Theft Claim Fraud Usually Starts With Borrowed Proof

Here is my hot take: most theft claim fraud is not born from genius criminal planning. It usually starts with something painfully ordinary, a receipt from someone else, a photo pulled from an old claim, a screenshot from a marketplace listing, or a contractor invoice that was real once, just not for this loss.

I call this borrowed proof. It looks harmless on the surface because the document or image may be genuine. That is exactly what makes it annoying. A fake Rolex receipt is easy to mock. A real receipt for a real Rolex, submitted by the wrong person for the wrong incident, is where claims teams earn their coffee.

The FBI estimates that insurance fraud costs the United States more than $308 billion per year. Theft claims are only one slice of that, but they are a fertile slice because they often rely heavily on claimant-supplied proof: purchase receipts, product photos, police reports, repair estimates, appraisals, bank statements, and screenshots.

And in 2026, “proof” has never been easier to borrow, alter, regenerate, or explain away.

Why theft claims are perfect for borrowed proof

Theft claims have a structural problem: the item is gone. In a fire claim, an adjuster may inspect the damage. In an auto collision, there is a vehicle. In a warranty claim, there may be a serial number and a failed part. But with theft, the central evidence often vanished with the alleged loss.

That means the file leans on supporting documents. The receipt becomes the object. The photo becomes the ownership story. The screenshot becomes the valuation anchor.

I once reviewed a theft claim for several high-end electronics where every receipt looked clean. Fonts matched, totals added up, store details were plausible. The problem was not the receipts. The problem was that one of the serial numbers had appeared in a prior unrelated claim from a different household. Nobody had forged the receipt in the traditional sense. Someone had borrowed a believable paper trail and wrapped a new story around it.

That is the uncomfortable bit. Many fraudulent theft claims do not look like fraud at first. They look like a customer being organized.

Borrowed proof comes in more flavors than people think

When claims teams hear “document fraud,” they often imagine a badly Photoshopped invoice with a crooked total and a font from 2009. I wish it were still that charming.

Borrowed proof usually falls into a few recognizable patterns.

A claimant may use a real receipt from a friend, relative, reseller, or previous owner. They may submit images from a marketplace listing and present them as proof of ownership. They may reuse a receipt from an old claim, changing only the date or the item description. They may provide a genuine invoice from a business they know, but for goods never purchased by them. In some cases, they may use an authentic document as a base and make small edits to the name, address, date, SKU, or payment details.

The reason this works is simple: real documents carry credibility. A borrowed receipt has the texture of reality. It may contain the right tax calculation, merchant address, SKU formatting, payment reference, and layout. Manual reviewers are trained to spot nonsense, not always misplaced truth.

This is why I get twitchy when a claim file contains “too perfect” evidence. Not because organized claimants are suspicious by default. Plenty of people keep good records. But when the documentation is neat, recent, high-value, and oddly detached from the claimant’s wider history, I want to know where it came from.

The document may be real, but the relationship may be fake

The biggest mistake in theft claim review is asking only, “Is this receipt real?”

Better questions are:

- Does this receipt belong to this claimant?

- Does the payment method match their financial footprint?

- Does the purchase date make sense with the ownership story?

- Do the item identifiers appear anywhere else?

- Does the document metadata agree with the stated timeline?

- Was the proof created, downloaded, edited, or photographed after the reported theft?

That last one catches more awkward silences than you might expect.

A receipt can be genuine and still fail the claim. A photo can be authentic and still not show the claimant’s property. A bank statement can show a payment and still not support the specific item claimed. Claims fraud often lives in the gap between authenticity and relevance.

This is why I like looking at the whole paper trail rather than a single document in isolation. We covered this broader principle in detecting insurance fraud through the paper trail, and theft claims are one of the clearest examples. The “gotcha” is rarely one dramatic clue. It is usually five small inconsistencies standing close together, pretending not to know each other.

The rise of synthetic evidence changes the game, but not the fundamentals

Yes, AI-generated images and edited documents have made theft claim fraud easier. A claimant can create a convincing photo of a watch on a kitchen counter, generate a plausible invoice layout, or alter a receipt without needing design skills.

According to a BBC report on Admiral’s claims experience, fraudulent claims rose sharply, with AI-generated fake images and deepfakes playing a growing role. Verisk’s 2025 fraud reporting has also highlighted changing consumer attitudes toward AI-altered claim evidence, including a striking generational divide.

But here is the part I think gets missed: synthetic evidence did not replace borrowed proof. It upgraded it.

