Invoice Detection Works Better With Payment Context

Invoice detection gets much sharper when it stops staring at the PDF like it owes it money.

That is my hot take, and I will happily defend it in any AP, claims, or expense review meeting. A document can look perfect and still point money to the wrong place. A receipt can be genuine and still be misused. An invoice can pass OCR, match a purchase order, and sail through approval while the real problem sits quietly in the payment instructions.

In my experience, the most dangerous fake invoices are not the messy ones with wonky logos and suspicious fonts. Those are almost charming. The expensive ones are boring. They look like every other supplier invoice in the inbox. They use the right template, the right tax rate, the right approver, and just enough truth to avoid looking interesting.

That is why invoice detection works better with payment context. The document tells us what someone wants us to believe. The payment context tells us where the money is actually going.

My hot take: the invoice is only half the crime

Fraud teams love documents because documents leave clues. I do too. A manipulated PDF can reveal odd compression patterns, pasted text, inconsistent lighting, broken metadata, strange math, or edits that do not belong. Those clues matter.

But an invoice is rarely the end goal. Nobody manipulates an invoice for the joy of creating admin paperwork, unless they have a very unusual hobby. The goal is payment.

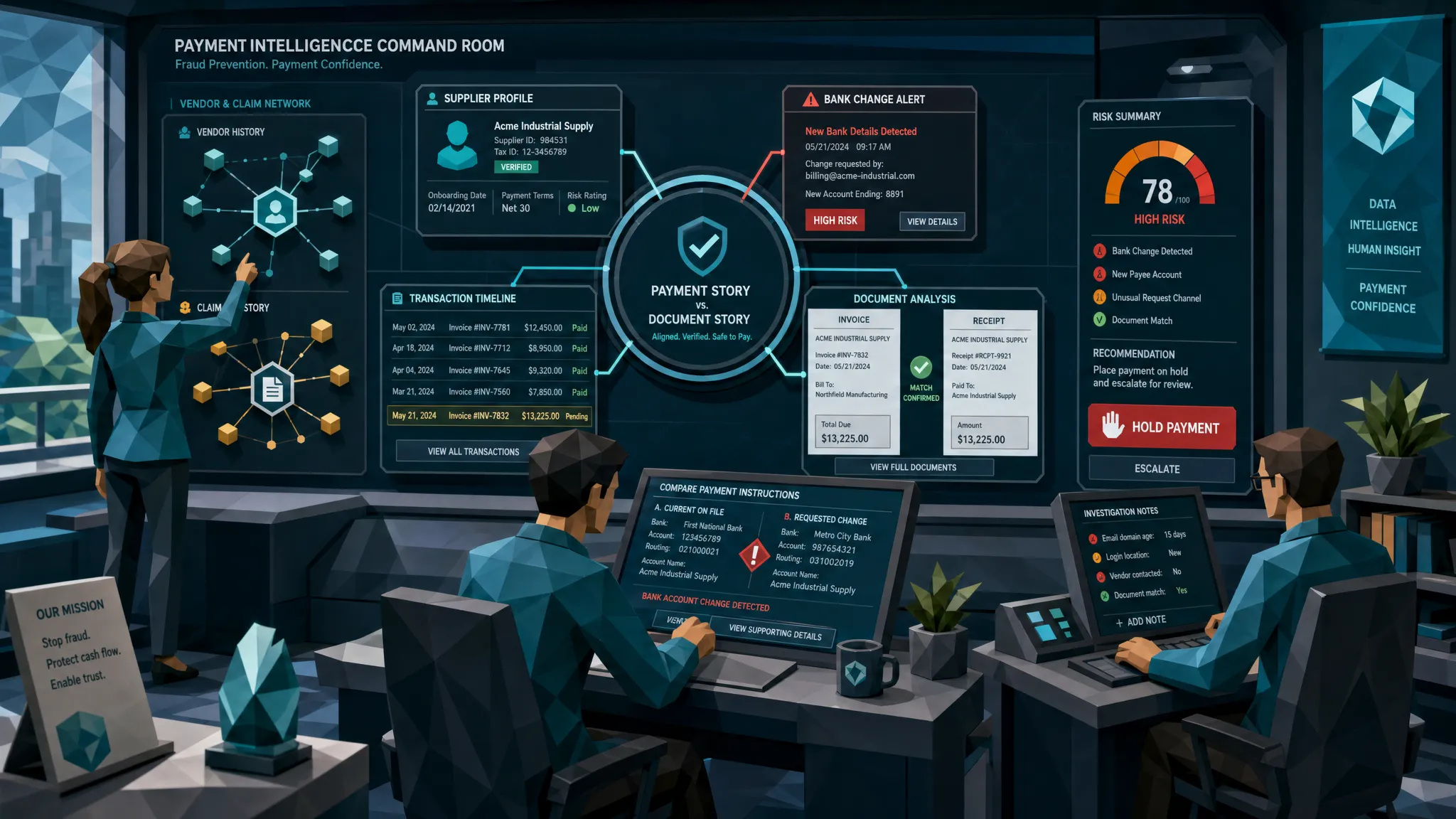

A few years ago, I reviewed a supplier invoice that looked painfully normal. Same vendor name, same layout, same line items, same approver. The invoice itself was clean enough that a busy AP clerk would have had no reason to pause. The catch was in the payment details. The bank account had changed, the payee name was slightly different from the supplier master, and the change request had arrived during a holiday week. Classic timing. Fraudsters do love a long weekend.

