Doctored Invoices Look Normal Until You Check the Math

My hot take after a decade of looking at suspect claims, expenses, and supplier payments: the most underrated fraud detector is still a calculator.

Yes, doctored invoices can look beautifully boring. The logo is crisp. The VAT number sits where it should. The font looks close enough to official. The PDF opens without screaming, “I was edited in a panic at 11:48 p.m.” But when someone changes an invoice, they usually change the number they care about and forget the small numbers that orbit it.

That is where the fun starts.

I once reviewed a contractor invoice that had all the right furniture: address, purchase order reference, itemized labor, materials, and a signature that looked like it had survived three photocopiers and a coffee spill. At a glance, everyone liked it. Then we recalculated the tax. The subtotal had been lifted by a few thousand dollars, but the tax amount still matched the original lower subtotal. The fraudster had edited the headline number and left the supporting math behind like footprints in wet cement.

That is the thing about doctored invoices. They often pass the “does this look normal?” test. They fail the “does this add up?” test.

Why doctored invoices survive a visual review

Most invoice review is built around pattern recognition. We look for a known vendor, a familiar layout, a reasonable amount, and an approval trail. In accounts payable, the reviewer is under time pressure. In insurance claims, the adjustor has a queue that seems to reproduce overnight. In employee expenses, a manager may approve receipts between meetings while pretending to listen to a quarterly planning call.

Fraudsters know this. They do not need to create a perfect document. They need to create a document that looks ordinary for three seconds.

That is why altered invoices often hide in plain sight. A changed total may sit in the same font family. A fake line item may be aligned closely enough. A claim invoice may be photographed at a slight angle, which conveniently hides pixel artifacts. A receipt may be crumpled, partly shadowed, or uploaded as a low-resolution image, which is the document equivalent of wearing sunglasses indoors.

The problem is that humans are much better at spotting ugly design than broken arithmetic. A bad logo jumps out. A tax calculation that is 1.7% off does not.

This is why I like math checks. They are boring, stubborn, and surprisingly hard to fool at scale.

