How a Deep-Fake Receipt Falls Apart Under Review

Here is my hot take after ten years of looking at suspicious claims, invoices, and expense packets: the best fake receipt is rarely beaten by a better pair of eyes. It is beaten by context.

A deep-fake receipt can look painfully convincing at first glance. The totals line up visually. The logo looks right. The paper has a coffee stain in just the right place. The claimant or employee may even submit it as a casual phone photo, which makes everyone feel like it must be real. Fraudsters know that reviewers are busy, queues are long, and nobody wants to be the person who delays a $42 lunch reimbursement for three days.

But receipts are stubborn little documents. They do not live alone. A real receipt has a relationship with a payment, a merchant, a timestamp, a tax rate, a device, a claim event, and sometimes a physical object. A fake has to keep all of those relationships straight. Most do not.

I once reviewed a repair receipt that looked clean enough to frame. The problem was not the logo, font, or image quality. The problem was that the receipt said the customer paid at 8:14 p.m., while the store location closed at 6:00 p.m. on Sundays. That is the kind of boring detail that ruins an otherwise beautiful lie.

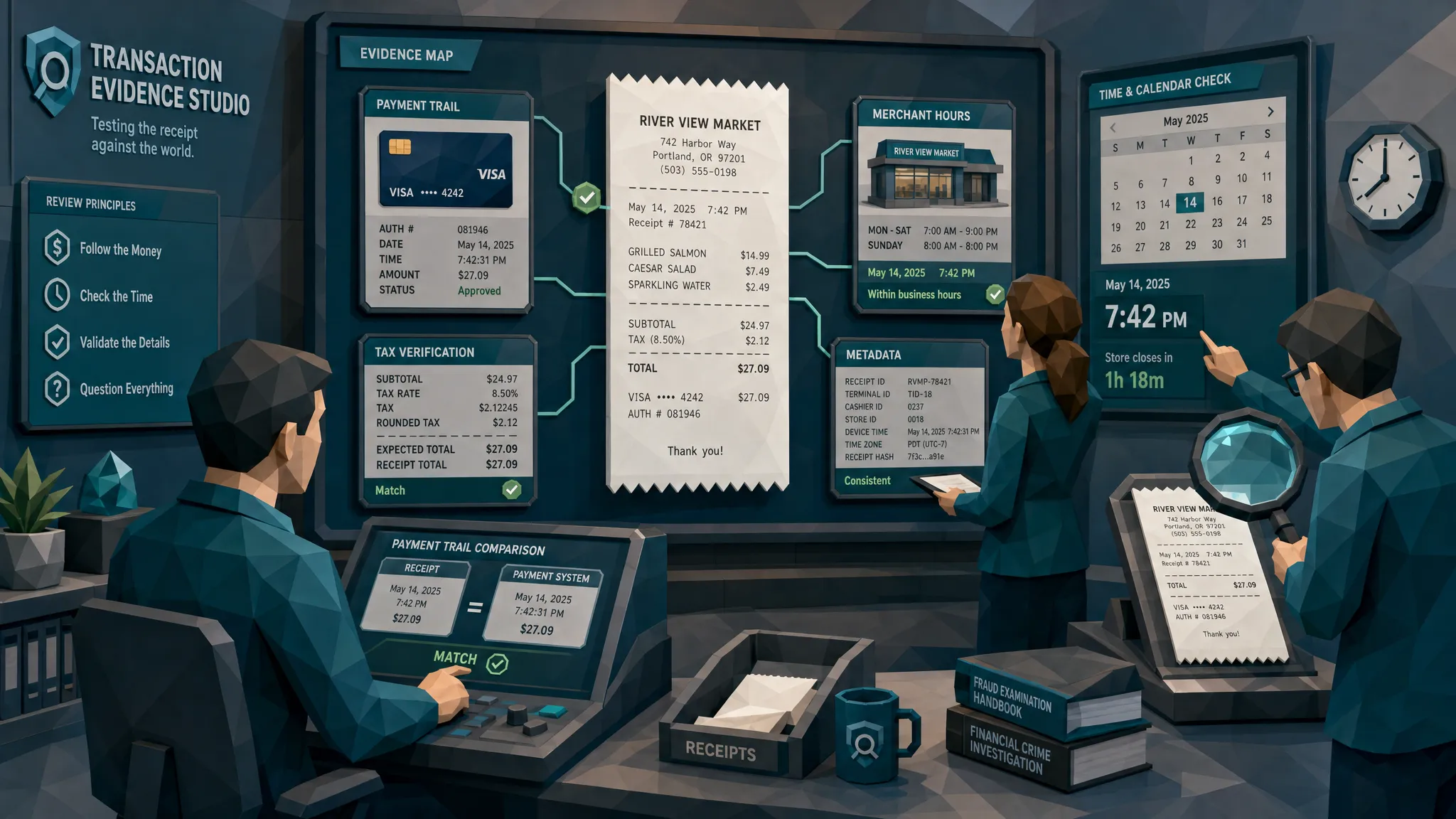

A deep-fake receipt has to survive five different tests

When people hear “deep-fake receipt,” they often imagine a fake document that fails because of weird pixels or a hallucinated store address. That does happen, especially with fast generated evidence. But the more interesting failures happen when the receipt is compared to the world around it.

In a proper review, the receipt has to pass five tests: the transaction story, the math, the image physics, the metadata, and the payment evidence. If any one of those is off, the document deserves a closer look. If two or more are off, I start clearing my afternoon.

This matters because the volume and quality of manipulated evidence are rising. The BBC reported that Admiral saw a 71% rise in fraudulent claims in 2025, with AI-generated fake images and deepfakes playing a role. On the insurance side, the FBI notes that non-health insurance fraud alone costs more than $40 billion per year, adding hundreds of dollars in premiums for the average family.

AP and expense teams are dealing with their own version of the same headache. The Association for Financial Professionals has reported widespread payment fraud targeting organizations, and the ACFE Report to the Nations continues to show how costly occupational fraud can become when controls lag behind behavior.

So yes, the receipt may look good. That is no longer the bar.