If we had only asked whether the invoice looked real, we would have shrugged and paid it. When we asked whether the payment made sense, the whole thing started to smell like microwaved fish in an office kitchen.

Why document-only checks miss good fraud

A lot of invoice systems were built to move work faster. Capture the fields, route the approval, match the PO, schedule the payment. That is useful, but speed is not the same as control.

OCR can read an invoice. Workflow software can push it to the right person. Matching logic can confirm that the amount lines up with a purchase order. None of that proves the document has not been manipulated, and it definitely does not prove the payment destination is safe. This is why I keep saying that invoice automation software needs more than OCR if the goal is fraud prevention rather than tidy processing.

The payment fraud backdrop is not exactly comforting. The Association for Financial Professionals has repeatedly reported high levels of payments fraud attempts against organizations. Business email compromise remains especially painful because it targets the human and procedural gaps around payments. The FBI Internet Crime Complaint Center reported billions in losses tied to business email compromise in its 2023 IC3 report.

Here is the uncomfortable bit: many of these attacks do not require a ridiculous fake invoice. They require a believable invoice attached to a believable process at a believable moment.

That is why document-only invoice detection can become a very polished magnifying glass. Helpful, yes. Complete, no.

What payment context actually means

Payment context is the surrounding financial reality of the invoice. It is the who, where, when, how, and whether-this-has-ever-happened-before of the payment request.

For an AP team, that might include the vendor master record, bank account history, recent changes to payment instructions, invoice frequency, currency, tax treatment, PO behavior, approver history, and whether the invoice looks similar to prior submissions.

For an insurance claims team, it might include claimant history, repair shop or contractor details, bank account ownership, claim timing, policy coverage, estimate patterns, prior payouts, and whether the invoice amount fits the physical facts of the claim.

For employee expenses, it might include merchant data, corporate card activity, employee role, travel dates, duplicate receipt submissions, reimbursement method, and whether the same receipt image has appeared before.

Put more simply: a document may answer, does this look like an invoice? Payment context asks, should we send money because of it?

That second question is where the fraud usually hides.

The payment clues I care about most

When we bring payment context into invoice detection, certain patterns become far easier to spot. The trick is not to create a monster checklist that nobody reads. The trick is to surface the few clues that change the risk picture.

Bank details that change at the wrong time are near the top of my list. A new bank account is not automatically fraud. Suppliers change banks, businesses get acquired, and finance teams update records all the time. But a bank change paired with urgency, a first-time approver, a high-value invoice, or a slightly altered supplier email deserves attention.

Payee names that do not match the relationship are another underrated clue. The invoice may say a known vendor, but the payment account might point to an individual, a related entity, or a name that is close enough to pass a sleepy Friday review. Close enough is not a control. It is a polite invitation to be robbed.

Amounts that fit the approval threshold too neatly should also get a look. If the approval limit is $10,000 and invoices keep arriving at $9,875, I do not assume the universe is being considerate. I assume someone understands the workflow.

Duplicates that are not exact duplicates are common too. Fraudsters and sloppy submitters both know that changing an invoice number, cropping a receipt, or adjusting a date can help avoid simple duplicate checks. This is why duplicate invoice detection should start before approval, before a payment request gains the dangerous social proof of having already been approved.

Payment behavior that does not match the vendor or claimant history can be the most revealing clue of all. A long-standing supplier suddenly invoices from a new location, requests a different currency, submits at a strange cadence, and changes bank details in the same week. Any one of those might be explainable. Together, they are a little orchestra of nope.

A simple example: the real receipt that still should not be reimbursed

Here is a non-expert example I use when explaining this to teams.

