What Insurance Company Investigators Check First

Hot take from a decade in fraud work: the first thing insurance company investigators check is rarely the dramatic photo. The photo gets attention. The boring stuff gets results.

I know, that is not very cinematic. Nobody greenlights a crime drama where the investigator says, with great intensity, I need to compare the invoice date with the bank account name. But in real claims work, that is where a surprising number of bad claims start to wobble.

The stakes are not small either. The FBI estimates that insurance fraud, excluding health insurance, costs more than $40 billion a year in the U.S. and adds an estimated $400 to $700 to the average family’s annual premiums. So yes, we check the dramatic photos. But first, we check whether the claim behaves like a real event that happened in the real world.

The first check is whether the claim can keep time

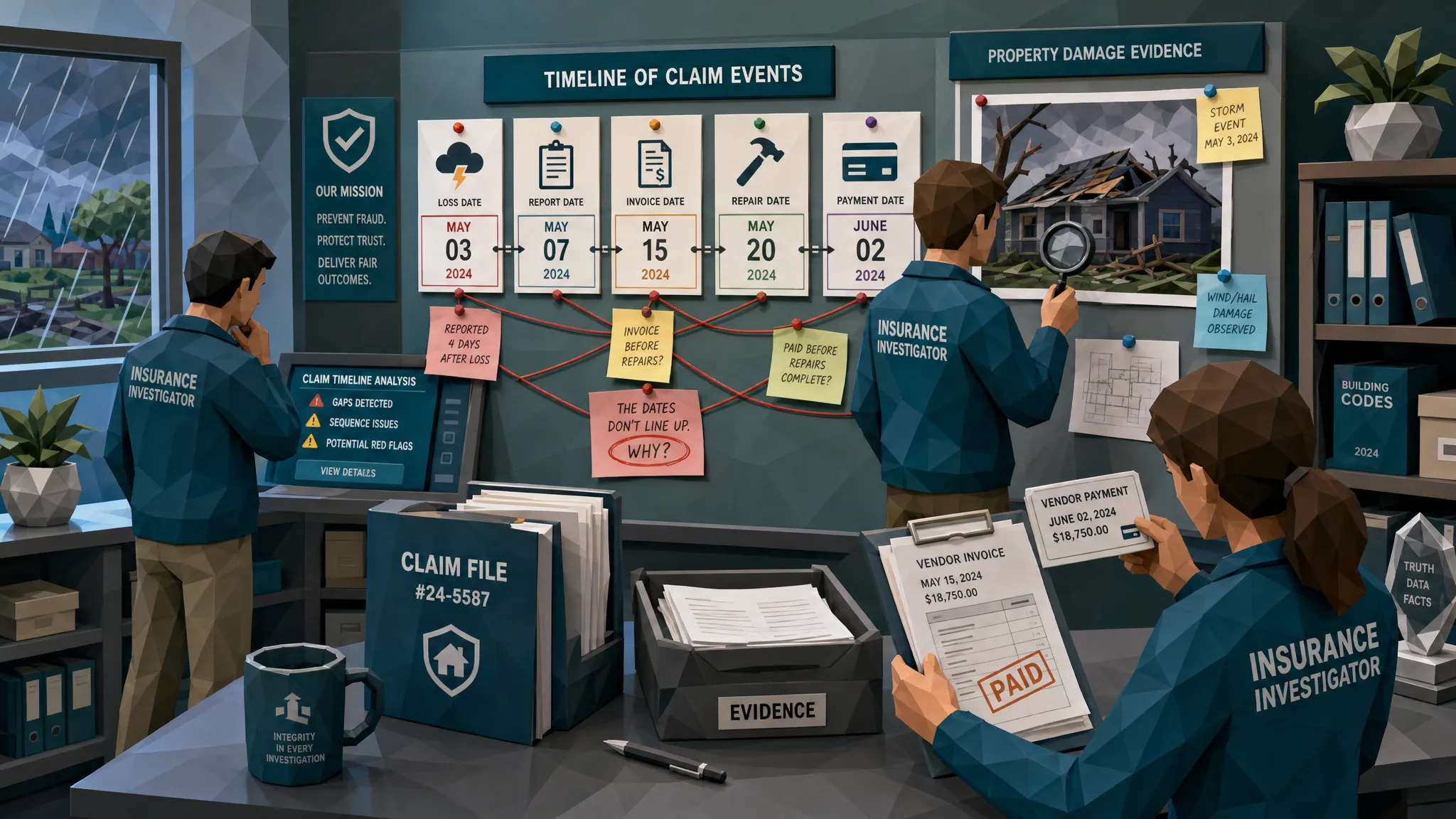

The timeline is the first lie detector, and it does not need batteries.

When I open a suspicious claim, I want to know when the loss allegedly happened, when it was discovered, when it was reported, when documents were created, when repairs were done, and when money moved. A legitimate claim can have messy timing, of course. People travel, contractors delay paperwork, phones die, storm damage is discovered late. Life is a badly stapled folder.