The first failure: the transaction story has gaps

A real receipt tells a story, even if it is a dull one. Someone bought something, from a specific merchant, at a specific location, on a specific date, using a specific payment method. That story should make sense next to the claim, expense policy, invoice, card feed, repair timeline, and vendor history.

Fraudsters often focus on the visible receipt and forget the story. In insurance claims, I have seen receipts dated after a loss but listing item models that were discontinued years earlier. In employee expenses, we see restaurant receipts submitted for a client dinner, but the transaction timestamp falls during a flight. In AP, a supplier invoice might reference a purchase location, project, or entity that does not match how that vendor normally bills.

The story can also be too perfect. I get twitchy when every suspicious receipt is cropped tightly, photographed at the same angle, and submitted minutes before a deadline. Normal people are messy in different ways. Fraudsters are often messy in the same way over and over.

A useful review question is simple: if this receipt is real, what else should exist? A card transaction, a delivery note, a repair photo, a purchase order, a calendar event, a mileage log, a warranty registration, a serial number, or a vendor communication may be expected. If the surrounding evidence is missing or oddly vague, the receipt has already started wobbling.

This is why relying only on “does it look real?” is a losing game. We have written before about why pretty fakes still fail review, and the short version is this: appearance is only one witness, and it is often the least reliable one.

The second failure: math is less forgiving than the human eye

Math has no sympathy. It does not care that the receipt has nice shadows.

Deep-fake receipts commonly stumble on subtotals, tax, discounts, tips, refunds, and change due. Sometimes the error is obvious, like a subtotal that does not equal the line items. More often, the problem is subtle. A tax amount is rounded in a way the merchant’s point-of-sale system would not use. A service charge appears before tax when the real merchant applies it after tax. A receipt shows cash tendered and card paid in a combination that would be unusual for that business.

Tax is my favorite quiet alarm bell. A fraudster may know the state tax rate, but miss the local add-on. They may apply tax to a non-taxable item. They may use a tax rate from the wrong city because they copied a template from somewhere else. None of these errors require a cinematic fraud lab to catch. They require reviewers to stop treating the total as decorative.