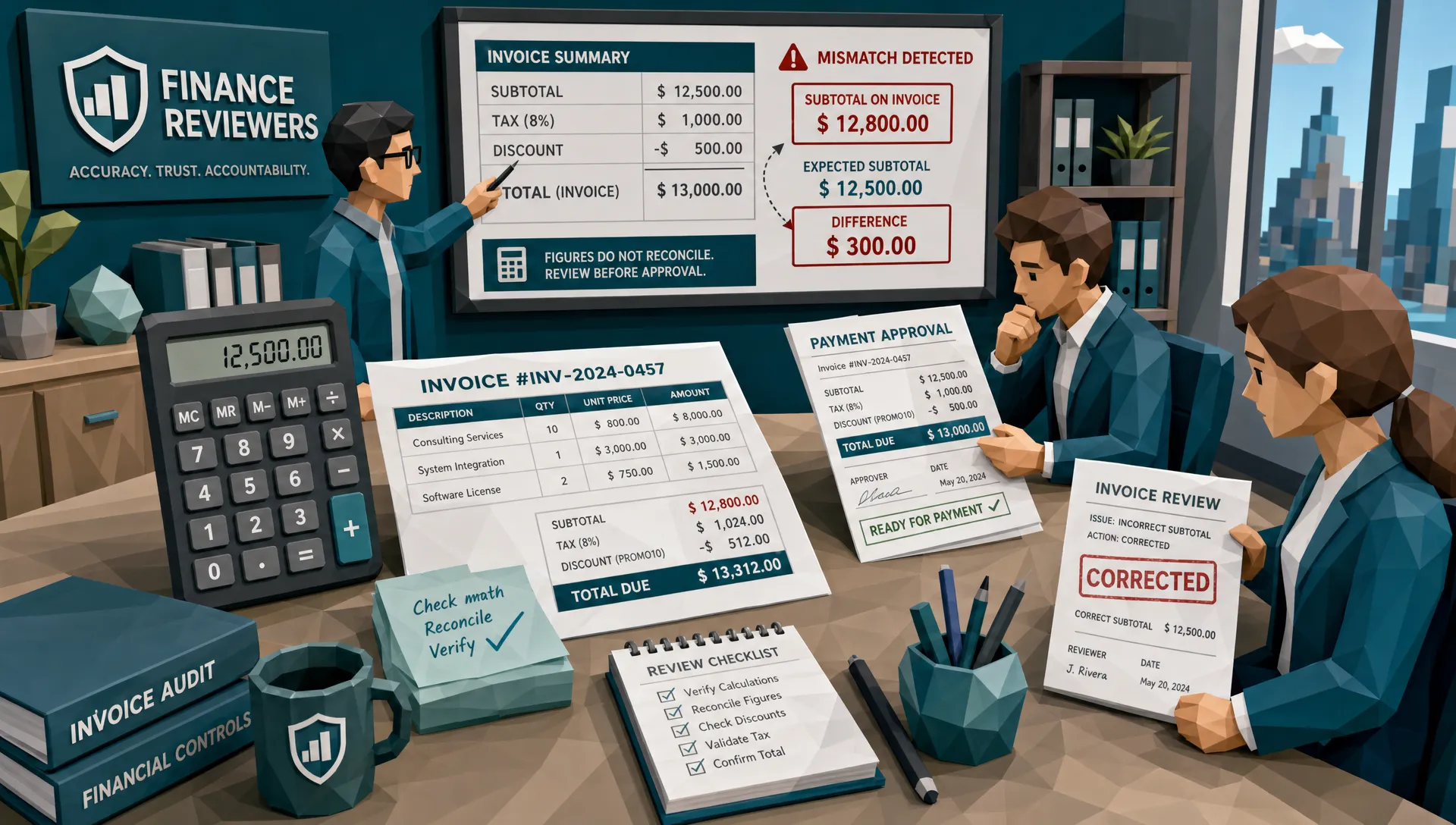

The first rule: totals are never alone

An invoice total is not a standalone fact. It is the final answer to a chain of smaller claims.

If the invoice says the total is $12,840, that number should be supported by quantities, unit prices, discounts, taxes, shipping, service fees, deposits, credits, and payment terms. If one piece changes, the others usually need to change too. Fraudsters often forget this because they are focused on the payout amount.

A common doctored invoice move is to inflate the total while leaving the subtotal or tax untouched. Another is to add a line item without updating the grand total properly. Sometimes the fraudster edits a quantity from “2” to “12” but forgets that the per-unit amount, discount, or tax class should change as well.

In claims work, I have seen repair invoices where the materials total increased, but the labor hours stayed suspiciously tidy. In AP, I have seen supplier invoices where a discount was applied to the original amount, not the altered amount. In employee expenses, the classic is a receipt where the tip, tax, and final total are mathematically incompatible. My favorite excuse was, “The camera must have stretched the receipt.” It had not stretched the multiplication.

The practical lesson is simple: do not ask whether the total looks plausible. Ask whether the total has parents, siblings, and a family resemblance.

The math errors I trust most

Some invoice irregularities are innocent. Vendors make mistakes. OCR misreads numbers. People transpose digits. I have fat-fingered enough spreadsheets to remain humble.

But certain patterns deserve attention, especially when they appear alongside unusual payment details, suspicious metadata, or a claimant with a conveniently urgent story.

The most useful math checks are usually the simplest ones:

- Recalculate line items from quantity and unit price.

- Rebuild the subtotal from the line items, not from the printed subtotal.

- Check that discounts apply to the right base amount.

- Confirm tax is calculated using the correct rate and taxable items.

- Compare shipping, handling, and service fees against the vendor’s normal pattern.

- Check whether deposits, credits, or prior payments reduce the balance correctly.

- Compare the payment requested with the amount actually due.

That last one matters more than people think. In invoice fraud, the document may be a prop. The payment instruction is often the real target.

The FBI’s 2023 Internet Crime Report reported more than $2.9 billion in business email compromise losses, much of it tied to payment diversion and vendor impersonation. A doctored invoice with a convincing total and a newly changed bank account is not a paperwork issue. It is a payment control issue wearing a PDF costume.

Rounding is where sloppy fraud goes to die

Rounding errors are tiny, but they are loud if you know how to listen.

Real accounting systems tend to round consistently. They apply tax rules in predictable ways. They handle discounts, currency conversion, and cents with boring discipline. Doctored invoices, especially those edited manually, often do not.

Here is a simple example. Suppose an invoice has three taxable line items, a discount, and a 7.5% tax rate. A real system will usually calculate tax after the discount if the discount reduces the taxable base. A fraudster may add the tax on the pre-discount amount, or worse, edit the grand total and leave the tax as a decorative number.

In cross-border expense claims, currency adds another trap. An employee may submit a receipt in AED, EUR, or GBP, then claim reimbursement in USD. The exchange rate should make sense for the transaction date, card posting date, or company policy. When the claimed amount uses a suspiciously favorable rate, I want to know why. When the same receipt appears twice with two different conversion rates, I want coffee and the original file.

Rounding alone should not convict anyone. But in my experience, it is a wonderful smoke detector. It tells you where to look before the fire reaches the payment run.

The line-item reality check

Math is not only arithmetic. It is also commercial reality.

