Invoice Reports That Actually Help Stop Fraud

Invoice reports should make a fraud reviewer slightly uncomfortable.

That is my hot take after a decade of looking at suspicious claims, vendor payments, and expense reimbursements. If a report only tells you that 1,248 invoices were processed, 97% were paid on time, and three departments are behind on approvals, congratulations, you have built a very tidy rearview mirror. It may help operations. It will not stop much fraud.

The invoice reports that actually help stop fraud do something different. They tell us which invoices deserve attention before money leaves the building, why they look strange, and what a human reviewer should do next. That sounds obvious, but in practice many finance and claims teams still rely on reports designed for throughput, not prevention.

And fraudsters know it. They do not need to beat your whole organization. They only need to beat the part of the process that says, looks fine, pay it.

My hot take: most invoice reports are built for comfort, not prevention

I once reviewed a set of contractor invoices for a property claim where every line item looked sensible at first glance. Paint, drywall, labor, disposal, all the usual suspects. The invoice total matched the estimate closely enough that nobody felt the need to poke it. The problem was buried in the document itself. A few digits in the bank details had been swapped, and the file had been resaved in a way that did not match the vendor’s normal pattern.

The monthly report would have shown the invoice as approved, paid, and closed. Very efficient. Also very wrong.

That is the core problem with many invoice reports. They summarize activity after the risk window has closed. They are full of totals, aging buckets, cycle times, and exception counts. Useful, yes. Fraud-stopping, rarely.

The stakes are not theoretical. The FBI estimates insurance fraud costs the United States more than $308 billion per year, which ultimately pushes costs back onto families and businesses. In the payments world, the Association for Financial Professionals has reported widespread payments fraud attempts, with invoice and vendor payment schemes remaining a persistent headache for finance teams.

So when someone asks me what a better invoice report should look like, I do not start with charts. I start with questions.

What useful invoice reports should answer before payment

A fraud-focused invoice report is not a prettier spreadsheet. It is a decision tool. If I am an AP manager, claims adjuster, fraud manager, or expense lead, I need it to answer a handful of practical questions fast.

The key questions are simple:

- Does this invoice look altered, synthetic, duplicated, or physically manipulated?

- Do the supplier details, payment details, and claim or purchase context agree with each other?

- Are the totals, taxes, dates, and line items mathematically and commercially plausible?

- Has this vendor, employee, claimant, or bank account appeared in suspicious patterns before?

- What evidence should I review before approving, rejecting, or escalating?

Notice what is missing from that list: a vague fraud score with no explanation. I have seen teams stare at risk scores like they are reading tea leaves. A score can help prioritize work, but only if the report explains the reason behind it.

This is where invoice reporting and invoice analytics start to overlap. If you want the deeper mechanics, we have written about how invoice analytics can reveal fraud before payment. The short version is that a useful report combines the document, the payment details, and the business context. Leaving out any one of those is like investigating a burglary while refusing to look at the door.

The four signals I want in every fraud-focused invoice report

A good invoice report should not drown the reviewer in data. It should surface the right signals with enough evidence to act. In my experience, four signal groups matter most.

Document integrity: has the file been touched?