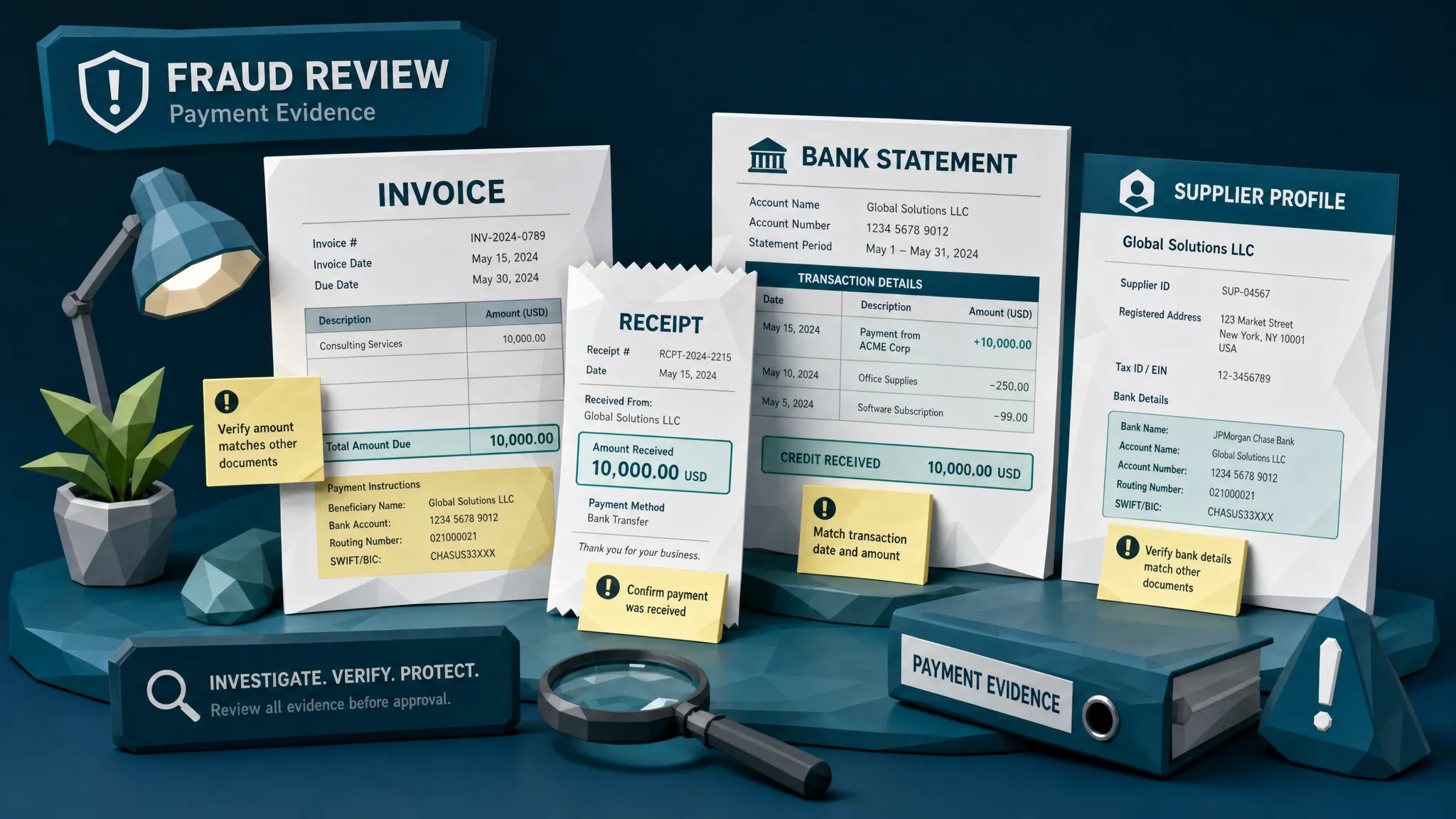

Imagine I submit a restaurant receipt for reimbursement. The receipt is real. The restaurant exists. The amount is accurate. The date is visible. A basic document check says, fine, that is a real receipt.

Now add payment context. My corporate card shows I was not at that restaurant. My calendar says I was on vacation. Another employee submitted the same receipt image two weeks ago. The receipt total is just under the threshold for manager review. Suddenly the question changes.

The receipt did not have to be fake to be fraudulent.

That point matters for employee expenses, warranty claims, health claims, property claims, and AP. Fraud is not always a forged artifact. Sometimes it is a real artifact placed into the wrong story.

The ACFE has long estimated that organizations lose around 5% of revenue to fraud each year, according to its Report to the Nations. That number includes many schemes, not just invoices or expenses, but it captures the larger lesson: weak context is expensive.

Insurance claims need the same thinking

Insurance teams have their own version of this headache. A contractor invoice after a home claim may look legitimate. A repair estimate may match the damage photos. A medical bill may contain all the expected fields. But the payment context can tell a different story.

Has this contractor appeared across unrelated claims with similar wording? Has the claimant used the same bank account as another claimant? Does the invoice date make sense given the loss date and inspection timeline? Does the amount resemble a normal repair cost for that geography, property type, or vehicle class? Was the invoice created after the adjuster requested additional evidence?