A claim invoice for a flooded kitchen should not include materials that do not belong in a kitchen repair. A warranty repair invoice should not contain labor hours that exceed the shop’s opening hours. A supplier invoice for office stationery should not suddenly include industrial equipment unless there is a very good explanation. And yes, sometimes the explanation is good. Fraud review should be skeptical, not smug.

This is where vendor context helps. Legitimate marketplaces can sell a broad mix of products under one brand, so mixed categories are not automatically suspicious. For example, a reviewer looking at UAE purchases should understand that a marketplace offering groceries, stationery, home décor, and personal care in one place can produce a varied basket that is perfectly normal. The question is not “Are these categories different?” The question is “Do the quantities, prices, taxes, shipping charges, and payment trail make sense together?”

That distinction matters. Bad fraud detection overreacts to odd-looking documents. Good fraud detection separates unusual from impossible.

Why doctored invoices often break when tied to payment data

A doctored invoice may look convincing in isolation. Pair it with payment data and it often starts sweating.

If a supplier invoice says the amount due is $18,250, what was actually paid last time? Is this bank account new? Does the payment reference match the invoice number? Does the vendor usually invoice on the 15th, but this one arrived at 2:00 a.m. on a Saturday? Was the invoice submitted from the same email domain as previous invoices? Is the claim amount aligned with the invoice total, or did someone upload a document for $4,600 and request $6,400?

This is why I am wary of systems that treat invoices like isolated images. A document can be visually neat and financially nonsensical. The deeper fraud picture comes from the relationship between the document, the claimant or vendor, the payment instruction, and the approval path.

This also explains why a tampered invoice rarely fails in just one place. We have written about that broader pattern before in A Tampered Invoice Rarely Fails in Just One Place, and math is usually one of the earliest cracks.

Insurance claims: the math behind inflated losses

In insurance, doctored invoices usually serve one of three purposes: inflate the cost, support a false event, or convert an ordinary loss into a bigger payout.

The FBI notes that insurance fraud is costly for families, including higher premiums, and estimates it adds hundreds of dollars per year to the average family’s premiums through non-health insurance fraud costs. Claims teams already know the pressure. The difficulty is that the document can look emotionally and operationally plausible. A homeowner had a fire. A driver needs repairs. A policyholder replaced stolen equipment.

The invoice may be real but altered. That is a tricky category. A real vendor name and real invoice template create trust, while the changed totals do the damage.

In property and casualty claims, I like to compare the invoice math with the physical story. If drywall replacement jumped from one room to four rooms, did the photos show four damaged rooms? If water mitigation hours doubled, did the equipment rental period also double? If a medical or health-related bill shows bundled services, do the codes, dates, and totals line up?

Fraudsters can edit numbers. They have a harder time making every related fact agree.

Accounts payable: the small math miss that becomes a big payment

AP fraud is often less dramatic than claims fraud, but the losses can be brutal because payments repeat.

The Association for Financial Professionals has reported widespread payment fraud attempts against organizations in its Payments Fraud and Control Survey. Anyone who has managed AP knows the battlefield: high invoice volume, vendor changes, rush approvals, partial POs, exceptions, and the occasional executive who forwards something with “Please handle today” as if policy is a decorative plant.

Doctored invoices exploit exceptions. They appear where three-way matching is weak, where purchase orders are not used, or where multi-site operations rely on local approvals. Construction, facilities, healthcare groups, veterinary rollups, care homes, and fast-growing startups are common examples because operations move quickly and documentation is messy.

The math check here is not only “Does the invoice add up?” It is also “Does this invoice add up compared with how this vendor normally bills us?”

A new service fee, a repeated delivery charge, a tax line on a non-taxable item, a total that does not match the contract rate, or a balance due that ignores a credit memo can all be signals. Not proof. Signals.

If your AP workflow is optimized to route approvals but not inspect tampering, you have a gap. We covered that gap in Invoice Workflow Software Has a Blind Spot for Tampering, and it is one of the reasons finance teams should not confuse automation with assurance.

Employee expenses: the most human math problem

Expense fraud is where I have heard the funniest explanations and seen the strangest math.

A receipt total changed from $48.19 to $84.19, but the tip stayed at $7.23. A rideshare receipt was submitted twice, once as transport and once as client entertainment, because apparently the car was very emotionally supportive. A hotel folio had a manually added “business fee” that did not appear in the tax calculation or payment summary.

The Association of Certified Fraud Examiners estimates in its Report to the Nations that organizations lose about 5% of revenue to fraud each year. Expense abuse may feel small compared with vendor fraud, but it spreads culturally. If employees learn that nobody checks the math, padding becomes casual. Casual fraud is still fraud. It just wears sneakers.