Fraudsters do not always generate everything from scratch. More often, they take a real artifact and improve it. They clean up a receipt. They alter a date. They add a missing claimant name. They generate a “before theft” image based on a real marketplace photo. They make the borrowed proof fit better.

That means claims teams should not treat AI-generated evidence as a separate bucket. It belongs in the same family as manipulated receipts, reused invoices, and inconsistent payment details. The core question remains provenance: where did this proof come from, and does it truly connect to the claimant, the loss, and the claimed value?

The red flags I take seriously in theft claim fraud

I am not a fan of red-flag bingo. One suspicious detail does not make a fraud case. People make mistakes. Retail systems produce ugly receipts. Phones strip metadata. Police reports can be thin. Life is messy, and insurance files are messier.

Still, certain patterns deserve attention.

One of the strongest indicators is a receipt that looks valid but has weak ownership linkage. For example, the payment method is cropped out, the last four digits do not match known cards, or the claimant cannot explain how they paid. Another is a receipt or invoice created after the theft date, especially when the claimant insists it was an old record they “just found.”

I also pay attention to product photos that appear too generic. If a stolen bicycle photo looks like it came from a retailer listing, check it. If jewelry photos have inconsistent backgrounds, lighting, or metadata, check them. If serial numbers are missing from high-value electronics, check why.

Then there are timeline issues. A claimant reports a laptop stolen on Monday, submits a receipt on Tuesday, and the image file shows it was edited Wednesday morning. Could be innocent. Could be a scanner app. Could be someone tidying up a document. But it belongs in the review conversation.

The most overlooked red flag is document clustering. Fraudulent theft claims often contain proof that shares hidden similarities: the same device used to photograph multiple “old” receipts, identical cropping across different merchants, repeated metadata patterns, or file names that suggest the documents were collected in one sitting. Borrowed proof often arrives as a bundle.

Why manual review struggles with borrowed proof

A good adjuster can smell nonsense in a claim narrative. I have seen experienced handlers catch fraud from a single odd phrase in a statement. Human judgment still matters.

But borrowed proof is hard because it does not always look manipulated. Manual review is excellent at asking, “Does this make sense?” It is weaker at inspecting pixels, metadata, mathematical irregularities, file histories, and cross-document consistency across thousands of claims.

That is not a criticism of adjusters. It is a math problem and a boredom problem. Nobody should have to stare at receipt edges all afternoon trying to decide whether a shadow is natural or suspicious. That is how good people become cynical and bad receipts sneak through.

For theft claims, the review process needs to separate three questions that often get blended together.

First, is the document visually and technically authentic? Second, does the document support the claimed ownership and value? Third, does the document fit the rest of the claim file?

Traditional review often overweights the first question. Fraud detection needs all three.

Payment details are the underrated witness

If I had to pick one witness in a theft claim file, I would often pick the payment data. It is less glamorous than a photo and less dramatic than a claimant statement, but it is harder to bluff consistently.

A receipt says something was purchased. Payment details help show who purchased it, when, through which channel, and whether the transaction pattern makes sense. A card ending in 4821, a billing ZIP code, a merchant location, an authorization timestamp, and a refund trail can turn a nice-looking receipt into either solid support or a problem.

This is where many simple “is this image real?” checks fall short. A document can pass a visual authenticity check and still fail once payment information is compared against the claim story. In theft claim fraud, that distinction matters.

At Docklands AI, we focus on manipulated, photoshopped, and AI-generated invoices and receipts, but the bigger value comes from looking beyond the image alone. Payment information, document forensics, metadata, mathematical checks, and physical manipulation signals all help build a fuller fraud picture. The goal is not to accuse more people. The goal is to stop weak evidence from sailing through just because it looks tidy.

If you already think of claims fraud as a document problem, the next step is to think of it as a relationship problem: the relationship between the claimant, the document, the payment, the timeline, and the item.

