Property Insurance Claim Fraud Hides in Repair Documents

My hot take after a decade around claims fraud: the best place to find property insurance claim fraud is usually not the dramatic photo of the collapsed ceiling. It is the repair document that looks boring enough to skip.

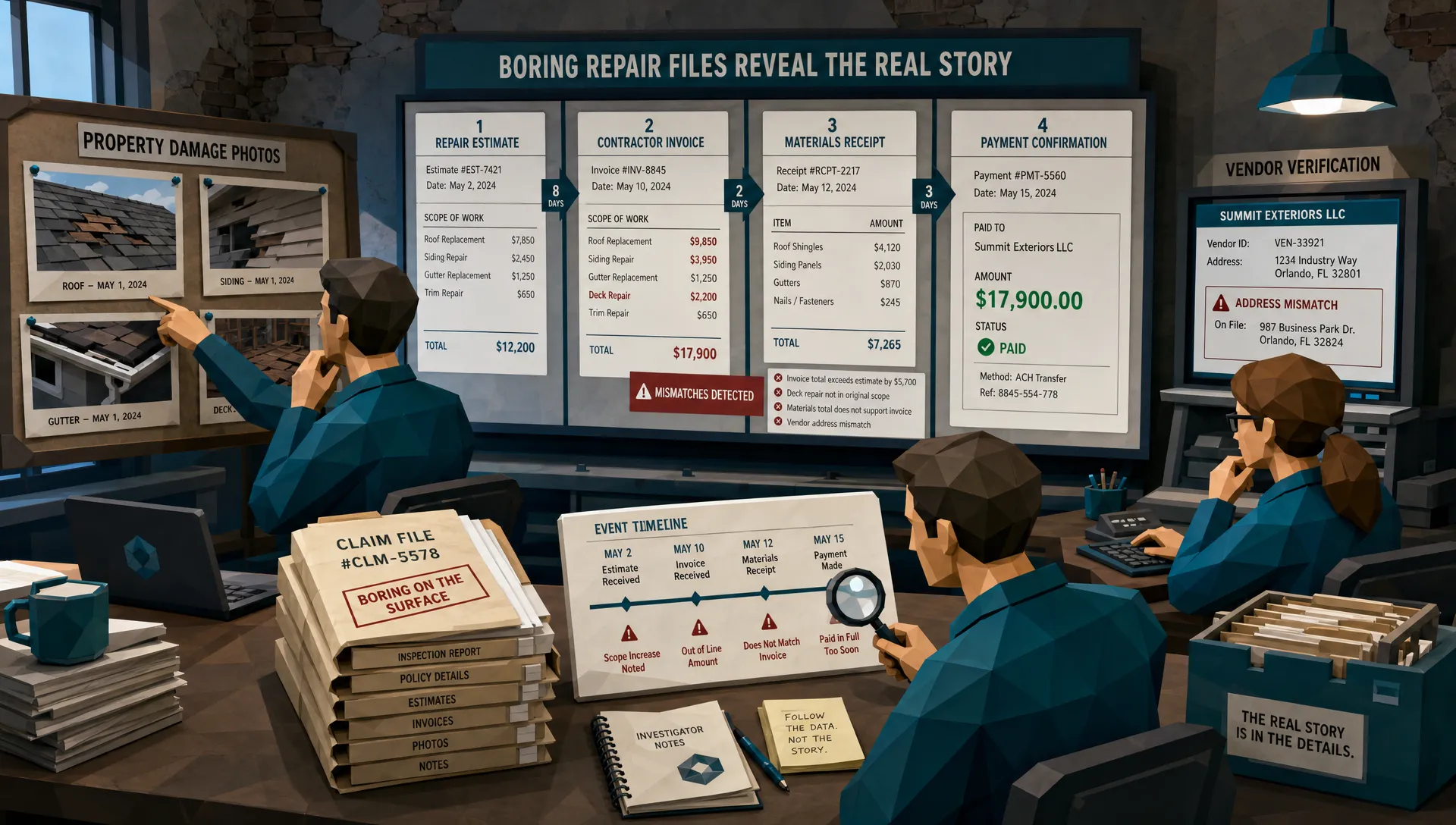

That sounds backwards, I know. Photos get attention. A smoky wall, a flooded laundry room, a roof with missing shingles, those images feel like the case. But repair estimates, contractor invoices, supplements, payment receipts, and work completion notes are where the story either holds together or starts limping.