Managers should not need to become forensic accountants. They do need support that flags the suspicious math before approval. The best expense reviews compare receipt totals, tax, tip, merchant category, payment card data, duplicate submissions, and policy limits. A receipt that passes OCR may still fail basic sense.

Do not treat every mismatch as fraud

Here is the part that keeps us honest: math mismatches are not always malicious.

Vendors use different rounding rules. Taxes vary by jurisdiction and product type. Tips may be calculated after discounts. Shipping can be taxable in one place and not in another. OCR can mistake an 8 for a 3, especially on a wrinkled receipt photographed under lighting that belongs in a haunted basement.

The point is not to reject every invoice with a one-cent discrepancy. The point is to prioritize review intelligently.

A one-cent rounding difference from a long-time vendor is noise. A $1,200 subtotal mismatch, a changed bank account, a new approver, and metadata showing edits after submission is a symphony.

That is why the best fraud teams build a layered view. Visual tampering, metadata, mathematical inconsistencies, physical manipulation, vendor history, and payment details all matter. If you want a broader checklist, our guide to billing fraud red flags hidden in invoices and receipts walks through more of the non-math clues.

How I would build a math-first invoice review process

If I were redesigning invoice review from scratch, I would not start with the prettiest dashboard. I would start with the arithmetic.

First, rebuild every invoice total from the ground up. Do not trust the printed subtotal. Extract quantities, unit prices, discounts, taxes, fees, credits, and final amount, then compare the rebuilt total to the claimed total.

Second, compare the invoice against known context. Vendor history, purchase order terms, claim details, policy limits, expense policy, payment method, and prior submissions should all have a vote.

Third, escalate based on combined risk, not one weird field. A tax mismatch alone may be a training issue. A tax mismatch plus altered metadata plus a new bank account is a different animal.

Fourth, preserve the original file whenever possible. Screenshots and compressed images destroy evidence. If someone uploads a PDF, keep the PDF. If someone submits a phone photo, keep the original image. Compression is where forensic detail goes to retire.

Finally, give reviewers an explanation they can act on. “Suspicious document” is vague. “Invoice total is $2,430 higher than recalculated line items, tax amount matches a lower subtotal, and payment account changed from prior vendor record” is useful.

That level of clarity helps AP managers, claims adjustors, fraud teams, and expense reviewers make faster decisions without turning every approval into a courtroom drama.

Where Docklands AI fits

At Docklands AI, we focus on detecting manipulated, photoshopped, and AI-generated invoices and receipts before they create losses. The reason math matters to us is simple: document fraud is rarely only visual. A changed pixel may reveal the edit, but the payment context often reveals the motive.

That is why invoice and receipt analysis should combine document forensics with mathematical checks and payment information. If the document looks normal but the numbers do not reconcile, we want that surfaced before money leaves the business or a claim is settled.

For claims teams, that can mean catching inflated repair bills or altered receipts. For AP teams, it can mean finding suspicious invoices before payment. For expense teams, it can mean spotting manipulated receipts without asking managers to play detective after dinner.

The calculator will not replace judgment. But it will embarrass a surprising number of doctored invoices.

Frequently Asked Questions

What are doctored invoices? Doctored invoices are invoices that have been altered, fabricated, or manipulated to change details such as totals, line items, dates, tax amounts, vendor information, or payment instructions.

Why do doctored invoices often fail math checks? Fraudsters often edit the amount they want paid but forget to update related fields such as tax, discounts, subtotals, deposits, or line-item totals. That creates inconsistencies a visual review may miss.

Can an invoice have a math error without being fraudulent? Yes. Rounding differences, tax rules, OCR mistakes, and vendor errors can all create innocent mismatches. The key is to combine math checks with metadata, vendor history, payment details, and document forensics.

Which teams should check invoice math most carefully? Insurance claims teams, accounts payable teams, employee expense managers, payroll teams, and fraud investigators should all check invoice math, especially when payments are large, urgent, unusual, or tied to new bank details.

Is manual review enough to catch doctored invoices? Manual review helps, but it struggles at scale. Busy teams often focus on whether a document looks normal. Automated checks can recalculate totals, compare payment context, and flag suspicious patterns before approval.

Stop letting bad math approve good-looking fraud

Doctored invoices are designed to look routine. The safest response is to make routine checks smarter.

If your team is reviewing invoices, receipts, claims, or expenses at volume, Docklands AI can help detect manipulation using document forensics, mathematical irregularity checks, metadata analysis, and payment context. The goal is not to slow every payment. It is to stop the ones that should never leave the building.

If you want to see how stronger invoice and receipt fraud detection could fit into your workflow, visit Docklands AI and start with the documents that look normal, especially the ones whose math quietly disagrees.

Request a Demo Today!

Book your demo below.