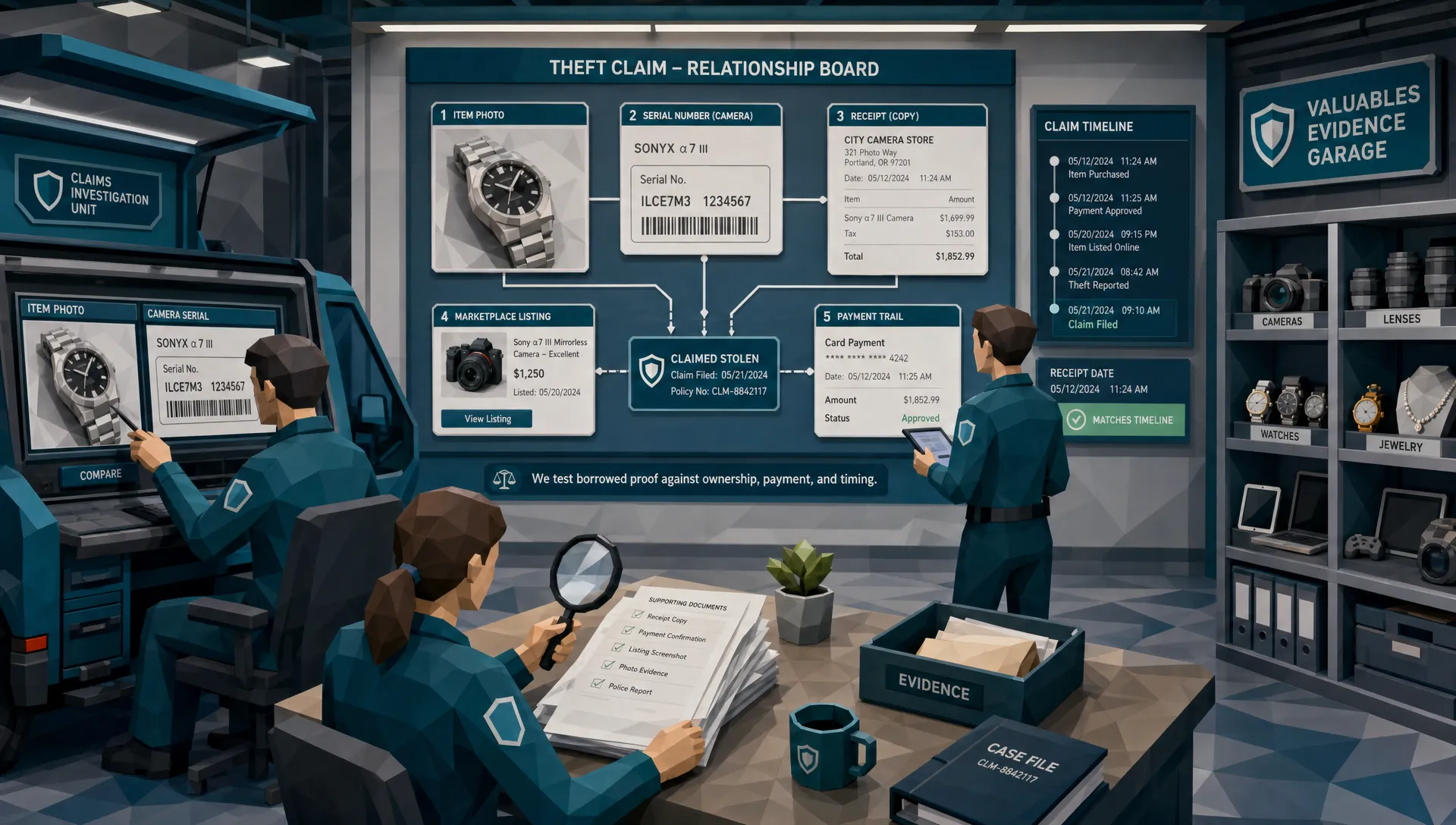

A simple example: the stolen camera that changed owners three times

Here is a version of a case I have seen in different forms.

A claimant reports a stolen camera kit worth several thousand dollars. They provide a receipt, product photos, and a list of lenses. The receipt is real. The store exists. The product SKUs match. The math works.

But the receipt is from two years earlier and paid with a card that does not belong to the claimant. The claimant says it was a gift. Fine, gifts happen. Then one of the product photos appears in an old resale listing. The claimant says they used the listing photo because their own photos were on the stolen camera. Also possible, though not ideal. Then the serial number from one lens appears in a prior claim tied to a different name. Now we have a pattern.

None of those details alone proves fraud. Together, they tell a story: the proof is real, but the ownership chain is not.

That is borrowed proof in its natural habitat. It hides behind plausible explanations until the file is viewed as a network rather than a stack of attachments.

Do not punish good customers for bad evidence habits

A quick caution because I have seen teams overcorrect.

People submit messy proof because normal people are not evidence librarians. They crop screenshots badly. They forward old emails. They photograph receipts on kitchen counters under yellow light. They lose boxes, manuals, and serial numbers. If having imperfect documentation made someone a fraudster, half the country would be in trouble before lunch.