But fraud often has a timeline problem because the story is assembled backward. The claimant knows what payout they want, then they build the evidence to fit. That is how you get an invoice dated before the storm, a repair estimate created minutes after the accident, or a receipt from a vendor that was closed on the day of purchase.

One of my favorite simple examples was a property claim where the roof repair invoice looked perfectly normal. Logo, line items, tax, payment terms, the whole costume. The issue was that the invoice date was the day before the hail event. Maybe the roofer had a crystal ball. More likely, someone copied an old invoice template and forgot that weather has a calendar.

This is why I tell newer investigators to start with the calendar. Before you debate motive, look at sequence.

Next comes coverage, because timing has a cousin

After the timeline, I look at coverage fit. Did the policy exist at the time of loss? Was there a recent change in limits? Was coverage added shortly before the event? Does the claimed damage fall inside the policy terms, warranty conditions, or health plan rules?

This is not about assuming guilt when someone files soon after buying a policy. Plenty of people buy insurance, then immediately have bad luck. That is what insurance is for, and the universe has a dark sense of humor.

Still, investigators pay attention to claims that appear right after inception, right after a coverage increase, right before cancellation, or immediately after a deductible change. In warranty claims, that might mean a repair request just after registration. In health insurance, it might mean documents that do not align with provider records or treatment dates. In home and P&C claims, it often means the loss date has to work very hard to fit the policy window.

The question is simple: does the claimed event match the contract and the claimant’s behavior around that contract?

Then we read documents like they are witnesses

Invoices, receipts, estimates, medical bills, proof of ownership, repair reports, and contractor statements are not admin clutter. They are witnesses with timestamps, habits, formatting, and sometimes very poor poker faces.

This is where the paper trail earns its keep. If you want a deeper dive into why the ordinary-looking documents matter so much, Docklands has a useful breakdown on why detecting insurance fraud starts with the paper trail.

In the first pass, I am usually looking for the same categories of oddness: totals that do not add up, tax that is calculated strangely, fonts that change halfway down a receipt, line items that do not match the loss, vendor details that are vague, invoice numbers that look invented, and documents that appear too clean for the situation they describe.

That last one sounds subjective, so let me explain. A receipt for emergency supplies after a basement flood may be photographed on a kitchen counter, slightly wrinkled, with imperfect lighting. A suspicious version may arrive as a flawless digital document with no realistic purchase trail, no card record, no matching merchant footprint, and no reason it should exist in that form.

Fraudsters used to need a friend with editing software. Now, anyone with an internet connection can generate or alter claim evidence. The BBC reported that Admiral saw a 71% rise in fraudulent claims, with AI-generated images and deepfakes contributing to the problem. That does not mean every polished document is fake. It means polish is no longer proof of legitimacy.

The payment trail gets checked earlier than many people realize

Here is my very practical opinion: payment details are underrated.

A forged invoice can look beautiful, but money has to land somewhere. Investigators check whether the vendor name matches the payee, whether bank details changed recently, whether payment instructions make sense, and whether the claimant is asking for reimbursement in a way that bypasses normal vendor relationships.

I once saw a contractor invoice that looked fine until the payment went to an individual account with the same surname as the claimant. Was that automatically fraud? No. Small contractors can operate messily. But it moved the claim from normal review to please explain this like I am holding a coffee and have only three minutes.

False evidence often falls apart when documents, payments, and vendor details are compared side by side. That is why reviewing how false insurance claim evidence falls apart under review is useful for claims teams trying to tighten their first-pass process.

Photos and metadata matter, but I do not worship metadata

Photos are important, especially in property, auto, warranty, and contents claims. Investigators look at whether images match the reported damage, whether lighting and shadows make sense, whether the same damage appears in multiple claims, whether the room or vehicle context fits, and whether the photo appears edited or generated.

Metadata can help too. Device information, timestamps, location data, software history, and file creation details can all provide useful clues. But metadata is not a judge. It is a witness, and witnesses can be missing, confused, or stripped out by ordinary technology.

A photo with no metadata is not automatically suspicious. Many messaging apps and claim portals remove it. A photo with metadata is not automatically true either. Metadata can be altered, copied, or inconsistent for boring reasons.

The better question is whether the photo agrees with the rest of the file. Does the image timestamp line up with the loss date? Does the damage match the invoice? Does the room match previous inspection photos? Does the claimed item appear newer, older, repaired, or staged?

According to Verisk’s 2025 fraud research, 76% of carriers said claims manipulation became more sophisticated in the prior year. That tracks with what many of us see: the single piece of evidence is less reliable than the relationship between all the evidence.

Vendor and claimant patterns come into view quickly

By the time I have checked the timeline, coverage, documents, payments, and photos, I am usually looking for patterns.