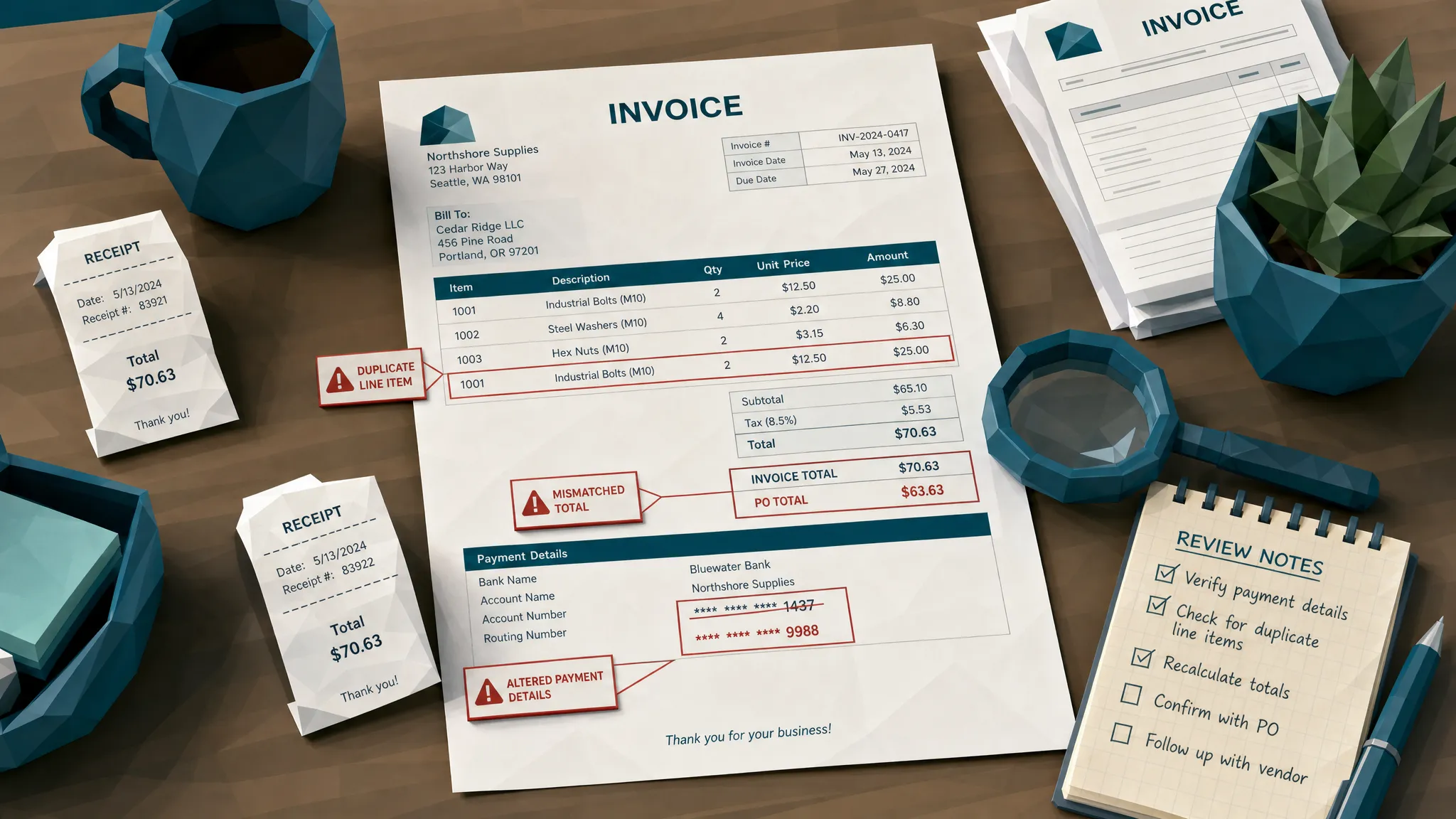

Fraudulent invoices often look normal because they are normal invoices with small changes. A bank account edited here, a total changed there, a date adjusted to fit a policy window. The best manipulation is boring. Nobody is submitting an invoice with a cartoon villain watermark on it, although I would personally appreciate the honesty.

Document integrity checks look for signs of tampering, including inconsistent pixels, suspicious compression, missing or odd metadata, mismatched fonts, cloned areas, and edits that do not align with how the file should have been created. In claim environments, this also includes photos of receipts or invoices that may have been printed, altered, re-photographed, or generated from scratch.

A good invoice report does not simply say suspicious document. It shows the reviewer where the issue appears and what kind of manipulation may be present. That matters because a claims handler or AP reviewer needs to make a defensible decision, not just follow a blinking red light.

Payment context: does the money go where the story says it should?

Payment details are where many fraud attempts reveal themselves. A real vendor name paired with a new bank account. A familiar invoice template routed to a different beneficiary. A construction invoice submitted through a claim file, but the payment destination has no relationship to the contractor.

This is why I am skeptical of tools that only ask, is this file real? Real files can still be weaponized. A legitimate invoice can be intercepted and edited. A legitimate vendor can be impersonated. A legitimate employee can upload the same receipt twice with just enough cropping to look different.

The report should connect the document to the payee, bank details, historical vendor records, claimant information, purchase order data where available, and prior payments. When those pieces disagree, the reviewer should see the conflict immediately.

Math and chronology: do the numbers and dates behave?