I once reviewed a kitchen water-loss claim where the photos looked clean, the insured was polite, and the contractor invoice was formatted beautifully. Too beautifully, as it turned out. The invoice included line items for removing and replacing oak baseboards. The property photos showed tile baseboards throughout the kitchen. Nobody had noticed because the dollar amount was ordinary, not outrageous. Fraud does not always arrive wearing a fake mustache. Sometimes it arrives as a $640 line item.

Why repair documents deserve more suspicion than they get

The industry has spent years training adjusters to look at damage photos, statements, and coverage. That still matters. But repair documentation has become the soft underbelly of property claims because it is easy to create, easy to edit, and often reviewed under time pressure.

The FBI notes that insurance fraud costs families through higher premiums, with non-health insurance fraud estimated at more than $40 billion annually. Property claims are not the only culprit, but they are a ripe environment for document fraud because so many third parties touch the file: roofers, mitigation vendors, plumbers, electricians, flooring crews, public adjusters, emergency repair firms, contents vendors, and sometimes a cousin with a printer.

The newer wrinkle is that manipulated documents no longer look sloppy. A fake invoice can have a logo, tax ID, line-item detail, a QR code, and a polite footer thanking you for your business. A repair estimate can be nudged rather than invented. A contractor can take a real invoice and alter the date, scope, or total. That is why property insurance claim fraud often hides in repair documents, not because the documents are always fake, but because they are flexible.

A 2025 BBC report on Admiral described a sharp rise in fraudulent claims involving manipulated evidence. Verisk’s 2025 fraud report also points to a market where claim manipulation is becoming more sophisticated. I do not read those reports and think, “The robots are coming.” I think, “The paperwork is getting better at lying.”

The repair document is not one document

When people say “the repair invoice,” they often mean one PDF. In practice, a repair file is a chain. That chain might include the initial estimate, mitigation invoice, contractor supplement, materials receipt, payment confirmation, proof of completion, photos of the damaged area, and sometimes a public adjuster package.

The trick is to stop reviewing each item like it lives alone. A document can look fine in isolation and still be wrong in context.

A roof estimate dated Monday may be plausible. A materials receipt dated three days before the reported hailstorm is more interesting. A water mitigation invoice may have standard equipment charges. A drying log showing dehumidifiers running after the certificate of completion was signed is more interesting. A contractor supplement might include code upgrades. A permit record showing no permit pulled is more interesting.

That is the point. Fraud rarely confesses inside one box. It leaks between boxes.

If you want a broader view of how supporting evidence breaks down, we have written about how false insurance claim evidence falls apart under review. Property repair documents follow the same pattern: the weakness is usually in the relationship between dates, amounts, vendors, photos, and payments.

The documents I would never let pass on autopilot

Some repair documents deserve more attention than others. Not because they are always fraudulent, but because they carry the most opportunity for inflation or substitution.

The initial estimate sets the anchor. If it is inflated, everything downstream starts too high. The supplement is where scope creep often enters the room wearing a hard hat. The final invoice is where estimates become “completed work,” sometimes without matching proof. Materials receipts can be reused or borrowed. Payment confirmations can show whether the money actually went where the invoice says it went.

In my experience, these are the repair documents most worth slowing down for:

- Contractor estimates that are unusually generic or unusually detailed for the damage shown.

- Supplements that add high-margin items without new photos, adjuster notes, or code support.

- Final invoices that copy the estimate exactly, including quantities that should have changed after inspection.

- Materials receipts that do not match the property, season, vendor location, or claimed repair type.

- Proof of payment that points to a different business name, personal account, or suspicious timing.

- Completion documents signed before materials were purchased or before mitigation could realistically end.

I am not saying every mismatch is fraud. Small contractors are not all accountants. Some use templates from 2014, handwritten notes, and a scanner that sounds like a lawnmower. That messiness can be perfectly legitimate. What worries me is not mess. What worries me is a document trail that is too convenient.

The “too clean” repair file problem

Here is another unpopular opinion: the most suspicious file is not always the messy one. Sometimes it is the one that looks like it was built for an audit.