Do the same vendors appear across unrelated suspicious claims? Do invoices share the same formatting quirks? Are phone numbers, addresses, email domains, or bank details reused? Has the claimant filed similar losses before? Does the repair cost sit oddly high compared with the damage shown?

This is where experienced investigators become annoyingly good at spotting echoes. A fake invoice template has habits. A staged claim has habits. So does a claimant who has learned just enough about the process to be dangerous.

We have to be careful here. Pattern checking should never turn into unfair profiling or lazy suspicion. The goal is to compare behavior and evidence, not make assumptions about a person. Good fraud work protects honest policyholders as much as it protects the insurer.

The interview usually comes after document review

People imagine the investigator starts with a tense interview. In my experience, that is usually backward.

If you interview too early, you ask vague questions and get vague answers. If you review the documents first, you ask useful questions. What made you choose that contractor? When did you receive the invoice? How did you pay? Why does the repair estimate predate the inspection? Can you provide the original receipt rather than a screenshot?

The best questions are calm, specific, and boring. That is when the story either becomes clearer or starts shedding parts like an old suitcase.

I once had a claimant explain, very confidently, that a receipt had been issued at the store counter on Saturday afternoon. The document data suggested it had been created on a phone Sunday evening. That did not close the file by itself, but it gave us the right follow-up questions. A good investigation is built from those moments.

My preferred first-pass order

If I were training a new investigator tomorrow morning, coffee in hand, I would give them this order:

- Timeline integrity: Check whether the loss date, report date, document dates, repair dates, and payment dates can all live in the same universe.

- Coverage fit: Confirm the policy, limits, waiting periods, exclusions, endorsements, and recent changes align with the claimed loss.

- Document consistency: Review invoices, receipts, estimates, bills, and reports for formatting issues, math errors, duplicate content, and signs of alteration.

- Payment logic: Compare vendor names, payees, bank details, reimbursement requests, and proof of payment.

- Photo credibility: Check whether images match the damage, location, timing, and supporting documents.

- Metadata and file history: Use timestamps, device details, software traces, and upload history as clues, not final proof.

- Vendor and claimant patterns: Look for repeated entities, shared contact details, unusual claim histories, and template reuse.

- Targeted follow-up: Interview the claimant, vendor, or provider only after you know which gaps need explaining.

This order is not sacred. A suspicious claim may demand a different route. But as a first pass, it keeps investigators focused on evidence instead of vibes.

A fair warning: early checks are triage, not a verdict

The first checks are designed to decide what deserves deeper review. They are not supposed to turn every typo into a fraud referral.

A legitimate invoice can have a typo. A real contractor can use ugly templates. A claimant can misremember a date. A genuine receipt can be photographed badly. If we treated every oddity as fraud, claims operations would grind to a halt and honest customers would suffer.

The skill is knowing when several small inconsistencies point in the same direction. One mismatch is a question. Three or four mismatches, especially across documents, photos, payment details, and timeline, become a pattern.

This is also why structured fraud scoring and document-level review should work together. Models can help prioritize claims, but document forensics helps explain what is actually wrong with the evidence. Docklands has more on that distinction in its guide to insurance claim fraud detection models vs document forensics.

Frequently Asked Questions

Do insurance company investigators check social media first? Usually, no. Social media can be useful in certain claims, but investigators typically start with the claim file, timeline, coverage, documents, payments, and photos. Public posts may support or contradict evidence, but they rarely replace the core file review.

What makes a receipt suspicious in an insurance claim? Common red flags include mismatched dates, incorrect totals, strange tax calculations, inconsistent fonts, missing merchant details, reused receipt numbers, suspicious screenshots, and payment records that do not match the receipt.

Can metadata prove a claim is fraudulent? Metadata can support an investigation, but it usually should not be treated as proof on its own. File data can be missing or altered for innocent reasons. The strongest findings come when metadata conflicts with the timeline, documents, photos, and payment trail.

What do investigators check first in property claims? In property claims, investigators often start with the loss timeline, policy status, photos of damage, repair estimates, invoices, contractor details, weather or incident data, and proof of payment.

How can claims teams speed up first-pass fraud review? Standardize the first checks, preserve original files, compare documents against payment details, and use forensic tools to flag manipulation, document generation, metadata issues, and math irregularities before payment decisions are made.

Make the first check harder to fool

Fraudsters are getting better at making invoices, receipts, and images look believable. The good news is that believable is not the same as consistent.

Docklands AI helps claims teams examine invoices and receipts for manipulation, AI-generated documents, metadata issues, mathematical irregularities, and physical tampering. It also uses payment information to build a deeper fraud picture, which is where many weak document checks fall short.

If your team is still relying on manual review alone, the first suspicious claim you miss may look perfectly ordinary. That is the problem. The expensive ones usually do.

Request a Demo Today!

Book your demo below.