In AP, mathematical irregularities show up differently. A fake invoice might have neat round amounts across multiple line items, odd unit pricing, mismatched freight charges, or a total that has been altered while the amount in words remains unchanged. For expense teams, tips are a gold mine. A meal receipt with a handwritten tip that perfectly lands on a policy limit deserves attention, especially if it happens every Friday.

There is a phrase I use with new reviewers: fraud likes convenience. Real receipts are produced by systems with rigid rules. Fake receipts are produced by people trying to reach a goal.

The third failure: pixels and paper disagree

This is the part everyone expects, and it still matters. A deep-fake receipt often contains image-level clues that are hard to keep consistent across the whole document. The amount may have slightly different blur than the surrounding text. The merchant logo may be sharper than the thermal print. The paper grain may continue behind one line but not another. Shadows may fall naturally on the receipt edge, while the edited total floats above the paper like it has never met gravity.

Photoshop edits tend to leave seams. Generated receipts tend to leave odd textures. Printed fakes tend to reveal themselves through paper behavior, ink patterns, or repeated artifacts. If you have ever seen a “receipt photo” where the barcode looks crisp but the item names look melted, you know the feeling. It is the visual equivalent of someone wearing a tuxedo with flip-flops.

One common mistake is reviewing only the changed field. If the total looks suspicious, reviewers zoom into the total. Fair enough, but the better move is to compare that area with stable parts of the document. Are the characters formed the same way? Is the noise pattern consistent? Does the compression look uniform? Does the line spacing behave like the rest of the receipt?

For a deeper look at the physical side of this problem, our guide on why a printed fake receipt still gives itself away covers the paper and print clues that often survive even after someone tries to “launder” a digital fake by printing and re-photographing it.

The fourth failure: metadata forgets to lie consistently

Metadata is not a magic truth machine. Phones strip it. Apps rewrite it. Some systems convert images to PDFs and wipe useful clues. I have seen honest documents with strange metadata, and I have seen fake documents with clean metadata.

Still, metadata can be very useful when treated as one piece of the puzzle. A receipt photo created after the claim submission date is a problem. A PDF that claims to be a scanned receipt but was created in editing software deserves scrutiny. A file with multiple save events, mismatched timestamps, or an unusual device trail can help explain how the document moved before it arrived in your system.

The key is restraint. Do not accuse someone because one metadata field looks strange. Do use metadata to decide whether the receipt should be compared more closely against payment data, vendor records, and image-level evidence.

I learned this lesson the awkward way early in my career. I flagged a receipt because the metadata suggested it had been modified. It turned out the employee had used a company-approved scanning app that compressed every receipt the same way. The document was fine. My ego was not. Since then, I treat metadata like a witness who may be useful but should not be left alone with the verdict.

The final failure: payment evidence refuses to cooperate

This is where many deep-fake receipts collapse.

A receipt may say Visa ending in 4821. The card feed may show no matching transaction. The receipt may show a merchant name that does not match the acquirer descriptor. The amount may be close but not exact. The receipt may show a purchase on Saturday, while the payment settled from a different merchant category two days earlier. In insurance, a claimant may submit a repair receipt, but the payment record points to a different business entirely.

Payment context is powerful because it is harder to fake convincingly at scale. A fraudster can generate a receipt in minutes. They usually cannot generate the corresponding card transaction, merchant descriptor, authorization trail, refund history, and banking context with the same ease.

This is also why generic “is this image real?” checks are not enough for serious fraud review. They can help, but they are looking at a narrow slice of the evidence. The stronger approach is to ask whether the document and the payment story agree.

Docklands AI was built around that idea. For invoices and receipts, we combine forensic checks for manipulated, photoshopped, and AI-generated documents with payment information to build a deeper fraud picture. In practice, that means a suspicious document is not judged only by pixels. It is judged by whether the document behaves like a real transaction.

How I would review a deep-fake receipt tomorrow morning

If I were sitting with a claims manager, AP manager, or expense lead tomorrow, I would not tell them to turn every reviewer into a forensic examiner. That is a lovely idea if you have unlimited budget and a time machine. Most teams have neither.

