss. In warranty claims, one service bill can convert routine wear into a covered failure. In travel or health-adjacent accident claims, one receipt can shift timing or inflate reimbursement. Different category, same old paperwork mischief.

What I would change in the review process

If I could redesign accident claim review from scratch, I would stop treating repair bills as attachments and start treating them as evidence packages.

That means the bill should be checked against the claim timeline, the repair estimate, photos, vendor history, payment instructions, prior claims, and document integrity signals. Not every claim needs a deep investigation. But every repair bill requesting payment should pass a basic coherence test.

The review should answer a few plain-English questions. Does this bill make sense for this accident? Does the timing make sense? Do the line items match the claimed damage? Has this document been edited in suspicious ways? Does the payment destination fit the vendor? Has this claimant, vendor, or account appeared in similar patterns before?

This is where technology helps, provided it is used practically. I am not interested in tools that merely say “suspicious” and then leave an adjuster to guess why. Good fraud detection should surface the specific reasons a document deserves attention, such as metadata inconsistencies, visible tampering, mathematical irregularities, duplicated evidence, or payment mismatches.

Docklands AI is built for that kind of work: detecting manipulated, photoshopped, and AI-generated invoices or receipts, while also using payment information to build a fuller fraud picture. For teams trying to catch issues before payout, that matters more than another dashboard that looks pretty in a quarterly meeting.

For a wider set of pre-payment warning signs, I would also point claims teams to this guide on claims fraud signals that appear before payout. The best time to find a bad repair bill is before finance has already released the funds and everyone is pretending recovery will be easy.

How fraud teams can review repair bills without slowing every claim

The practical objection is fair: claim teams cannot manually investigate every bill like it is a crime scene. They should not have to.

The answer is tiered scrutiny. Low-risk claims can move quickly when the repair bill, payment details, vendor history, and claim context all line up. Higher-risk claims should receive more attention because the file itself asks for it.

In my experience, the best teams do three things consistently. They standardize what “normal” looks like for common repair scenarios. They compare documents against context instead of reviewing them in isolation. And they give adjusters a clear escalation path that does not make them feel like they are throwing a grenade into the workflow.

That last part is underrated. If reporting a suspicious bill creates friction, people stop reporting. If fraud review sends every claim into a black hole, adjusters learn to avoid it. The process has to be fast, explainable, and proportionate.

This is also where known patterns help. Accident scams are often repetitive. The same inflated towing charges. The same suspicious vendors. The same altered dates. The same invoice template reused with just enough changes to pass a quick glance. If you are seeing those patterns in auto files, Docklands has a related breakdown on how fraudulent auto insurance claims follow familiar patterns.

A repair bill is not proof, it is a claim about a claim

Here is the hot take I promised: we give repair bills too much emotional authority.

Because they look official, we treat them as proof. But a repair bill is really an assertion. It says work was done, parts were used, amounts are owed, and the timing is true. All of that may be correct. Some of it may be correct. Or the bill may be wearing a fake mustache.

Fraud teams do not need to become cynical about every claimant. Most people are honest, and most claims deserve to be handled quickly. But speed and skepticism can coexist if the review process is designed well.

The goal is not to accuse. The goal is to verify before money leaves the building.

If one repair bill can start an accident claim scam, one smart review step can stop it.

Frequently Asked Questions

What are common signs of accident claim scams in repair bills? Common signs include dates that do not match the accident timeline, unexplained increases from estimate to invoice, vague line items, repairs unrelated to the reported damage, suspicious edits, and payment details that do not match the named repair vendor.

Can a real repair shop invoice still be part of a fraudulent claim? Yes. A repair shop can be legitimate while the submitted bill is altered, inflated, duplicated, or used for damage unrelated to the accident. The key is to compare the invoice with the broader claim file and payment trail.

Should every accident repair bill be escalated to fraud review? No. Most claims should move efficiently. The better approach is risk-based review, where documents with timing conflicts, tampering signals, unusual payment instructions, or vendor anomalies receive deeper scrutiny.

Why do payment details matter in accident claim fraud? Payment details can reveal mismatches that the invoice image does not show. If the bill names one business but payment is requested to a different entity or personal account, that discrepancy deserves review before payout.

Catch the repair bill before it becomes a loss

Accident claim scams often succeed because one repair bill looks ordinary enough to pass through a busy workflow. Docklands AI helps claims and fraud teams examine invoices and receipts for tampering, manipulation, AI-generated evidence, metadata issues, mathematical irregularities, and payment inconsistencies before payout.

If your team is still relying on visual review alone, it may be time to give the repair bill a harder interview. Visit Docklands AI to see how document fraud detection can fit into your claims process.

Request a Demo Today!

Book your demo below.