Fraudsters are often creative with images and lazy with arithmetic. I say that lovingly, because bad tax math has saved more money than some board-approved transformation programs.

A fraud-focused invoice report should flag totals that do not add up, tax amounts that do not match the jurisdiction or rate, line items that repeat awkwardly, invoice numbers that jump out of sequence, and dates that make no sense. In insurance claims, chronology is especially important. If the repair invoice predates the loss event, someone needs more coffee, or more likely, a deeper review.

Pattern behavior: is this invoice part of a cluster?

One odd invoice can be a mistake. Five odd invoices sharing a bank account, layout, email domain, or claimant address are something else.

Useful invoice reports should help reviewers see patterns across time. Duplicate submissions, near-duplicate documents, repeat vendors with unusual approval behavior, employees whose receipts always land just under approval thresholds, and claimants who submit invoices from a suspiciously tight circle of providers all deserve attention.

This is where manual review starts to creak. A person can remember the weird invoice from Tuesday. They cannot reliably remember every altered PDF, vendor alias, and reused payment detail from the past eighteen months.

A simple example: the contractor invoice that looks fine

Let’s make this concrete. Imagine a home insurance claim after water damage. The claimant submits a contractor invoice for kitchen repairs. The vendor appears to be a real renovation business, the work type makes sense, and the total sits comfortably within the adjuster’s expected range.

In the real world, a reviewer might verify that the business exists by checking a contractor’s website, for example a renovation company such as Revo Craft Renovations, then move on. That is a reasonable first step. It is not enough.

The invoice report should ask the next questions. Does the invoice metadata match the claimed creation path? Have the bank details changed from prior invoices? Does the logo show signs of being pasted over another document? Do the labor and material totals add up? Does the payment account appear elsewhere in unrelated claims? Is the invoice number consistent with prior documents from the same supplier?

This is where many fraud attempts slip through. The vendor may be real, but the document may be altered. The work may be real, but the amount may be inflated. The claimant may be genuine, but the payment destination may have been redirected. Fraud loves partial truth. It gives the reviewer just enough comfort to stop asking questions.

Report design matters more than people think

A messy report can hide fraud as effectively as a missing control. I have seen reports with every useful data point included, technically, but scattered across seven tabs, three exports, and a dashboard that looked like a cockpit designed by a committee of raccoons.

The best invoice reports are built around reviewer behavior. Busy people do not need more columns. They need a clear queue, a plain explanation, and a way to see the evidence quickly.

In practice, that means every flagged invoice should have a short risk narrative. Something like: bank account changed from prior vendor record, PDF metadata inconsistent with original source, subtotal and tax do not reconcile, visually similar invoice submitted last month by another claimant. That kind of explanation is much more useful than high risk, 87.

It also means the report should separate severity from confidence. A possible duplicate for a $90 meal receipt is not the same as a manipulated vendor invoice for $190,000. Both may deserve review, but they should not compete equally for attention.

And yes, screenshots or visual evidence matter. If an invoice looks manipulated at the pixel level, show the area of concern. If metadata is odd, show what changed. If payment details conflict with history, show the previous and current values side by side in a controlled review view. Reviewers trust reports that let them inspect the evidence.

The metrics that actually help leadership

Executives need summary reporting, but the wrong metrics can create perverse incentives. If leadership only sees processing speed, teams will optimize for speed. If they only see fraud caught after payment, they will underestimate near misses and prevented losses.

For leadership, I like invoice reports that show prevented payment value, value under review, confirmed fraud, false positives, review cycle time, repeat offender patterns, and control gaps by business unit or claim type. That gives finance, audit, and fraud teams a shared view of where risk is entering the process.

The ACFE Report to the Nations has long shown that occupational fraud can impose major costs on organizations, often over long periods before detection. The lesson for invoice reporting is straightforward: measure detection before loss, not only investigation after loss.

For AP teams, business email compromise is another reason reporting has to include payment context. The FBI IC3 2023 report highlighted billions in losses tied to business email compromise, much of it aimed at payment processes. If your invoice report cannot show sudden bank detail changes, unusual payee routing, or vendor identity mismatches, it is leaving the front door politely unlocked.

Why standard invoice software often misses the thing you care about

Many invoice systems are excellent at capture, routing, approval, and payment. That is their job. But fraud often lives in the original document and the surrounding context, not just the fields extracted from it.