Real repairs are noisy. Dates shift. Labor changes. Materials get substituted. A plumber comes Tuesday instead of Monday. The flooring vendor backorders the exact product. A homeowner pays a deposit, then pays the remainder later. The documentation should still make sense, but it often has normal wrinkles.

Fraudulent repair packages can look strangely frictionless. The estimate, invoice, and payment proof all match perfectly to the penny. The supplement explains everything neatly, but there is no field note that triggered it. The photo set includes the exact angles needed to support the new line items, but no broader room context. The invoice language is professional, yet the vendor cannot be found at the address listed.

That is why I like to review repair files the way a claims veteran reviews a story over coffee. Does it sound lived-in? Or does it sound rehearsed?

Documentation discipline matters in any trust-based service. Even outside insurance, a patient would expect medically supervised weight-loss programs to keep assessments, follow-ups, and progress records that support the treatment plan. Property repairs deserve the same boring consistency: scope, timing, materials, and payments should line up without needing mental gymnastics.

The red flags that actually matter

I have a soft spot for simple red flags because they catch real problems without turning every claim into a courtroom drama. Here are the patterns I pay attention to first.

Dates that make the repair timeline impossible

Dates are the low-hanging fruit, which means they are also the fruit everyone forgets to pick.

A contractor invoice dated before the loss is obvious. More often, the issue is subtler. The estimate is prepared before the inspection could have occurred. Materials are purchased before emergency mitigation is complete. A supplement is submitted after final payment, but claims to reflect work required before completion. A hotel receipt overlaps with a completed repair sign-off.

One roof claim I saw had a supplement for interior water staining tied to a storm date. The contractor photos showed wet ceiling spots, but the file also had an earlier invoice for repainting the same room. The “new” damage was possibly old damage wearing a fresh storm hat.

Scope that does not match the damage

A scope mismatch is not always about dollars. It is about physical logic.

If a bathroom leak affects one vanity wall, why are we replacing flooring in three rooms? If smoke damage is limited to a kitchen appliance fire, why is the estimate charging for full HVAC duct replacement? If a tree strikes the garage roof, why does the invoice include interior painting in the primary bedroom?

Good adjusters already think this way. The challenge is that modern repair documents bury questionable scope inside familiar estimating language. The line items look normal. The combination does not.

For related patterns across claim types, our guide to fraud insurance claim tactics adjusters should watch covers how inflated invoices, altered receipts, and staged support documents tend to show up in the file.

Supplements that become a second claim

Supplements are necessary. Anyone who has opened a wall knows the first estimate is sometimes only a polite guess. But supplements are also where property insurance claim fraud can quietly gain altitude.

The fraud risk is highest when the supplement adds new damage categories rather than refining known repair work. A legitimate supplement might add hidden mold remediation discovered behind drywall. A suspicious supplement adds unrelated flooring, cabinetry, or exterior work without inspection notes, photos, code citations, or vendor explanation.

The phrase I listen for is “while we were there.” It can be legitimate. It can also be the opening line of a very expensive fairy tale.

Vendor identity that does not survive a five-minute check

Repair fraud often depends on a vendor name that appears credible enough to avoid scrutiny. The invoice may list a business name, phone number, address, and license number. That does not mean the vendor did the work, exists at that address, or received the payment.

Watch for contractor names that differ slightly across documents. “ABC Restoration LLC” on the estimate becomes “ABC Restore Services” on the invoice and a personal payment to “Mike B.” That might be sloppy admin. It might also be a borrowed invoice template or a shell vendor.

When public adjusters are involved, the documentation can become even more layered. Some files are perfectly legitimate. Others contain representation agreements, contractor estimates, and repair invoices that seem to move as a pack. We explored that document trail in our article on public adjuster scams and the documents behind them.

Math that is technically correct but commercially weird

Fraud review is not only about bad arithmetic. Plenty of fraudulent documents add up correctly. The better question is whether the math behaves like real repair work.

Does the labor rate fit the region? Are material quantities realistic for the square footage? Are overhead and profit applied where they make sense? Is tax charged on items that should not be taxed, or missing where it should appear? Are identical line items repeated across unrelated rooms?