The FBI has warned for years that insurance fraud increases costs across the system. From where I sit, the new wrinkle is that fake evidence is getting easier to produce and harder to review manually at scale. Claims teams cannot rely on visual inspection alone, especially when repair invoices, medical documents, photos, and payment instructions all interact.

A manipulated invoice is one risk. A genuine invoice tied to a suspicious payout pattern is another. Both deserve attention before money moves.

Why payment context reduces false alarms

Fraud teams do not need more noise. I have never met an AP manager who woke up thinking, I hope my queue has 400 low-quality alerts today. If that person exists, please keep them away from my coffee.

Payment context helps because it gives alerts a reason. A tiny visual anomaly on a low-value invoice from a long-standing supplier with stable bank details may deserve a light-touch review. The same anomaly on a first-time vendor with new payment instructions and a rushed approval path deserves a very different reaction.

This is where many fraud programs go wrong. They treat every suspicious document clue as equally important. In the real world, risk lives in combinations.

A mismatched font may be harmless. A mismatched font plus a changed beneficiary plus a new approver plus an invoice just under the approval threshold is a proper problem.

Good invoice detection should not shout every time a pixel looks odd. It should help teams decide which oddities matter because of the payment that follows.

Build the control where the decision happens

The best time to catch invoice fraud is before approval, not during reconciliation and definitely not after the bank transfer. After payment, you are no longer doing prevention. You are doing archaeology with a worse budget.

To make payment-aware detection work, the control needs to sit close to the decision point. That means analyzing the original document and the payment fields together before the invoice, claim, or expense is approved.

In practice, I like to see systems compare the submitted document with vendor or claimant history, review bank and beneficiary details, check for document manipulation, flag mathematical oddities, and connect those signals into a single review picture. Not a giant mystery score with no explanation. A practical risk view that tells an analyst why something deserves attention.

There is a wider finance lesson here too. Context beats isolated data in almost every spend decision. Procurement teams learn this during renewals when a quote looks reasonable until usage, licenses, terms, and commercial history are reviewed together. That is why specialist Salesforce contract and SKU reviews can be valuable before renewal discussions. The same principle applies to invoices: the document alone rarely tells the full financial story.

Where Docklands AI fits

Docklands AI was built around a simple idea: invoice and receipt fraud detection should look at the document and the payment reality around it.

The platform helps detect manipulated, photoshopped, and AI-generated invoices and receipts using forensic document analysis, metadata review, mathematical checks, and physical manipulation signals. Crucially, Docklands also uses payment information from a claim, expense, or payment request to build a deeper fraud picture than a basic document authenticity check.

That matters because most fraud losses do not happen when a suspicious PDF enters the inbox. They happen when that PDF convinces someone to release funds.

For insurance claim managers, that means better review of invoices and receipts tied to payouts. For AP managers, it means stronger checks before supplier payments leave the business. For employee expense teams, it means catching suspicious receipts before reimbursement becomes recovery work.

If your current process only asks whether the invoice can be read, routed, and matched, you are leaving a lot of context on the floor. And fraudsters, being the tidy little opportunists they are, will pick it up.

Frequently Asked Questions

What is invoice detection with payment context? Invoice detection with payment context means reviewing the invoice document alongside payment details such as bank account, beneficiary name, vendor history, approval path, amount behavior, and prior transactions. It helps teams judge whether the payment request makes sense, not only whether the document looks real.

Why is document-only invoice detection risky? Document-only checks can miss fraud when the invoice appears legitimate but the payment destination, timing, or vendor behavior is suspicious. Many fraud attempts use mostly accurate documents with small but important changes to payment instructions.

Does payment context help reduce false positives? Yes. Payment context helps separate minor document oddities from meaningful fraud signals. A small visual anomaly may matter much more when it appears alongside a new bank account, unusual approval route, or first-time vendor payment.

Is this only relevant for accounts payable teams? No. Payment-aware detection is useful for insurance claims, warranty claims, health claims, employee expenses, and any workflow where documents are used to justify payment. The risk pattern is similar: a document creates trust, then money moves.

When should invoice detection happen? It should happen before approval and before payment. Once an invoice is approved, it gains credibility inside the workflow and becomes harder to stop. After payment, the organization is already in recovery mode.

Stop treating invoices like lonely PDFs

The invoice is evidence, but the payment is the motive. If we separate the two, we make fraud detection harder than it needs to be.

My advice is simple: keep the forensic document checks, but do not let them work alone. Pair them with payment context. Look at where the money is going, how the payment request compares with history, and whether the story holds together.

If you want to catch manipulated invoices, suspicious receipts, and risky claims before they cost real money, Docklands AI can help you bring document forensics and payment context into the same review process.

Request a Demo Today!

Book your demo below.