I would start by separating routine review from high-risk review. A low-dollar, policy-compliant receipt from a known employee or vendor should not receive the same attention as a high-dollar claim with a new vendor, a rushed submission, and a fuzzy receipt uploaded at 11:58 p.m.

For high-risk items, I like a simple review pattern:

- Does the receipt match the event, policy, vendor, and expected timeline?

- Do the subtotal, tax, discounts, tips, and totals behave correctly?

- Does the image show inconsistent blur, compression, shadows, spacing, or typography?

- Does the metadata support the claimed origin, or does it raise a reasonable question?

- Does the payment trail match the amount, merchant, date, and method shown on the receipt?

That is not a long checklist. It is a discipline. The point is to stop treating the receipt as a standalone object and start treating it as part of a transaction.

There is also a human side. Reviewers need permission to question attractive documents. Many frauds get through because the receipt “looks professional.” Well, so do forged resumes, fake invoices, and half the cold emails in your spam folder. Professional appearance is cheap now. Coherence is harder.

If your team sees the same patterns repeatedly, document them. Maybe fake receipts from one merchant often use the wrong tax treatment. Maybe a certain expense category has a habit of producing cropped images with no payment method visible. Maybe a contractor’s invoices always arrive as clean PDFs with no underlying purchase trail. Pattern memory is one of the best fraud controls a team can build.

What this means for claims, AP, and expense teams

The rise of deep-fake receipt evidence does not mean every receipt is suspicious. It means the old comfort signals have lost value. A crisp logo, a realistic fold, and a plausible total are no longer enough.

For insurance claims teams, the risk is paying for losses supported by fabricated purchase or repair evidence. For warranty teams, it is accepting proof of purchase that never existed. For AP teams, it is approving invoices that look routine but lack a real supplier transaction behind them. For expense teams, it is reimbursing employees for meals, rides, equipment, or lodging that were altered after the fact.

The best defense is not paranoia. Paranoia burns out good reviewers and annoys honest customers and employees. The better defense is layered review. Let humans handle judgment, context, and escalation. Let forensic tooling handle the tedious comparisons across image quality, metadata, math, and payment information.

If you want a practical companion piece, our article on what fake receipt generator output reveals instantly shows how fast-made fakes often expose themselves before the review even gets sophisticated.

My final opinion may be unpopular with anyone selling a simple “real or fake” button: receipt fraud is not solved by a single score. It is solved by evidence alignment. When the receipt, payment record, timing, merchant behavior, and document forensics all agree, you can move faster with more confidence. When they disagree, the deep-fake receipt starts to fall apart.

Frequently Asked Questions

What is a deep-fake receipt? A deep-fake receipt is a fabricated or heavily manipulated receipt made to look like proof of a real purchase. It may be generated, edited from a real receipt, printed and photographed, or altered with image editing tools.

Can a deep-fake receipt look completely real? Yes, at first glance. Many fakes now look convincing enough to pass a quick visual review. They usually fail when compared against math, metadata, payment records, merchant behavior, and the surrounding claim or expense context.

What is the strongest clue that a receipt is fake? Payment mismatch is one of the strongest clues. If the receipt amount, merchant, date, payment method, or card details do not match the payment evidence, the document should be escalated.

Should reviewers rely on metadata to reject a receipt? Not by itself. Metadata can be altered, stripped, or changed by normal scanning and upload tools. It is best used alongside image forensics, mathematical checks, and payment verification.

How can teams review receipts faster without missing fraud? Teams should triage by risk and use automation for repetitive checks, including tampering detection, metadata analysis, math validation, and payment matching. Human reviewers can then focus on judgment calls and escalations.

A better way to catch receipts that only look real

If your team is still reviewing receipts with zoom, instinct, and a prayer, I get it. That is how many fraud programs started. But deep-fake receipt evidence has made visual review too fragile on its own.

Docklands AI helps claims, AP, and expense teams detect manipulated, photoshopped, and AI-generated invoices and receipts before they become losses. We combine document forensics with payment context, so your reviewers can see where the story holds together and where it breaks.

Because in fraud review, the question is not whether a receipt looks real. The question is whether it can survive being compared to reality.

Request a Demo Today!

Book your demo below.