If a system reads an invoice total correctly, matches it to a purchase order, and routes it to the right approver, it may consider the process successful. But what if the invoice image was edited before submission? What if the bank account was changed inside the PDF, while the vendor name stayed the same? What if the receipt is a synthetic image that looks convincing enough for a quick glance?

That is why we argue that traditional tools need a document-level fraud layer. If this sounds familiar, the deeper explanation is in our piece on why invoice software still misses document fraud.

The practical point is this: invoice reports should not depend solely on extracted text. They should preserve and analyze the original file, the visual structure, the metadata, the math, and the payment relationship. Otherwise, the report may faithfully summarize bad inputs.

Or as one finance director once told me after a duplicate payment review, the system did exactly what we asked. Unfortunately, we asked the wrong question.

What Docklands AI looks for in invoice reports

At Docklands AI, we think invoice reports should help teams stop suspicious payments before they become awkward post-mortems. The platform analyzes invoices and receipts for signs of manipulation, including AI-generated documents, Photoshop-style tampering, metadata anomalies, mathematical irregularities, and physical manipulation.

The important part is context. Docklands also uses payment information from a claim, expense, or payment workflow to build a deeper fraud picture. That helps teams move beyond a narrow file authenticity check and toward a more practical question: does this document, this payee, and this payment request make sense together?

For insurance claims, that can mean reviewing repair invoices, receipts, and supporting documents before payout. For accounts payable, it can mean screening vendor invoices where purchase order procedures are incomplete or unavailable. For employee expenses, it can mean finding altered receipts, duplicate submissions, or suspicious patterns without asking managers to become amateur document examiners.

Reports should support action, too. Real-time reporting, analytics, API and webhook integration, executive dashboards, multiple user and project support, and secure access controls such as 2FA all matter because fraud review is a workflow, not a side quest.

Common reporting mistakes I would retire tomorrow

If I could quietly remove three habits from invoice reporting, I would start with after-payment dashboards that look impressive but arrive too late. They are useful for audit and recovery, but they do not prevent the first loss.

Second, I would retire reports that treat all exceptions equally. A missing PO number, a changed bank account, and a manipulated invoice image do not belong in the same generic exception bucket. That is how important signals get buried under administrative noise.

Third, I would stop reporting fraud as if it were only a finance problem. Invoices show up in AP, insurance claims, warranty claims, payroll reimbursements, and employee expenses. The same manipulated receipt can be a tiny expense issue in one company and a repeat claims pattern in another. Reporting needs to follow the document and the money, not just the department code.

Frequently Asked Questions

What should invoice reports include to help stop fraud? Useful invoice reports should include document integrity signals, payment context, math checks, duplicate detection, vendor or claimant history, and clear evidence for reviewers. The goal is to prioritize suspicious invoices before payment, not simply summarize processing activity after the fact.

Are invoice reports different from invoice analytics? Yes, although they overlap. Invoice analytics finds patterns and risk signals across documents, payments, vendors, employees, and claims. Invoice reports package those findings into a workflow that reviewers and leaders can use to make decisions.

Can invoice reports catch manipulated PDFs and receipts? They can if the reporting process includes document forensics. Standard OCR or approval reports may only read the visible fields. Fraud-focused reports look at visual edits, metadata, pixel-level inconsistencies, mathematical irregularities, and suspicious payment changes.

Who needs fraud-focused invoice reports? AP managers, claims adjusters, fraud teams, expense managers, payroll teams, audit leaders, and insurance claim managers all benefit. Any team that approves invoices, receipts, or payment evidence before money moves should have reporting that highlights manipulation risk.

How often should teams review invoice fraud reports? High-risk workflows should be reviewed continuously or daily, especially before payment runs or claim payouts. Executive summaries can be weekly or monthly, but operational fraud queues need to be timely enough to stop loss.

Make your invoice reports harder for fraudsters to beat

The best invoice reports do not try to make reviewers paranoid. They make them precise. They cut through the harmless noise, surface the documents that deserve scrutiny, and explain the evidence clearly enough for a team to act before payment.

If your current reports mostly tell you what already happened, it may be time to redesign them around prevention. Docklands AI helps organizations detect manipulated, photoshopped, and AI-generated invoices and receipts using document forensics, payment context, and fraud-focused reporting built for real review workflows.

Request a Demo Today!

Book your demo below.