The point is not to reject claims because a receipt looks odd. The point is to route higher-risk proof into a smarter review process.

A fair process should give claimants room to clarify, provide alternate proof, or explain ownership. It should also protect honest policyholders from premium increases caused by preventable fraud. The FBI notes that insurance fraud can add hundreds of dollars to annual premiums for the average family. That is the quiet tax nobody voted for.

There is a parallel here outside insurance too. In hiring, for example, a polished profile is not the same as a truthful profile, which is why legitimate services such as recruiter-led professional profile optimization focus on improving presentation without inventing credentials. In claims, we have the same basic duty in reverse: admire neat documentation if you like, but verify what it actually proves.

How claims teams can respond without slowing everything down

The answer is not to treat every theft claim like a crime scene. That would be expensive, slow, and deeply unpopular. The answer is to make the first review smarter.

Start by triaging documents based on risk. High-value theft claims, repeated losses, recent policy inception, unusual item categories, missing payment linkage, and compressed timelines should trigger closer evidence review. Then examine the submitted proof as a connected set, not as separate attachments.

Look for provenance. Where did each file originate? When was it created? Has it been edited? Does the receipt’s payment information align with the claimant? Do product photos appear elsewhere online? Do serial numbers, invoice numbers, or merchant details recur across claims?

Just as important, record what “normal” looks like for your book of business. Fraud detection improves when teams understand common merchant formats, typical receipt capture methods, normal claim timelines, and ordinary customer behavior. You cannot spot strange if you have never defined normal.

If your current process relies mostly on OCR, manual review, and basic duplicate checks, borrowed proof will continue to slip through. OCR can read text, but it cannot tell you whether the document’s story is true. Manual review can catch obvious issues, but it does not scale well. Basic duplicate matching helps, but fraudsters have learned to make tiny changes.

For a deeper dive into the mechanics of altered proof, our article on how fraud in claims often starts with document manipulation breaks down the common tampering methods that claims teams should understand.

The future of theft claim fraud is boring, which is bad news

The scariest fraud is not always the cinematic kind. It is the boring kind that fits into normal workflows.

Borrowed proof works because it resembles the everyday clutter of claims handling. A receipt here. A screenshot there. A photo with no metadata. A claimant who says, “That’s all I have.” The file feels familiar, so it moves.

That is why I think theft claim fraud prevention needs to become less obsessed with spotting fake-looking documents and more focused on verifying document relationships. Does this proof belong here? Does it belong to this person? Does it support this loss? Does the payment trail agree? Do the files behave like they were created when and how the claimant says they were?

When claims teams ask those questions early, borrowed proof becomes much less useful.

Frequently Asked Questions

What is theft claim fraud? Theft claim fraud occurs when someone exaggerates, fabricates, or misrepresents a theft loss to receive an insurance payout. It can involve fake ownership, inflated values, staged thefts, altered receipts, reused photos, or genuine documents submitted for items the claimant did not own.

What does “borrowed proof” mean in an insurance claim? Borrowed proof means evidence that may be real but does not genuinely belong to the claimant or the reported loss. Examples include a friend’s receipt, an online listing photo, a prior claim document, or an invoice for an item purchased by someone else.

Can a real receipt still be used fraudulently? Yes. A receipt can be authentic and still be misleading if it does not prove the claimant owned the item, paid for it, or lost it in the reported theft. Claims teams should verify the relationship between the receipt, payment method, item, claimant, and timeline.

Why are theft claims vulnerable to document fraud? Theft claims are vulnerable because the stolen property is often unavailable for inspection. That puts more weight on receipts, photos, appraisals, and payment records, which can be borrowed, edited, reused, or generated.

How can insurers detect borrowed proof faster? Insurers can improve detection by reviewing document metadata, payment details, visual manipulation signals, serial numbers, duplicate evidence, and timeline consistency. Automated forensic checks can help route suspicious claims for closer review without slowing down legitimate claims.

Stop borrowed proof before it becomes a paid claim

Theft claim fraud rarely announces itself with a neon sign. More often, it arrives as a clean receipt, a plausible photo, and a story that almost fits.

Docklands AI helps claims teams detect manipulated, photoshopped, and AI-generated invoices and receipts using forensic analysis, metadata checks, mathematical irregularity detection, and payment-based fraud signals. If your team is still reviewing theft claim evidence attachment by attachment, it may be time to look at the relationships hiding inside the file.

Visit Docklands AI to see how stronger document fraud detection can help protect claims outcomes before borrowed proof turns into real loss.

Request a Demo Today!

Book your demo below.