I once saw an invoice where the total was clean, the unit prices were plausible, and the format looked professional. The giveaway was quantity. The claimed paint volume could have covered the house twice. Unless the contractor was painting the walls, ceiling, driveway, and possibly the family dog, something was off.

Payment information is the underrated fraud signal

This is where I think many claims operations can improve quickly. Too many reviews focus on whether the document looks real. That is useful, but incomplete.

The better question is whether the document behaves like part of a real financial transaction.

Who was paid? When? By what method? Does the payment amount match the invoice or does it match a rounded estimate? Was the payment made before the invoice date? Was it split into unusual chunks? Does the bank account or payment recipient connect to the vendor named on the repair document?

At Docklands AI, this is one reason we look beyond surface-level document appearance. A receipt or invoice may pass a basic “does this look edited?” test, while the payment details tell a different story. For property claims, that context can separate a bad scan from a bad claim.

How I would tighten review without slowing every claim

Nobody wants a fraud process that turns a simple water leak into a 90-day saga. The goal is not to interrogate every homeowner or punish honest contractors. The goal is to route the right files to deeper review before payment leaves the building.

A practical approach is to build a repair-document triage habit. Start with timeline, scope, vendor, math, and payment. If those five areas agree, move on. If two or more disagree, escalate.

The questions are plain English:

- Do the repair dates make physical sense for the reported loss?

- Does the scope match the damage shown and described?

- Do supplements explain new work with evidence, not just line items?

- Does the vendor identity stay consistent across documents and payments?

- Do totals, quantities, taxes, and labor rates fit the job?

- Does proof of payment support the invoice rather than merely decorate it?

That last phrase matters. Proof of payment should support the invoice. Too often it merely decorates it.

The best teams I have worked with do not treat fraud review as a separate ritual performed by a distant department. They teach adjusters to notice the first oddity, then give fraud teams the tools to confirm or dismiss it quickly. That keeps honest claims moving and gives suspicious files the attention they deserve.

Do not confuse suspicion with proof

A quick caution from someone who has been humbled more than once: red flags are not convictions.

Contractors make clerical errors. Homeowners misplace receipts. Emergency repairs happen out of order. Rural vendors may have odd payment practices. A family dealing with a fire loss may not present documents like a corporate finance department.

The danger is turning every inconsistency into an accusation. That creates bad customer outcomes and wastes investigative time. The better posture is curiosity. Ask for clarification. Compare the file. Validate the vendor. Check the payment trail. Look for patterns, not one lonely typo.

Fraud detection should be a scalpel, not a leaf blower.

Frequently Asked Questions

What is property insurance claim fraud? Property insurance claim fraud happens when someone intentionally misrepresents a property loss to receive payment they are not entitled to. In repair documents, that can include inflated estimates, altered invoices, reused receipts, fabricated contractor bills, or supplements for work that was not caused by the covered loss.

Why do repair documents matter so much in property claims? Repair documents translate damage into dollars. Photos show what may have happened, but estimates, invoices, receipts, and payment records determine what gets paid. That makes them a common place for exaggeration, manipulation, or borrowed proof.

Is an incorrect invoice always evidence of fraud? No. Mistakes happen, especially in urgent repairs. A wrong date, typo, or mismatched business name should trigger review, not automatic denial. Fraud is more likely when multiple inconsistencies point in the same direction.

Which repair document is most commonly abused? Supplements are especially risky because they are submitted after the initial estimate and can add new scope. Final invoices and proof of payment are also high-value review points because they connect the claimed repair to actual money movement.

How can insurers reduce false positives during repair document review? Use context. Compare documents to each other, not just to a checklist. A file with one typo may be harmless. A file with timeline conflicts, vendor inconsistencies, edited metadata, and payment mismatches deserves a closer look.

See what the repair documents are really saying

Property claims will always involve judgment. But judgment gets sharper when the paperwork is examined as a connected story, not a stack of attachments.

Docklands AI helps claims teams detect manipulated, photoshopped, and AI-generated invoices and receipts, while also using payment information to build a deeper fraud picture. If your team is reviewing property claims at scale, the repair documents are too important to leave to a quick glance.

Because the next fraudulent claim probably will not announce itself with a cartoon villain laugh. It will arrive as a clean PDF with a contractor logo and a total that looks just reasonable enough.

Request a Demo Today!

Book your demo below.